We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Withdrawing up to 40% tax bracket - how long will my pension last?

Comments

-

Unfortunately investment returns are erratic in nature. Might be reassuring on a spreadsheet. The reality is going to be very different.beeza650 said:

This runs out at 98 but is wrong because it doesn't include any tax free 25% - I'd originally (and may still do) intended to withdraw that as a lump sum and buy a nicer house.eskbanker said:

I haven't modelled your scenario, but my point was that you were asking if your 'dubious' spreadsheet seemed 'about right', so if you're wanting anyone to validate your thinking then you'd need to share your workings (including the parameters you've assumed)!beeza650 said:

yup...and mine says £1m works - what does yours sayeskbanker said:It'll all come down to the quality of the assumptions, including investment growth, inflation, higher rate threshold, etc.")

0

0 -

Oh dear, why would you accept the equity risk for a 3.5% return when you can get a ~4% return from government gilts with no risk? I fear your pessimism is overdone?SouthCoastBoy said:

Am a bit more pessimistic than that equity growth 3.5%, inflation 2.5%Albermarle said:

So in that case you need to look at the possible real growth of your pension investments. 5% minus 3% inflation ( estimated) = 2%beeza650 said:

yes exactlyDullGreyGuy said:

Though that also assumes you dont increase your drawings as the thresholds for tax increase and assumes you're happy effectively reducing your spending each year as your income stays static but inflation increases prices cutting your spending power.Mark_d said:Suppose you pension pot is worth £1m at age 55. Suppose you pension pot grows at an average rate of 5% per year thereafter (after charges). Then you'll generally get £50k per year.If you withdraw less than £50k per year your fund will never run out.

I would absolutely keep up with the 40% bracket (although who knows what future taxation might look like). Also full state pension kicks in at 67 (today). The point about inflation is up to the gov really, if they don't increase the 40% bracket then yes, there'd be less to spending power.

I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.0 -

I'm hoping it isNedS said:

Oh dear, why would you accept the equity risk for a 3.5% return when you can get a ~4% return from government gilts with no risk? I fear your pessimism is overdone?SouthCoastBoy said:

Am a bit more pessimistic than that equity growth 3.5%, inflation 2.5%Albermarle said:

So in that case you need to look at the possible real growth of your pension investments. 5% minus 3% inflation ( estimated) = 2%beeza650 said:

yes exactlyDullGreyGuy said:

Though that also assumes you dont increase your drawings as the thresholds for tax increase and assumes you're happy effectively reducing your spending each year as your income stays static but inflation increases prices cutting your spending power.Mark_d said:Suppose you pension pot is worth £1m at age 55. Suppose you pension pot grows at an average rate of 5% per year thereafter (after charges). Then you'll generally get £50k per year.If you withdraw less than £50k per year your fund will never run out.

I would absolutely keep up with the 40% bracket (although who knows what future taxation might look like). Also full state pension kicks in at 67 (today). The point about inflation is up to the gov really, if they don't increase the 40% bracket then yes, there'd be less to spending power.

I can't get my head round bonds/gilts, to get that 4% return don't you need to buy at point of issue otherwise there is an underlying market price factored into the buy price?It's just my opinion and not advice.1 -

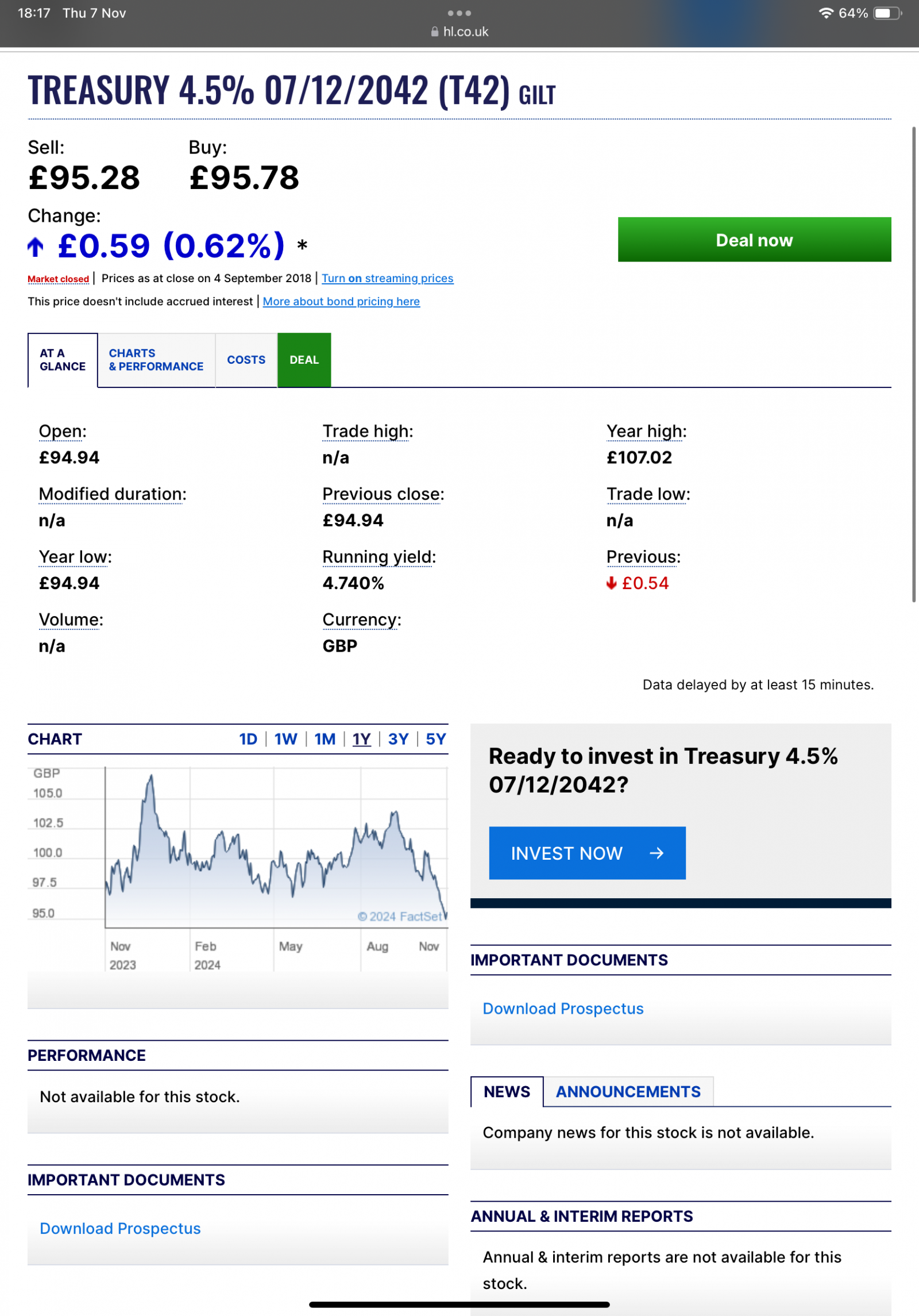

You can buy TREASURY 4.5% 07/12/2042 (T42) under the par value of £100 meaning you have a gross redemption yield in excess of 4.5% (ignore the date of 4 September 2018 - that’s nonsense, this was priced over £150 at that date as yields were much lower).SouthCoastBoy said:

I'm hoping it isNedS said:

Oh dear, why would you accept the equity risk for a 3.5% return when you can get a ~4% return from government gilts with no risk? I fear your pessimism is overdone?SouthCoastBoy said:

Am a bit more pessimistic than that equity growth 3.5%, inflation 2.5%Albermarle said:

So in that case you need to look at the possible real growth of your pension investments. 5% minus 3% inflation ( estimated) = 2%beeza650 said:

yes exactlyDullGreyGuy said:

Though that also assumes you dont increase your drawings as the thresholds for tax increase and assumes you're happy effectively reducing your spending each year as your income stays static but inflation increases prices cutting your spending power.Mark_d said:Suppose you pension pot is worth £1m at age 55. Suppose you pension pot grows at an average rate of 5% per year thereafter (after charges). Then you'll generally get £50k per year.If you withdraw less than £50k per year your fund will never run out.

I would absolutely keep up with the 40% bracket (although who knows what future taxation might look like). Also full state pension kicks in at 67 (today). The point about inflation is up to the gov really, if they don't increase the 40% bracket then yes, there'd be less to spending power.

I can't get my head round bonds/gilts, to get that 4% return don't you need to buy at point of issue otherwise there is an underlying market price factored into the buy price?

1 -

Thks for that, so I guess I should look for gilts below par value. Are all gilts issued at par value £100FIREDreamer said:

You can buy TREASURY 4.5% 07/12/2042 (T42) under the par value of £100 meaning you have a gross redemption yield in excess of 4.5% (ignore the date of 4 September 2018 - that’s nonsense, this was priced over £150 at that date as yields were much lower).SouthCoastBoy said:

I'm hoping it isNedS said:

Oh dear, why would you accept the equity risk for a 3.5% return when you can get a ~4% return from government gilts with no risk? I fear your pessimism is overdone?SouthCoastBoy said:

Am a bit more pessimistic than that equity growth 3.5%, inflation 2.5%Albermarle said:

So in that case you need to look at the possible real growth of your pension investments. 5% minus 3% inflation ( estimated) = 2%beeza650 said:

yes exactlyDullGreyGuy said:

Though that also assumes you dont increase your drawings as the thresholds for tax increase and assumes you're happy effectively reducing your spending each year as your income stays static but inflation increases prices cutting your spending power.Mark_d said:Suppose you pension pot is worth £1m at age 55. Suppose you pension pot grows at an average rate of 5% per year thereafter (after charges). Then you'll generally get £50k per year.If you withdraw less than £50k per year your fund will never run out.

I would absolutely keep up with the 40% bracket (although who knows what future taxation might look like). Also full state pension kicks in at 67 (today). The point about inflation is up to the gov really, if they don't increase the 40% bracket then yes, there'd be less to spending power.

I can't get my head round bonds/gilts, to get that 4% return don't you need to buy at point of issue otherwise there is an underlying market price factored into the buy price?It's just my opinion and not advice.0 -

Thanks for taking it off topic 1

-

OP - if you're 50 now, you can't start to draw from your pension until you are 57. Not sure you've clocked that?Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0

-

Rather than just using my spread sheet which looks at the one set of parameters I found there are a few modelling options out there. I have used https://firecalc.com/ others have mentioned https://www.cfiresim.com/ and https://ficalc.app/

For those unfamiliar the idea is to runs multiple simulations based on historical data, US biased and you can tune for state pension, investment styles when you stop working etc, Rather than giving you a yes/no answer you see how likely your model would have failed using real historical data points.

Well I think that's what it does.

0 -

Not necessarily - but they, normal gilts, are redeemed at par value £100 and that’s the important value. No problem buying over par if the yield is acceptable in a tax advantaged account. Income is taxed but there is no CGT on gilts so taxable accounts prefer low coupon higher capital gain gilts. Higher coupon is better for ISA and SIPP as no tax on coupons or gains in those.SouthCoastBoy said:5

Thks for that, so I guess I should look for gilts below par value. Are all gilts issued at par value £100FIREDreamer said:

You can buy TREASURY 4.5% 07/12/2042 (T42) under the par value of £100 meaning you have a gross redemption yield in excess of 4.5% (ignore the date of 4 September 2018 - that’s nonsense, this was priced over £150 at that date as yields were much lower).SouthCoastBoy said:

I'm hoping it isNedS said:

Oh dear, why would you accept the equity risk for a 3.5% return when you can get a ~4% return from government gilts with no risk? I fear your pessimism is overdone?SouthCoastBoy said:

Am a bit more pessimistic than that equity growth 3.5%, inflation 2.5%Albermarle said:

So in that case you need to look at the possible real growth of your pension investments. 5% minus 3% inflation ( estimated) = 2%beeza650 said:

yes exactlyDullGreyGuy said:

Though that also assumes you dont increase your drawings as the thresholds for tax increase and assumes you're happy effectively reducing your spending each year as your income stays static but inflation increases prices cutting your spending power.Mark_d said:Suppose you pension pot is worth £1m at age 55. Suppose you pension pot grows at an average rate of 5% per year thereafter (after charges). Then you'll generally get £50k per year.If you withdraw less than £50k per year your fund will never run out.

I would absolutely keep up with the 40% bracket (although who knows what future taxation might look like). Also full state pension kicks in at 67 (today). The point about inflation is up to the gov really, if they don't increase the 40% bracket then yes, there'd be less to spending power.

I can't get my head round bonds/gilts, to get that 4% return don't you need to buy at point of issue otherwise there is an underlying market price factored into the buy price?

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards