We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Annuities versus Drawdown versus both

Comments

-

A nice aspect of an annuity is that it gives you an income that is generally initially greater than that recommended that you take from a DC account as it has the mortality credit and also return of capital baked in. This can take pressure of your DC drawdown. However, DC drawdown will almost always be better for your overall lifetime finances, giving you flexible access to your capital and your heirs a larger inheritance - it's the "almost" in that sentence that is critical to your decision.Triumph13 said:Another vote for a mixed solution. The headache of drawdown strategies is trying to turn a volatile set of returns into a level income. If you are prepared to accept a volatile income, then many of those issues go away and you can have a higher equity percentage and expect a greater total income over the long run.

The greater the amount of fixed, indexed income you have from SP, DB and annuities, the higher the degree of volatility you can put up with from your drawdown portfolio. I'm a firm believer in creating, if you can afford to, enough fixed income that you can afford to not worry about volatility in your drawdown income. I find that a lot less stressful than trying to maximise a fixed drawdown income and then worrying about your pot surviving.

We are lucky enough not to need to buy any further annuity as we'll have a couple of small DBs plus our SPs, with cash being used to stand in for these until they arrive. That gives us enough of a floor that we are comfortable with 100% equities in our drawdown pot and a fixed percentage withdrawal method. Add in the impact of tax and a 50% drop in portfolio value will translate as a 20% drop in our budget. Everyone will have their own answer to what the mix of fixed to variable income should be. That one works for us.And so we beat on, boats against the current, borne back ceaselessly into the past.1 -

Sales of annuities are already increasing. With the normalisation of interest rates. They provide a decent level of guaranteed return. Those investors that actively traded shares in the pre 2007 GFC era. Will be prepared for what's to come. Now that Central Banks are no longer underpinning the equity markets.Springfield1970 said:

What are your thoughts/experiences with this? I am aware that annuities haven't been optional for a while, but I think they are going to become popular and feasible again from 2027 (when the IHT law changes)3 -

Agree with @Hoenir. Annuities are rightly becoming more attractive now for fundamental pricing reasons, and that's 2-3 years before the 2027 proposed changes which for me are secondary.

A mix of drawdown and annuity may be right for many.3 -

I have been pondering similar issues as the OP for many months. Have decided to buy a joint life RPI linked annuity with 20-25% of my pension and put rest into drawdown for now.3

-

Thanks for your reply. I'm aware of not tinkering with investments and that they should be boring and left alone. When I had sub £100k I wasn't really bothered about fluctuations. I suppose when I say hobby I mean preoccupation and a sense of responsibility. After all that pot is something very precious and hard earned and needs looking after. With an annuity there would be no work, monitoring or learning, forums, meeting with WA, or worry about it crashing or failing, or getting muddled and confused or having to make choices (in my 70s,80s).dunstonh said:However, Drawdown is also a nice idea. Control, a hobby, potentially bigger gains, but I can't help feeling that seeing it dwindle down would be like watching a ticking clock.hobby shouldn't come into it. If you are investing correctly, it should be boring as hell. If you are looking for it as a bit of excitement, then you are more likely to end up with a poorer outcome.

Statistically, in most periods, drawdown will beat annuity unless you are too heavy in low volatility investments). In a small number of periods, annuity will be better.

A mixture of the two is viable. This also includes the method of deciding how you would split equities and bonds. e.g. 60/40 but rather than buying bonds, you use the 40% to buy an annuity and go 100% equities with the remainder.Also, I imagine I'd be very anxious about the inevitable crashes, and I don't want to deal with that when I'm in my 70s or 80s.You get one every 5-7 years, you have probably gone through many before. So, why are they are concern now?

What did you do in the past when they happened?I'm mostly in NA equities and world index, little bonds.Which is at odds with what you describe about yourself.The growth has been massive the last few months, and I know what's coming.Not really.

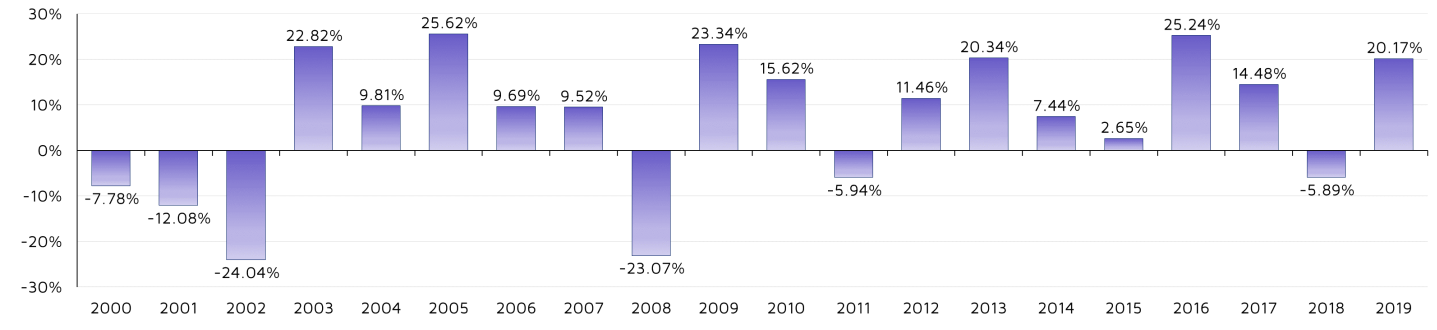

if you look at a 100% equities portfolio over 20 years with 80% developed, 15% UK and 5% emerging (you would likely have less nowadays but we must not apply today's thinking to past thinking) you will see that there have been plenty of years where the returns have been similar or larger.

Interesting statistics, but I can't help feeling that the statistics for annuity versus drawdown must be more nuanced, ie women like me that are healthy and clean living. I see annuities like a lottery where you can potentially get incredible returns, which is why I wanted to start one quite early and get way more than 15 years. Psychologically I think that would be quite positive, like a 'live longer to beat the system' challenge. This is why I was interested in your thoughts and experiences about this aspect.

I like the 40% annuities 60% equities idea. Crashes didn't bother me before because I didn't have more than £100k in. I see that the more I have, the more I am concerned, I also know that crashes recover and not to sell. I'm fine with that risk NOW. When I'm older I may be different. Who knows? I saw my FIL obsessively worrying about his pot, it had to reach £1m, he was well beyond retiring and he wasn't touching it. It was like it was tied up in his mortality. It scared me, I don't want to become one of those people.

My particular funds have grown about 15% after fees since I made changes from less tech 5 months ago. That's the biggest growth I've seen yet, but I've only been investing for 8 years.

0 -

Thank you for your reply. Good stats. And I'd also be leaving something for my son, though he would rightly so have to pay tax on it. Not as attractive as him not paying tax on it, but perhaps I could also use it to help him out while I'm still on the planet.Albermarle said:Drawdown is also a nice idea. Control, a hobby, potentially bigger gains, but I can't help feeling that seeing it dwindle down would be like watching a ticking clock.

Based on historical statistics, there is the concept of a Safe Withdrawal rate ( nothing is guaranteed but it is is a useful rule of thumb)

The correct SWR ( typically 3.5% to 4%) should mean that the pot has only a 5% chance of running out before you are 95 ( or something along those lines) . It is quite possible you will die with substantially more than you started with.

So unless you were unlucky and markets were very poor for extended periods, it is unlikely you would see your pot dwindle away. The key is not to withdraw from it too quickly.

If you are interested there are two threads on this subject currently running ( listed very close to yours)

But do most 95 year olds log on to their investment accounts and make complicated decisions with their SIPPS?

I find it all mind boggling as a 54 year old, almost like a part time job! I enjoy it and its rewarding, but also a bit scary.2 -

Thank you , this is very interesting to hear how this all works in day to day life. I think I may regret giving up control. I also assumed it wouldn't grow any further if I took the natural yield. Maybe starting off in drawdown and then seeing how it goes might be best. I am going to stop feeding it when Im 61/62 though.tacpot12 said:I think you are right to consider the psychology of investing. You have some experience of this, and can see the downsides of having to manage your SIPP. But I think you also have to consider whether you will regret giving up the control you currently have.

I have my SIPP In drawdown, and am living off the natural yield of the portfolio, which is about 4.2% pa. The portofolio is increasing in value slowly, so the natural yield is also going up (probably at around 1/3rd the rate of inflation). So there is no need for you to watch the value of your portfolio dwindling down, unless its small to start with.

I'm invested mainly in Investment Trusts, but with a few Unit Trusts and a couple of EFTs. The portfolio was designed to be pretty much a buy-and-forget deal, and it has proven to be that with few surprises. There have been a couple of corporate actions that needed some decisions, but never more than one a year. The big change will come when I hit my State Retirement age. At that point, all my DB pensions will also be in payment and I would be in a position to convert about half of my portfolio back to being growth/accumulation focused. The question is: with the proposed change tht IHT will apply to pensions, would it be better to continue to have the income and extract it and give it away to my children?

There is a lot of room for creativity that I didn't realise, like going from a safer position and then later more risk when you get the SP. That's quite interesting. Also there's so much more flexibility. Like drawing down different amounts, ie funding a sabbatical year then maybe not drawing down for a couple of years. I like that.

I suppose your children could inherit some of it after tax. How do you feel about all our efforts to be tax efficient then losing a bloody great chunk of it at the end anyway? And do you forsee the rules changing again come the next election round?0 -

Thank you for your reply. No DC pot here just SIPP. It's been strongly recommended I don't use the TFLS to pay off the mortgage but I've run the figures and it's so tempting (I hate having to pay the interest and the critical illness insurance and income protection insurance). I did do some calculations, but I think I need to do them again. However, if my pot doesn't dwindle down and I don't take the TFLS then the TFLS portion could be worth a LOT MORE as it grows particularly as I plan to continue running my business until I drop.Bostonerimus1 said:My advice would be to pay off the mortgage from income before you retire...don't use the TFLS to pay it off. Then secure a base of income with a lifetime annuity, there are arguments for either index linked or fixed, and do drawdown from the DC pot. If you can DIY the drawdown, as financial fees are a big drag on your drawdown amount, especially in the early years.

Oh but to be free of the chalice of half of my take home pay servicing mortgage capital, capital overpayments, and pension investments. It takes a lot of discipline and sacrifice.

0 -

Thank you for your reply. Your plans look well thought out and you know yourself well. I'm leaning more towards a mixed approach with all this information.Lowtrawler said:The truth is, there are no right or wrong answers on what investment approach will be best when you retire. As Dunstonh points out, there are statistical probabilities about which approach will normally be best but this needs to be tempered by your attitude to risk and a statistical probability is not a certainty.

Personally I expect to spend around 20% more in retirement than I do currently. Through bond ladders, defined benefit pensions and state pension I have this covered (so long as the tax rules, tax bands and state pension rules don't alter dramatically). I also plan to hold around 4 years net spend in more volatile funds to allow for capital repairs and replacements (cars, home maintenance). I will consider changing the bond ladder to an annuity later in life and we own our own home which can ultimately act as a safety net. I know this is much more conservative than many people will be happy with but I don't want to worry about finances once I retire.

With fewer people having access to DB pensions and annuity rates currently at more acceptable levels, it is likely more and more people will be considering annuities for peace of mind in retirement. You sound like someone who has a low threshold to risk and so at least some of your investments should be considered for annuities.

Here's an idea. I think it's possible to hold BOTH HIGH and LOW threshold to risk. I think the feelings about risk live on a spectrum, changing hourly, daily, at different ages and states of living, like all emotions, and I see money as the ultimate psychology. I find it fascinating. And more and more of us are having to become involved in our pension decisions. Which is difficult as it is a minefield with not a lot of clarity and accessibility. We are lucky to have forums like these (this particular forum has set me on the way to having substantial net worth and a sense of empowerment).

1 -

Thank you. As I enjoy working I think I'll have my basics covered, then by SP age, that'll cover my mortgageless basics. I suspect I'll keep working so I'll be very grateful of the TFLS portion of the drawdown and I'll be able to live with volatily.Triumph13 said:Another vote for a mixed solution. The headache of drawdown strategies is trying to turn a volatile set of returns into a level income. If you are prepared to accept a volatile income, then many of those issues go away and you can have a higher equity percentage and expect a greater total income over the long run.

The greater the amount of fixed, indexed income you have from SP, DB and annuities, the higher the degree of volatility you can put up with from your drawdown portfolio. I'm a firm believer in creating, if you can afford to, enough fixed income that you can afford to not worry about volatility in your drawdown income. I find that a lot less stressful than trying to maximise a fixed drawdown income and then worrying about your pot surviving.

We are lucky enough not to need to buy any further annuity as we'll have a couple of small DBs plus our SPs, with cash being used to stand in for these until they arrive. That gives us enough of a floor that we are comfortable with 100% equities in our drawdown pot and a fixed percentage withdrawal method. Add in the impact of tax and a 50% drop in portfolio value will translate as a 20% drop in our budget. Everyone will have their own answer to what the mix of fixed to variable income should be. That one works for us.

Now I realise it may not dwindle down, it seems I'll be able to leave at least some of it to my son. As opposed to nothing of it with an annuity. Also, it might be a comfort to have it when Im really old and perhaps need big fees.

Once that annuity choice has been made, there's no going back. And as I love working I don't think I'll really need it. If I can hold back and not panic spend the TFLS to get rid of mortgage it might be the best way. I can understand why my adviser was emphatic that I don't touch it. I just wish he'd explained it better.

Thank you all for giving me food for thought. It's really helped.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards