We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

My initial plan to retire at 59 hoping for some advice

Comments

-

The ability to take take tax free cash over an extended time period only applies to Defined Contribution pensions. Fidelity, where you got your information from, are not involved in DB pensions.LL_USS said:

The TFLS is only a one-off option? So it's different from this general rule: https://retirement.fidelity.co.uk/access-your-pension/taking-tax-free-cash/ ??:GrumpyDil said:OP is talking about USS pension which is defined benefit so the tax free element is handled differently.

The OP can take a pension commencement lump sum ranging from 0 up to maximum amount they are entitled to.

It is a one off option and doesn't remain in the fund and OP can't take further sums later.

What it does impact is the regular pension payments which reduce/increase according to the lump sum payment.

"Take less than the tax-free allowance – if you don’t need all your tax-free cash, you don’t have to take it all at once. Just withdraw as much as you want and whatever is left can be taken later. If your pension savings rise in value, this could mean you could take a larger total amount tax-free."

With a DB scheme taking the TFLS and starting to receive your ongoing pension all happens at the same time.2 -

It isn't a 'general rule' - it's a rule which applies only to defined contribution schemes.LL_USS said:

The TFLS is only a one-off option? So it's different from this general rule: https://retirement.fidelity.co.uk/access-your-pension/taking-tax-free-cash/ ??:GrumpyDil said:OP is talking about USS pension which is defined benefit so the tax free element is handled differently.

The OP can take a pension commencement lump sum ranging from 0 up to maximum amount they are entitled to.

It is a one off option and doesn't remain in the fund and OP can't take further sums later.

What it does impact is the regular pension payments which reduce/increase according to the lump sum payment."Take less than the tax-free allowance – if you don’t need all your tax-free cash, you don’t have to take it all at once. Just withdraw as much as you want and whatever is left can be taken later. If your pension savings rise in value, this could mean you could take a larger total amount tax-free."From what I understood, if Twigwidge has 151K as max TFLS, if they only take, say 51K out at start of retirement as TFLS then the 100K remaining still should have tax free status when they gradually withdraw in subsequent years.Is it not tax free if not taken at start of retirement?

OP is in a defined benefit scheme, where there's a once-only chance to take a tax free lump sum (at the point they start to draw their benefits), with the remainder of their benefits being paid as regular, taxable instalments.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!2 -

I appreciate posts like this are well meant, but it might be better not to post when you have little or no familiarity with DB schemes. The danger is that someone skim reads your post, 'remembers' incorrect 'information', reads no further in the thread...you get the picture!LL_USS said:With my limited understanding, I think there is little point for someone to take out the MAX of TFLS if they only use that sum to put into some saving accounts outside of their pension. Only take out what they need immediately (like to pay off the mortgage, retirement treats...) and leave the rest continue being invested in the pension scheme to be withdrawn each year as needed. The remaining portion of your 25% total pot should still remain tax free when you take out later. I am not sure though. Would love to hear about this from others who know pension better.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!8 -

Don’t want to pry on personal circumstances but if you’re in USS - and going by the value of your pension, been in it for a few years - then it would be to your advantage if you could finish work after turning 60 rather than at 59 as the contributions you made to the pension prior to 2011 won’t have any actuarial reduction applied. Appreciate that the finishing date might not be your choice, but if it is then I would ask to stay on a while longer (if you can bear it, that is…).1

-

@Marcon fair enough, thanks. I thought it was just a discussion to work out what's the right way forward. But you are right, it could be counter-productive. I'll just sit and listen :-) and just raise a point when I am sure. I am an enthusiastic learner though, having spent the last couple of hours checking different sources on the matter.EDIT: I asked USS about whether one has to take the whole max TFLS and this is the answer - in line with what others say here:

0

0 -

Or just ask something you're not sure about as a question, giving others the chance to confirm or correct? That way you can double check what you are thinking and/or start a discussion. Pensions are ridiculously complicated so they will always be a team game and there's nothing to stop you playing!LL_USS said:@Marcon fair enough, thanks. I thought it was just a discussion to work out what's the right way forward. But you are right, it could be counter-productive. I'll just sit and listen :-) and just raise a point when I am sure. I am an enthusiastic learner though, having spent the last couple of hours checking different sources on the matter.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!2 -

At age 59, I believe that the USS reverse commutation factor is 23.36 So giving up £10k of TFLS would increase the annual pension by £428 before tax or £321 after tax. Not exactly a generous offer. OP might do just as well sticking the money in the bank as planned. If interest rates continue to beat inflation, the initial plan is good. If inflation takes off, OP might do better with the extra pension.

If it was me I would be looking to invest some of the money, bearing in mind that some of it needs to last 7 years, some much more. I'm not saying bet it all on BitCoin, but a diversified tracker fund is likely to beat inflation over that period. Open a SIPP and pay in as much as you can before April. Then pay in £2880/yr in May and each subsequent year. Invest in one tracker fund. This will give some protection against inflation, and improve tax efficiency.

The plan looks a little tight to me. If OP wants to retire, and is willing to make a few cutbacks, all will be fine. If they stick rigidly to the given expenditure number, I'm not sure they can increase spending to keep up with inflation. Would either need to gradually reduce spending power (no inflation increases), or the pot could run out.1 -

Many thanks to everyone that has replied so quickly, as I mentioned I am on a very steep learning curve here so all these comments/advice are very gratefully received 😊. This is rather long as I wanted to reply to the initial comments

@QrizB, unfortunately the only other savings I have are just under 10K in a cash ISA, as I have been using all spare cash over last few years to finish paying off mortgage (which is now paid)

@Dazed_and_C0nfused, yes this amount does have an actuarial reduction because of age and also a penalty for going before the age of 60 (explained below)

Here is my USS model prediction (hope I am allowed to post this)

£18.239 gross pension = £17,105 net = Just over £1,400 a month

The maximum tax free lump sum of 121,595 will be topped up to £151,000 by a tax-free voluntary severance payment of £30,000 to £151,000

@Dazed_and_C0nfused, I am not sure what tax code would be used, I have heard that some people initially are put on an emergency tax code but claim any overpayments back, how would I find out what tax code I would be on? Yes this £1,400 would be net (assuming my calculations above are correct)

@LL_USS, As far as I understand the USS pension rules (and they are not easy to understand to me 😊) I seem to be better off taking the maximum tax free lump sum as USS (appear) to give a one off opportunity (I think this is what GrumpyDill is referring to?) of taking most of my defined contribution savings tax free (note on USS model screenshot that my DC pot is at Zero if I take the maximum TF lump sum)

@Phossy, yes initially I will put all my tax free money into a 4% savings account and the transfer over a few years into both mine and my partner’s ISA allowances 😊 Yes I agree about savings protection and will definitely split initial savings over 2 accounts to benefit from the £85,000 FSCS protection

@Linton and Marcon, aside from near 10k in an ISA I have no other savings or pension pots of any kind and I have checked my state pension forecast and will have 34 full years at time of retirement 31st July) so I will need to top up 1 year eventually to get full state pension. I think there is a 10% cap on USS pension increases but it is not entirely clear on their website.

@Marcon I had no real opportunity to save since all extra cash has been used to finish paying off my mortgage, so just under 10K in an ISA and that’s all my savings, I will certainly max out both mine and partners ISAs when my lump sum is paid 😊 Sorry about the £ sign, I was typing my initial post on my phone and it is a nightmare to access the symbols, I will edit the original post later this evening if I can work out how to do this 😊

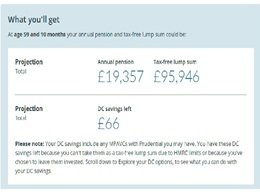

@Abermarle, Yes I could take slightly more pension and less lump sum, the maximum DB pension I can take is £19,357 gross (see screenshot below)

This would be a fraction under £18,000 net (£17,999) = bang on £1,500 per month net

But obviously this reduces my lump sum by £25,649 (121,595-95,946)

If I went down this route the total going into my savings would now be £95,946+£30,000 (severance) = £125,946

So if I put this in my savings account to top my pension up to my desired £2,500 per month I need £1,000 per month for 7 years (to state pension)

1,000 x 12 x 7 = £84,000 = This would leave £41,946 of my lump left at state pension age

After playing with the modeller to me it seems the most sensible choice for me was to take the maximum lump sum as taking the maximum pension would only give me an additional £75 per month (net) but result in a loss of 25.5K lump sum (I guess it is just personal choice in the end). I think this is what @Secret2ndAccount is indicating later in the thread as the reverse commutation factor is so poor

@Barralad77, I would love to take my pension at 60 to avoid the penalty but if I want the severance package like many Universities I have to take it by 31st July (a few months before I turn 60) I have looked into this with the Uni but they won't budge on this. I was hoping that if I still went on 31st July but deferred taking my pension until after I was 60 that this may be a way around the early penalty but after speaking with the USS advisor on the phone, deferring the pension immediately triggers the early penalty. I don't think there is any way around this (unless anyone knows better). For me I am willing to take the hit to get the severance package 😊

@Secret2ndAccount, Yes I certainly will be looking at other places to put the lump sum, I just have a feeling that investments in the current world economic climate may be a bit more risky than usual so probably safer in ISAs and the highest interest savings accounts I can get.

Thanks so much everyone for taking the time to reply

1 -

On the last point, the current global economic and political climate always looks risky, whenever you look at it. However most often markets just shrug it off. They are more interested in how many I phones Apple sell than the war in Gaza, Ukraine etc.

Over the long term it is actually more risky holding on to too much cash.0 -

Re. The point about losing out even if you defer taking it until you’ve turned 60. I learnt the same thing long after I’d spent years believing otherwise. It’s really annoying and I’ve never known what the reasoning behind it is. In terms of you discussing the possibility of staying on a few months longer, have you asked whether they’d accept you reducing your hours such that you would still be working a further 6.0FTE months? For example, if you needed to stay working until the end of December, would they allow you to drop down to, say, 0.5 for 10 months? So rather than earn 6 x 1.0 (Feb-July) you would work 1 x 1.0 (Feb) plus 10 x 0.5 (Mar-Dec). They both work out at 6.0 FTE months. Obviously, there are other factors to consider but it’s something I’d consider pursuing (if you’re losing out quite a bit on the pension for the sake of a handful of months).

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards