We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Teacher's Pension Scheme (TPS), errors on statement

I would appreciate anyone looking at the following details of a friends TPS pension statement. I have DC pensions, but follow this forum a lot and have a reasonable understanding of DB schemes. My friend ask me to help them understand this.

I can't reconcile the figures at all… To me they look like obvious errors, but can't believe an official statement can be so incorrect.

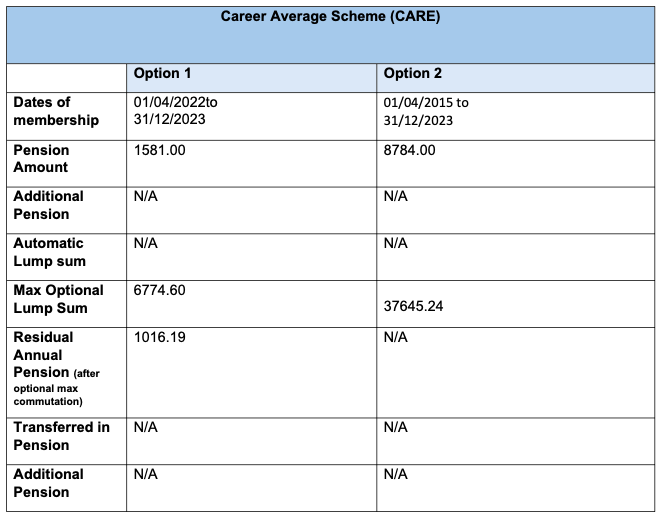

Below is a replication of the pension statement copied into a spreadsheet for easier calculations and condensed a bit to make it easier to view. As per the McCloud remedy, 2 options are given.

Option 1 : Remain in the Final Salary 80ths for 2015 -

2022

Option 2 : Opt to have the CARE scheme for 2015 - 2022

The accrual period

spans two parts, Final Salary 80ths and CARE (1/57th).

Option 1 appears to

be correct.

Option 2 appears to

be INCORRECT.

The stand out error is the Total Annual Pension Amount->Total Pension, Option 2 ignores the £8,784 accrued in the CARE scheme (red boxes), surely the Total should be = 80ths + CARE?

Total Annual Pension Amount->Automatic Lump Sum. Option 2, where does £116,474 come from. This should be 3x the 80ths Total Pension = £47,307 (green boxes)

Also, if you calculate the Max lump sum from Option 1 (yellow boxes), £61,431.67 + £48,267.75 + £6,774.60 = £116,474.02.

???? Has this been copied into the Option 2 Total Automatic Lump Sum box?

So

either I don't understand how the TPS DB works, or the statement is incorrect.

Any insight into this would be appreciated.

Comments

-

My OH is a deferred member of the NI-TPS (same as normal TPS but for teachers in Northern Ireland). Her pension statement was a complete mess. We wrote to them and it took months for them to even respond.

Eventually they acknowledged it was a mess and to would be fixed in "weeks". This was over a month ago and so far nothing.

Our next step is to write to our minister for education and MP. This is so unacceptable as it makes pension planning impossible.

TPS is an utter shambles at the minute it would appear. I have heard many other similar reports.0 -

BemmaFor what it's worth, I think you are right. The total annual pension for option 2 appears to omit the CARE pension. And the automatic lump sum for option 2 is clearly incorrect (given that the CARE section does not have an automatic lump sum, it is not obvious how the automatic lump sum under option 2 can exceed that given for option 1).1

-

FS to 2015

Automatic tax free PCLS £61,431.67 and annual pension £20,477.00

Option to commute £4023 of annual pension (commutation factor 12:1) to create additional tax free lump sum of £48,267.75.

This would give tax free PCLS of £109,699.42 and annual pension of £16,454.00

CARE 2015/22

Annual Pension £1,581 per annum

Option to commute £564.81 to create tax free PCLS £6674.60 (commutation factor 12:1) with annual pension £1016.19.

£61,431.67 + £48,267.73 + £6774.60 = £116,474

Annual Pension (FS) £16,454.00 Annual Pension (CARE) £1016.19

£16, 454 + £1016.19 = £17,770.19

If CARE converted to FS

Annual Pension £22, 058 ?

Automatic tax free PCLS £61,431.67 ?

Presumably there is an option to commute up to £ ? of annual pension (commutation factor 12:1) to create an additional tax free lump sum?

What is the maximum AP that can be commuted?

0 -

@tigerspill

Thanks you for your reply, this is also NI-TPS, I didn't want to confuse things as it's the same as TPS.

When you say you statement was a complete mess, do you mean that some of the basic calculations were incorrect. I.e. Like above, the automatic lump sum for Option 2 should be 3x the FS pension.

3 * £15,769 = £47,307.00

It's listed in the statement as £116,474.00 (that's £69,167 too much, hardly a rounding error)

My friend is an active member and considering Phased retirement and is asking for help on which Option (McCloud options) is better, but the statement is so far off it's ridiculous

I would love to hear how you progress with this, as I can see my friend having to follow a similar process, if you could update this thread as things happen I would be very grateful.

0 -

Thanks you for your reply, it reassures me that I'm not getting things incorrect. It appears the £8,785 CARE value is missing from the total and from above the Automatic lump sum is £69,167 too much. How can anyone choose which McCloud option with these figures so far off.

0 -

Thanks you for taking the time for such a detailed reply, but I think the the statement is such a mess that it has led to some incorrect results. I think it's such a mess, that I've struggled to reply with what is incorrect because some basic calculations in the statement appear to be just wrong!

I think you have interpreted the options the wrong way round:

From the supporting notes:Option 1 - This is known as the Legacy option which is the pension benefits accrued when the member opts to have the CARE scheme commence from 01 April 2022.15.

Option 2 - This is known as the Remedy option, which is the pension benefits accrued when the member opts to have the CARE scheme commence from 01 April 2015.So these calculations reconcile with Option 1 above - but this is for FS to 2022.

These figures ^^^ all align with the figures in Option 1 above FS to 2022, CARE 2022+xylophone said:

FS to 2015

Automatic tax free PCLS £61,431.67 and annual pension £20,477.00

Option to commute £4023 of annual pension (commutation factor 12:1) to create additional tax free lump sum of £48,267.75.

This would give tax free PCLS of £109,699.42 and annual pension of £16,454.00

CARE 2015/22

Annual Pension £1,581 per annum

Option to commute £564.81 to create tax free PCLS £6674.60 (commutation factor 12:1) with annual pension £1016.19.

This figure, which magically appears as the Automatic Lump Sum for Option 2xylophone said:

£61,431.67 + £48,267.73 + £6774.60 = £116,474

Yes, again this correlates to Option 1 in the table above, Residual Pension.xylophone said:

Annual Pension (FS) £16,454.00 Annual Pension (CARE) £1016.19

£16, 454 + £1016.19 = £17,770.19

This should align with Option 2, but this is where the statement gets really messy.xylophone said:

If CARE converted to FS

Annual Pension £22, 058 ?

Automatic tax free PCLS £61,431.67 ?

Presumably there is an option to commute up to £ ? of annual pension (commutation factor 12:1) to create an additional tax free lump sum?

What is the maximum AP that can be commuted?CARE converted to FS - My calculations are:

Annual Pension £15,769 + £8,784.=£24,553.00

Automatic Lump Sum £47,307 (3 * £15,769)The maximum AP that can be commuted is not shown! I'll include a screen grab of the actual statement for the CARE part - as I wouldn’t believe this myself on a forum that the residual pension is N/A! This, I believe, shows clearly that the statement is incorrect.

I calculate (1:12) that the Residual Annual Pension should be £5,5646.86, which would be a maximum AP that can be commuted to be £3,137.14

This correlates with the maximum Optional Lum Sum (CARE) is 30/7ths of the Total CARE Pension value according to the scheme rules. This figure seems correct on the statement, but a residual pension of N/A is just part of this mess.

£8,784.00 * 30/7 = £37,645.71

Also, for the avoidance of any doubt, I'm suggesting to my friend that no option lump sum is commuted (1:12 is bad), but it's very difficult to explain when the statement is so incorrect!

£37,645.71 / 12 = £3,137.14

I appreciate any help with this and it's getting very convoluted and complicated. As mentioned by Tigerspill, this might be a long process to sort out!1 -

The first problem was that it took several months for them to fix the log in issues she was having.Bemma said:@tigerspillThanks you for your reply, this is also NI-TPS, I didn't want to confuse things as it's the same as TPS.

When you say you statement was a complete mess, do you mean that some of the basic calculations were incorrect. I.e. Like above, the automatic lump sum for Option 2 should be 3x the FS pension.

3 * £15,769 = £47,307.00

It's listed in the statement as £116,474.00 (that's £69,167 too much, hardly a rounding error)

My friend is an active member and considering Phased retirement and is asking for help on which Option (McCloud options) is better, but the statement is so far off it's ridiculous

I would love to hear how you progress with this, as I can see my friend having to follow a similar process, if you could update this thread as things happen I would be very grateful.

When she eventually got logged in, the initial statement she got online had the Option B columns filled with computer code!

When they fixed that, They had her length of service totally wrong. We haven't even got as far as being able to work out option B as pretty much everything is so wrong, she can't move forward. She needs these basics fixed before we can then work through the calculations sensibly. In previous years her service length was correct - so it s something they have actually now broken.

We have been promised numerous call backs and have yet to receive a single one.

If we haven't received an updated version by the new year, we will be writing to the MoEd. This has the effect of generating a 10 day resolution time line (don't ask me how I know this )

)

0 -

The handling of the McCloud remedy by TPS has been pretty underwhelming -- e.g. they still cannot show the two options on benefit statements for active members (although I understand that is coming in the new year).0

-

Just circling back on this with some progress, in case any TPS members stumble on this...

My friend queried their TPS benefits statement, on my insistence, and they have been sent an updated version. Basically the original statement was a complete mess, the new figures are:

Total Annual Pension: £15.7k -> £24.9k, £9.2k increase.

PCLS: £116k -> £47k, £69k decrease.

There was no explanation or apology for the erroneous statement, just a new one in the post!

FWIW, my friend had no concept that the original statement was incorrect, they we're ready to just except what was on the statement.

Also, it took a lot of persuasion and convincing to my friend that the new position of an extra £9+k per year (CPI indexed) is a lot better than an extra £70k-ish PCLS!1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards