We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

DB Pension quotation value keeps decreasing each year

carrspaints

Posts: 81 Forumite

Hi all. I am now 60. For the past 3-years, I have requested pension quotations from Willis Towers Watson, with a stated retirement age of 65. That is when my deferred pension would ordinarily start paying out. However, this value keeps decreasing each year for each quotation I have received. In 2022, the value was £15,890. In 2023, it was £15,616 and today it is £15,407. I've emailed WTW, but the response I got did not address my email query to them at all - standard for WTW.

Can anyone explain why these values keep going down, when the Scheme

pension built up between 5 April 1997 and 5 April 2006 is increased by

price inflation up to 5% for each year between the date of leaving the

Scheme and

NRD, and 2.5% between 5 April 2006 and 5 April 2009? Thanks.

0

Comments

-

Well an obvious one may be that WTW got the numbers wrong. Not that I have any proof that might be possible of course. It's just that they are a very large company dealing with a wide variety of pension schemes some of which are astoundingly complex. And no doubt people move around doing admin on various schemes so might, perhaps, use the wrong process/spreadsheet/calculator/dates. Perhaps.I’m a Forum Ambassador and I support the Forum Team on Debt Free Wannabe, Old Style Money Saving and Pensions boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.

Click on this link for a Statement of Accounts that can be posted on the DebtFree Wannabe board: https://lemonfool.co.uk/financecalculators/soa.php

Check your state pension on: Check your State Pension forecast - GOV.UK

"Never retract, never explain, never apologise; get things done and let them howl.” Nellie McClung

⭐️🏅😇🏅🏅🏅0 -

Last year they would have assumed 2.5% and 5% revaluation for this year plus all future years.carrspaints said:Hi all. I am now 60. For the past 3-years, I have requested pension quotations from Willis Towers Watson, with a stated retirement age of 65. That is when my deferred pension would ordinarily start paying out. However, this value keeps decreasing each year for each quotation I have received. In 2022, the value was £15,890. In 2023, it was £15,616 and today it is £15,407. I've emailed WTW, but the response I got did not address my email query to them at all - standard for WTW.Can anyone explain why these values keep going down, when the Scheme pension built up between 5 April 1997 and 5 April 2006 is increased by price inflation up to 5% for each year between the date of leaving the Scheme and NRD, and 2.5% between 5 April 2006 and 5 April 2009? Thanks.

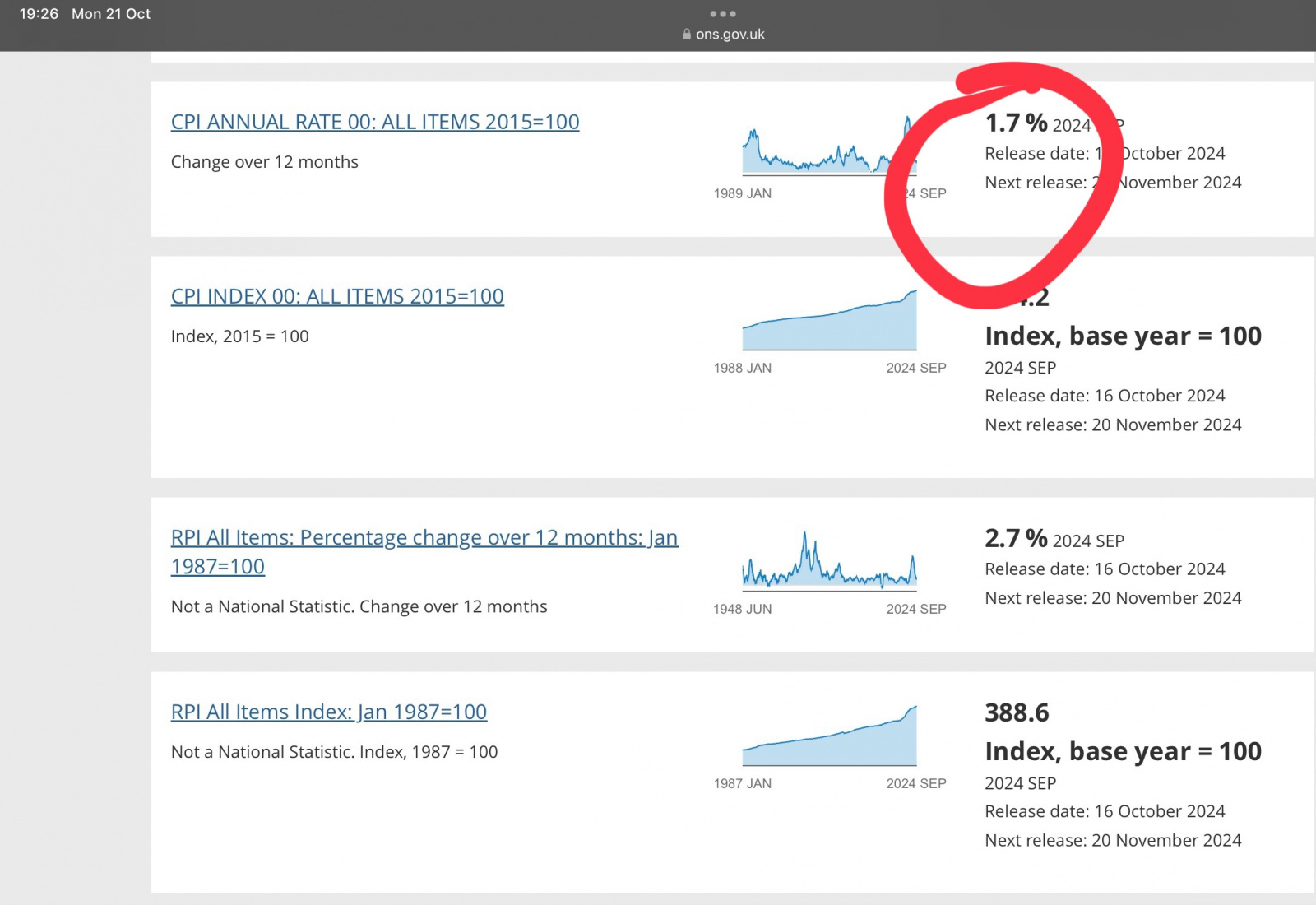

However inflation last year was only 1.7% - so last years pension has increased by 1.7% and not 2.5% or 5% hence the reduction in the value assumed at age 65 - the last year has increased by less than expected. Perhaps simikar happened between 2022 and 2023.

Do you have the full quotes - dates provided / effective dates and the split between the 2.5% and 5% pensions?1 -

You've a capped inflation linked benefit. If its gone down in projection then they'd predicted that inflation was higher than it turned out to be and/or they are predicting future inflation isn't going to be as high as they'd previously assumed.0

-

@FIREDreamer. The quotes I have don't split out the increases on the pension payout between 2 & 5%. They only provide the value if not taking 25% tax free, and a 2nd option if taking 25% tax free.Also, surely the value I receive each year includes the 2.5% & 5% adjustments for that year? (If inflation is higher) The value of the retirement payout value would therefore increase if that is the case. So if the following year, the increase is only 1.7% because of low inflation, it shouldn't have an impact on the previous year's value, or quote. Or have I misunderstood how this is calculated.By the way, was UK inflation last year only 1.7%?? I thought it would have been far greater than that. Thanks,0

-

Cpi was 1.7%, rpi was 2.7%.carrspaints said:@FIREDreamer. The quotes I have don't split out the increases on the pension payout between 2 & 5%. They only provide the value if not taking 25% tax free, and a 2nd option if taking 25% tax free.Also, surely the value I receive each year includes the 2.5% & 5% adjustments for that year? (If inflation is higher) The value of the retirement payout value would therefore increase if that is the case. So if the following year, the increase is only 1.7% because of low inflation, it shouldn't have an impact on the previous year's value, or quote. Or have I misunderstood how this is calculated.By the way, was UK inflation last year only 1.7%?? I thought it would have been far greater than that. Thanks,

0 -

Because they are based on projections of what inflation will be between now and when you reach age 65. By definition projections can be - and often are - wrong. In 2022 inflation was roaring away, but has reduced dramatically since then.carrspaints said:Hi all. I am now 60. For the past 3-years, I have requested pension quotations from Willis Towers Watson, with a stated retirement age of 65. That is when my deferred pension would ordinarily start paying out. However, this value keeps decreasing each year for each quotation I have received. In 2022, the value was £15,890. In 2023, it was £15,616 and today it is £15,407. I've emailed WTW, but the response I got did not address my email query to them at all - standard for WTW.Can anyone explain why these values keep going down, when the Scheme pension built up between 5 April 1997 and 5 April 2006 is increased by price inflation up to 5% for each year between the date of leaving the Scheme and NRD, and 2.5% between 5 April 2006 and 5 April 2009? Thanks.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

CPI increase for 2024 DB pension revaluation was 6.7%, capped at the relevant 5%/2.5%, 10.1% for 2023, and 3.1% for 2021. All use the 12 month increase for year before (2024 increase is 12 months up to Sep 2023 for example). 1.7% increase will be used for 2025's revaluation, so in theory should be replacing (e.g) a 2.5% value they maybe assuming currently for next year.FIREDreamer said:

Last year they would have assumed 2.5% and 5% revaluation for this year plus all future years.carrspaints said:Hi all. I am now 60. For the past 3-years, I have requested pension quotations from Willis Towers Watson, with a stated retirement age of 65. That is when my deferred pension would ordinarily start paying out. However, this value keeps decreasing each year for each quotation I have received. In 2022, the value was £15,890. In 2023, it was £15,616 and today it is £15,407. I've emailed WTW, but the response I got did not address my email query to them at all - standard for WTW.Can anyone explain why these values keep going down, when the Scheme pension built up between 5 April 1997 and 5 April 2006 is increased by price inflation up to 5% for each year between the date of leaving the Scheme and NRD, and 2.5% between 5 April 2006 and 5 April 2009? Thanks.

However inflation last year was only 1.7% - so last years pension has increased by 1.7% and not 2.5% or 5% hence the reduction in the value assumed at age 65 - the last year has increased by less than expected. Perhaps simikar happened between 2022 and 2023.

Do you have the full quotes - dates provided / effective dates and the split between the 2.5% and 5% pensions?

2.5% cap applies from 2009 , your pension pre-2009 cannot revalue at anything other than capped 5%. In-payment, this is different and is split Pre and Post 2005 instead.carrspaints said:Hi all. I am now 60. For the past 3-years, I have requested pension quotations from Willis Towers Watson, with a stated retirement age of 65. That is when my deferred pension would ordinarily start paying out. However, this value keeps decreasing each year for each quotation I have received. In 2022, the value was £15,890. In 2023, it was £15,616 and today it is £15,407. I've emailed WTW, but the response I got did not address my email query to them at all - standard for WTW.Can anyone explain why these values keep going down, when the Scheme pension built up between 5 April 1997 and 5 April 2006 is increased by price inflation up to 5% for each year between the date of leaving the Scheme and NRD, and 2.5% between 5 April 2006 and 5 April 2009? Thanks.

I therefore cannot see that assumed inflationary increases is the reason, no Scheme should logically be using assumptions over and above the statutory revaluation requirements of 5% / 2.5% which has been the case for the last 2 years. It would seem to me there is something else going on.

The latest value, i could understand as 1.7% will likely be lower than the values they assume for each year. But the idea that a company like WTW has updated their calculations in the 3 working days it's been since that CPI was released seems doubtful.0 -

Thanks for all of your replies. TBH, I have no idea what is going on, and I have givem up with WTW. For anyone who has ever tried dealing with them, they'll know that getting any logical, or reasonable response from WTW is unlikely. Getting a response at all can be considered a victory, albeit a pyrrhic victory (at best).0

-

If you're projecting to a fixed date in the future, then what inflation assumption is used is trivially important when revaluation is capped - e.g. assume 3%pa for the duration in deferment, and pension subject to higher revaluation will hold value in real terms but pension subject to lower revaluation won't. If either actual or assumed inflation then rises over time, the projected figure discounted back to current will fall (assuming those rises are ones over the cap).Tommyjw said:2.5% cap applies from 2009 , your pension pre-2009 cannot revalue at anything other than capped 5%. In-payment, this is different and is split Pre and Post 2005 instead.

I therefore cannot see that assumed inflationary increases is the reason, no Scheme should logically be using assumptions over and above the statutory revaluation requirements of 5% / 2.5% which has been the case for the last 2 years. It would seem to me there is something else going on.

The latest value, i could understand as 1.7% will likely be lower than the values they assume for each year. But the idea that a company like WTW has updated their calculations in the 3 working days it's been since that CPI was released seems doubtful.

In the OP's case, presumably the leap in inflation that occurred a few years back wasn't assumed previously. Ergo the quoted figure (projected to NRA then discounted back) would fall if there weren't enough below-cap years 'banked' to smooth the new above-cap ones out.0 -

This post reminds me of a few friends who experienced the same.

They had good DB pensions.

IIRC, there was three scenarios.

1. Some people stayed employed and contributed to the scheme and their pension target for say age 65 went up every year due to pensionable pay rises and extra years service or contributions. Unfortunately pensionable pay rises were zero or tiny due to various rules and the extra yearly service was only a small amount. So their age 65 target only went up slowly.

2. Some staff left employment or just opted out of the old scheme(joined the new DC scheme) and made no more payments in to that scheme and the 65 targets increased more than people who continued to activity contribute to to the old scheme due the inflation or the deferment rules. It looked pretty strange, pay in less and get more.

3. Some staff just activated the scheme and then enjoyed the inflation rises ever year and the ones who stayed employed often filled up the new DC scheme aggressively and trying to reduce income tax.

It all looked very strange.

Note, the staff who left the old DB scheme and joined the new DC actually got better death in service outcome if they expired in that zone, winners and loosers it looked to me, just like the budget this month.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards