We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

What questions are asked by HMRC regarding NIC history when ringing up to claim SP?

Comments

-

Post up the following info and we can give you a heads up as to what you need to doCurrent weekly £££.pp amount accrued up to April 2023 or 2024, not all have been updated so please specify.

Number of full NI years 15-16 and earlier

Number of full NI years 16-17 and later

Tax year you reach state retirement

Any COPE amount. If you have "You've been in a contracted-out pension scheme" on your forecast then click

here https://www.tax.service.gov.uk/check-your-state-pension/account/cope whilst logged into your tax account

Years which show not full and prices

1 -

Wow-you folks on here are so helpful!

Below is as of today, so assume it's April 2024.

Thank you!!")

0 -

Which answers point 4 and maybe, but only maybe, point 1.There should be more below that box plus the rest of the info about your NI record.1

-

Hi again,molerat said:Post up the following info and we can give you a heads up as to what you need to doCurrent weekly £££.pp amount accrued up to April 2023 or 2024, not all have been updated so please specify.

Number of full NI years 15-16 and earlier

Number of full NI years 16-17 and later

Tax year you reach state retirement

Any COPE amount. If you have "You've been in a contracted-out pension scheme" on your forecast then click

here https://www.tax.service.gov.uk/check-your-state-pension/account/cope whilst logged into your tax account

Years which show not full and prices

So to summarise:- Current weekly £££.pp amount accrued up to April 2024 (maybe 2023 due to comment below - info not ready?) £173.89

- Number of full NI years 15-16 and earlier 21

- Number of full NI years 16-17 and later 0

BUT letter from HMRC in Aril 2024 says I have 25 qualifying years of NICs up to 5.4.24?! - Tax year you reach state retirement: 2024/25 in 10 days or so time!

- Any COPE amount: thanks so much for this! I had no idea where to find that.

Contracted Out Pension Equivalent (COPE)

Your COPE estimate is £13.61 a week

Years which show not full and prices:

2023 to 2024Your record for this year is not available yet2022 to 2023Year is not fullPay a voluntary contribution of £824.20 by 5 April 2029. This shortfall may increase after 5 April 2025.

2021 to 2022Year is not fullPay a voluntary contribution of £800.80 by 5 April 2028. This shortfall may increase after 5 April 2025.

2020 to 2021Year is not full2019 to 2020Year is not fullPay a voluntary contribution of £824.20 by 5 April 2026. This shortfall may increase after 5 April 2025.

2018 to 2019Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

2017 to 2018Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

2016 to 2017Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

2015 to 2016Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

2014 to 2015Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

2013 to 2014Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

2012 to 2013Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

2011 to 2012Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

2010 to 2011Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

2009 to 2010Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

2008 to 2009Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

2007 to 2008Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

2006 to 2007Year is not fullPay a voluntary contribution of £824.20 by 5 April 2025. This shortfall may increase after 5 April 2025.

- Pay a voluntary contribution of £795.60 by 5 April 2027. This shortfall may increase after 5 April 2025.

0 -

Apologies. I was just compiling that info. Much appreciatedmolerat said:Which answers point 4 and maybe, but only maybe, point 1.There should be more below that box plus the rest of the info about your NI record.0 -

BUT letter from HMRC in Aril 2024 says I have 25 qualifying years of NICs up to 5.4.24?

At the very bottom of your NI record is there not a statement "You have x(4?) full years up to April yyyy" ?

Are there also not statements "Estimate based on your NI contributions up to 5 April 2023/24" and "You can improve your forecast ........ the most you can improve your forecast to is £xxx.xx" ?

So on the information provided you need 8 more years to reach the full amount. You could safely purchase up to 5 pre 2016 years but they only add £5.65 each compared to £6.32 for a post 2016 year. 7 post 2016 years will take you to £218.13, the 8th adding the final £3.07. So your best option would be in order of importance / cost - 20-21, 21-22, then the 5 22-23 and 16-17 to 19-20 then if you want to go the whole hog one from pre 2016 as that will be cheaper than 23-24 (£907.40) and although it doesn't fully give as much as a post 2016 year it will still only add the necessary £3.07.

1 -

Hi 'Molerat', That's very kind of you.molerat said:BUT letter from HMRC in Aril 2024 says I have 25 qualifying years of NICs up to 5.4.24?At the very bottom of your NI record is there not a statement "You have x(4?) full years up to April yyyy" ?

Are there also not statements "Estimate based on your NI contributions up to 5 April 2023/24" and "You can improve your forecast ........ the most you can improve your forecast to is £xxx.xx" ?

So on the information provided you need 8 more years to reach the full amount. You could safely purchase up to 5 pre 2016 years but they only add £5.65 each compared to £6.32 for a post 2016 year. 7 post 2016 years will take you to £218.13, the 8th adding the final £3.07. So your best option would be in order of importance / cost - 20-21, 21-22, then the 5 22-23 and 16-17 to 19-20 then if you want to go the whole hog one from pre 2016 as that will be cheaper than 23-24 (£907.40) and although it doesn't fully give as much as a post 2016 year it will still only add the necessary £3.07.

I've found this summary. Any good?"You have:25 years of full contributions

3 years to contribute before 5 April 2024

22 years when you did not contribute enough"

I've found a 2022 forecast with the sort of figures

you seek. Will see if I can find a more recent one!0

you seek. Will see if I can find a more recent one!0 -

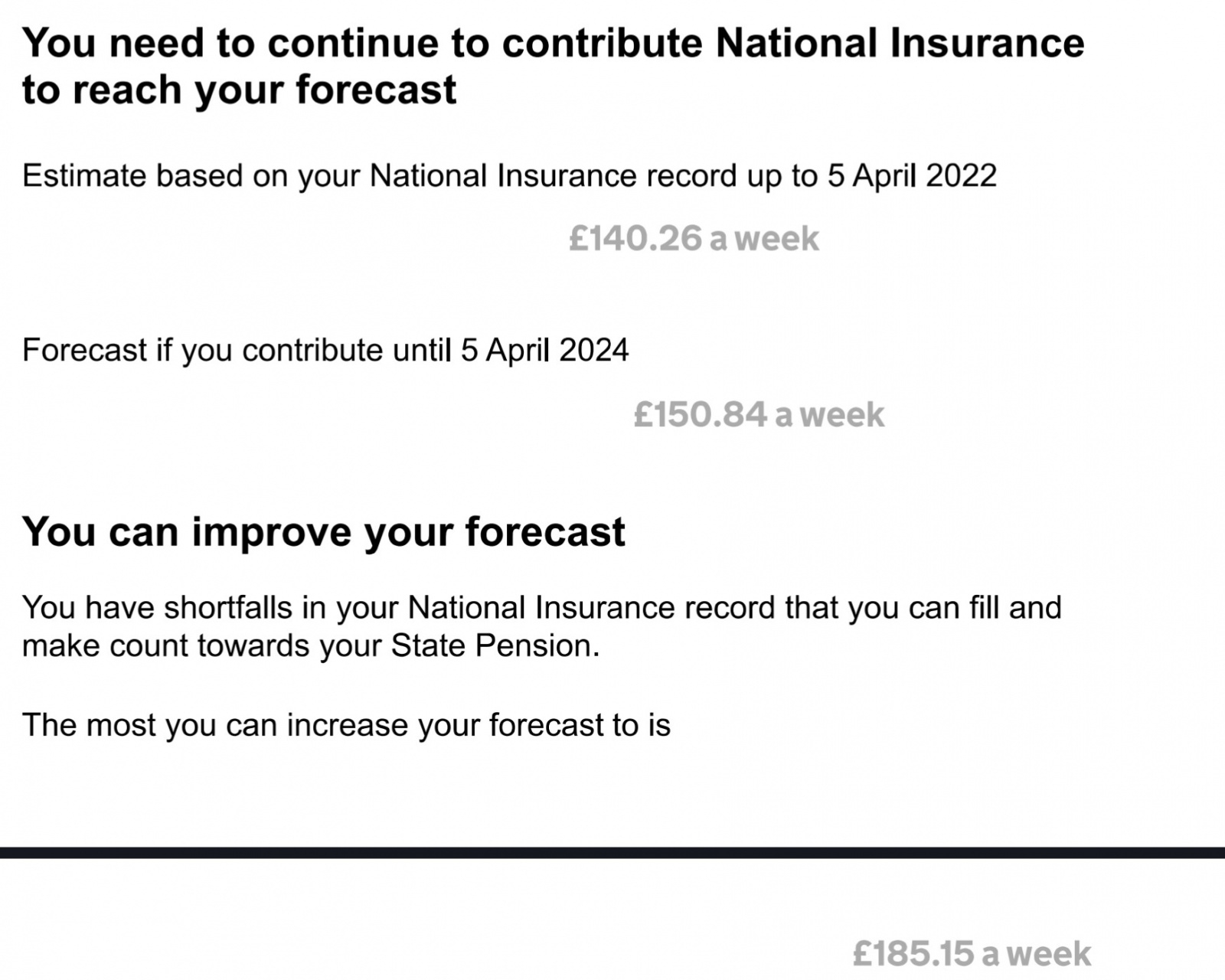

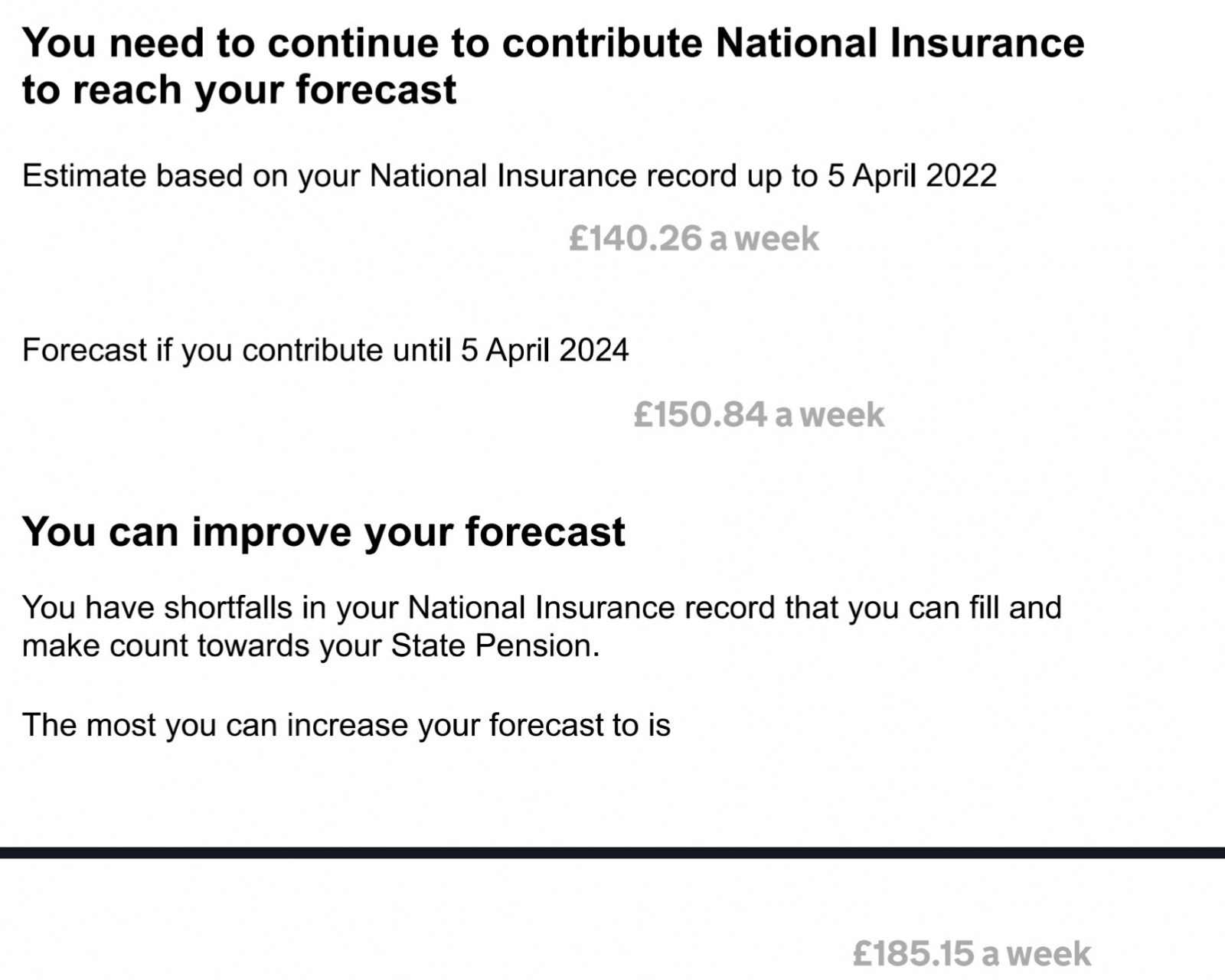

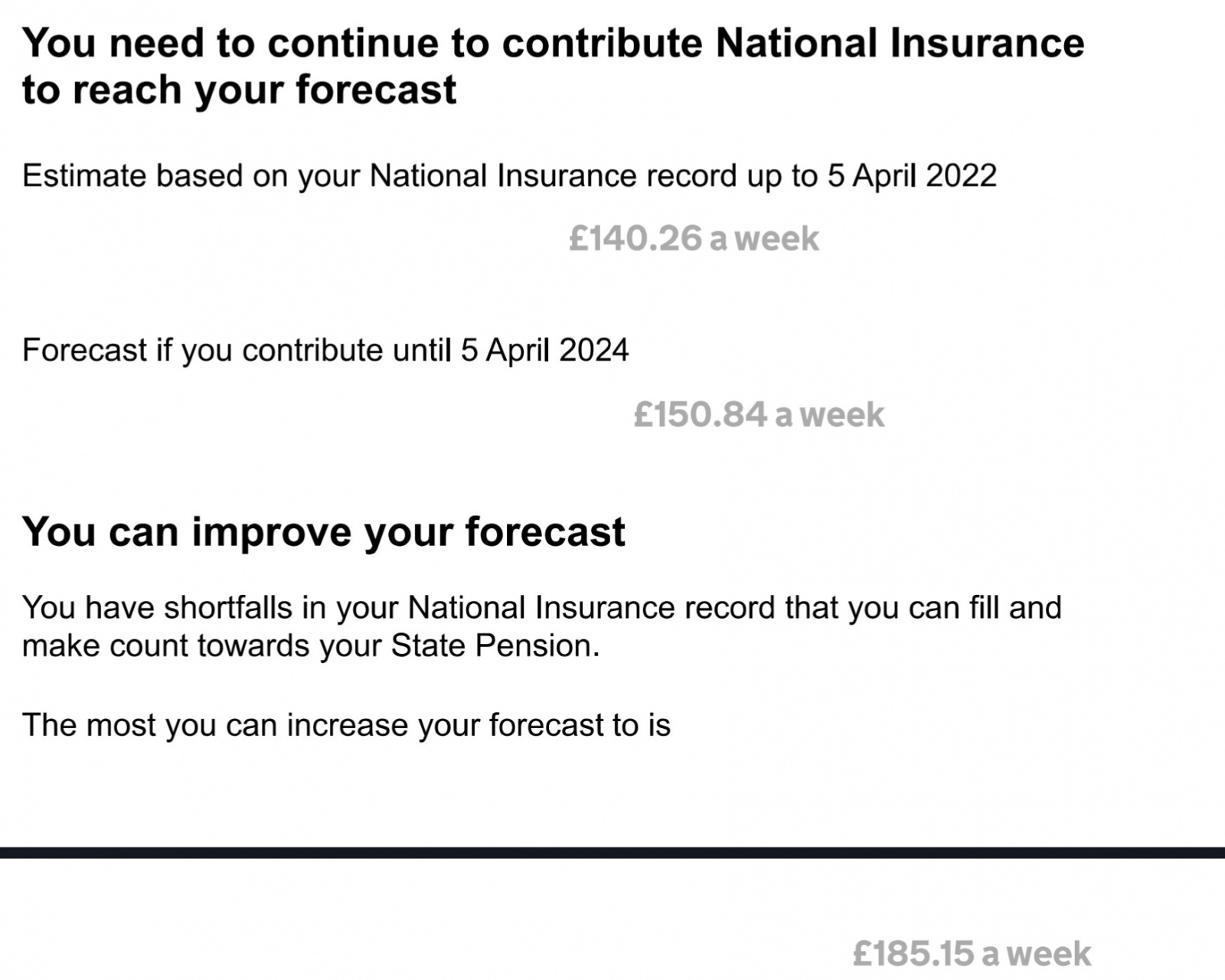

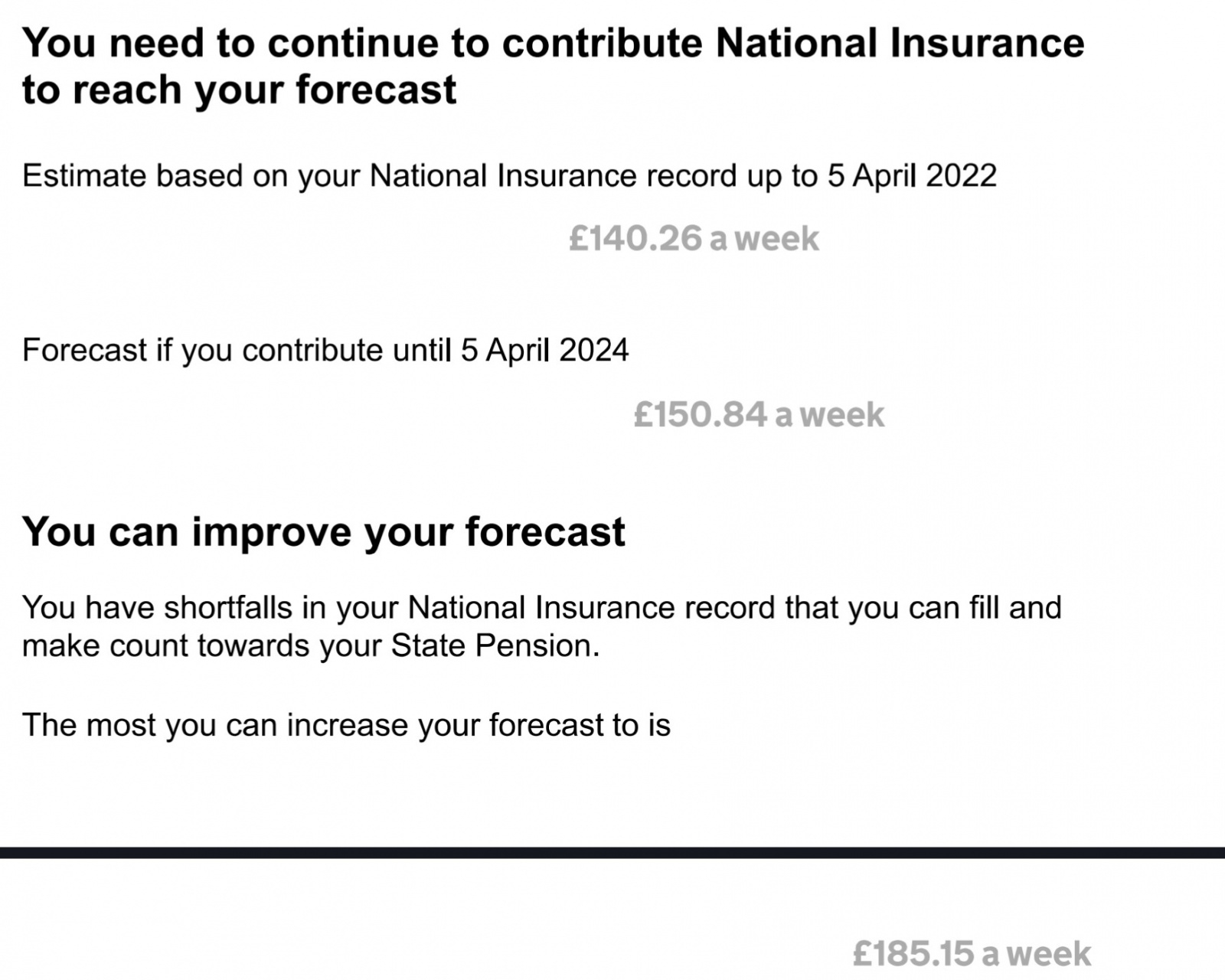

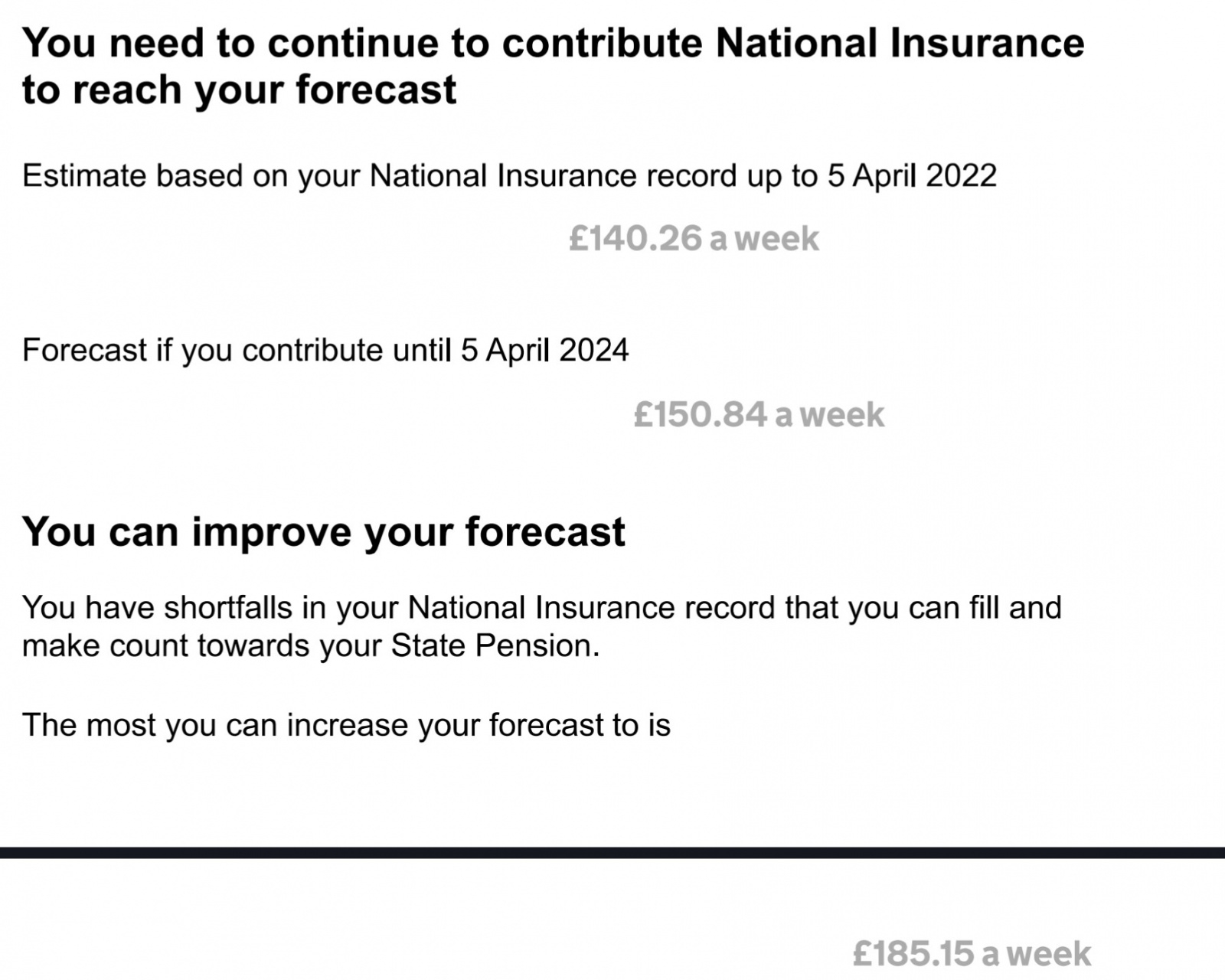

Estimate to 5.4.22 £140.26/wk

Estimate to 5.4.22 £140.26/wk

Forecast if you contribute to 5.4.24 £150.84/wk

Most you can increase is to £185.15/wk

(2022 figs)

0 -

Found 5.4.23 figs:

£167.57/wk

£173.89/wk

£221.20/wk0 -

As soon as I saw that 22 figure I worked out that £140.26 then is £167.57 now and you would reach £173.89, £6.32 more, with 23-24 contributions. I think a lot of information is removed from the forecast once you get into the 4 month claiming window.So to modify my earlier postSo on the information provided you need 9 more years to reach the full amount. You could safely purchase up to 5 pre 2016 years but they only add £5.65 each compared to £6.32 for a post 2016 year. 7 post 2016 years will take you to £211.81 plus 1 pre 2016 takes you to £217.46 with another adding the final £3.74. So your best option would be in order of value / cost - 20-21, 21-22, then the 5 22-23 and 16-17 to 19-20, 1 pre 2016 then if you want to go the whole hog another one from pre 2016 as that will be cheaper than 23-24 (£907.40) and although it doesn't fully give as much as a post 2016 year it will still only add the necessary £3.74. If not going the whole way buying 23-24 instead of a pre 2016 year would give you an extra 67p for an additional £83.20 cost.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards