We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Debt charges on a house we are buying

Comments

-

Which is fine if the price covers all of the secured debts. I presume from the context that it doesn't, and the seller doesn't have the cash to make up the balance.peterhjohnson said:As I understand it (and I may be wrong), the seller's solicitor:

1. Finds out the redemption amount for each charge

2. Gives each charge owner an undertaking to pay off the charge from the sale proceeds in return for the creditor releasing the charge.

3. You (+ maybe your lender) pay the seller's solicitor in the normal way at completion

4. Seller's solicitor pays off the debts

5. Seller's solicitor pays the seller the balance.1 -

…which means that any one of the charge holders who isn’t getting paid in full can block the sale by refusing to remove their charge. The seller has to persuade them that either they will get more money by agreeing to the sale eg if they would get some of their money, or to release the charge in return for a repayment plan.user1977 said:

Which is fine if the price covers all of the secured debts. I presume from the context that it doesn't, and the seller doesn't have the cash to make up the balance.peterhjohnson said:As I understand it (and I may be wrong), the seller's solicitor:

1. Finds out the redemption amount for each charge

2. Gives each charge owner an undertaking to pay off the charge from the sale proceeds in return for the creditor releasing the charge.

3. You (+ maybe your lender) pay the seller's solicitor in the normal way at completion

4. Seller's solicitor pays off the debts

5. Seller's solicitor pays the seller the balance.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.2 -

Can you post an example of one of the charges from the title deed (minus any identifying info)? There are two types of charging orders. One is an interim charging order, which does not have to be repaid on completion, and a full charging order which does. The wording on the actual deed will help identify which it is.1

-

gazfocus said:Can you post an example of one of the charges from the title deed (minus any identifying info)? There are two types of charging orders. One is an interim charging order, which does not have to be repaid on completion, and a full charging order which does. The wording on the actual deed will help identify which it is.

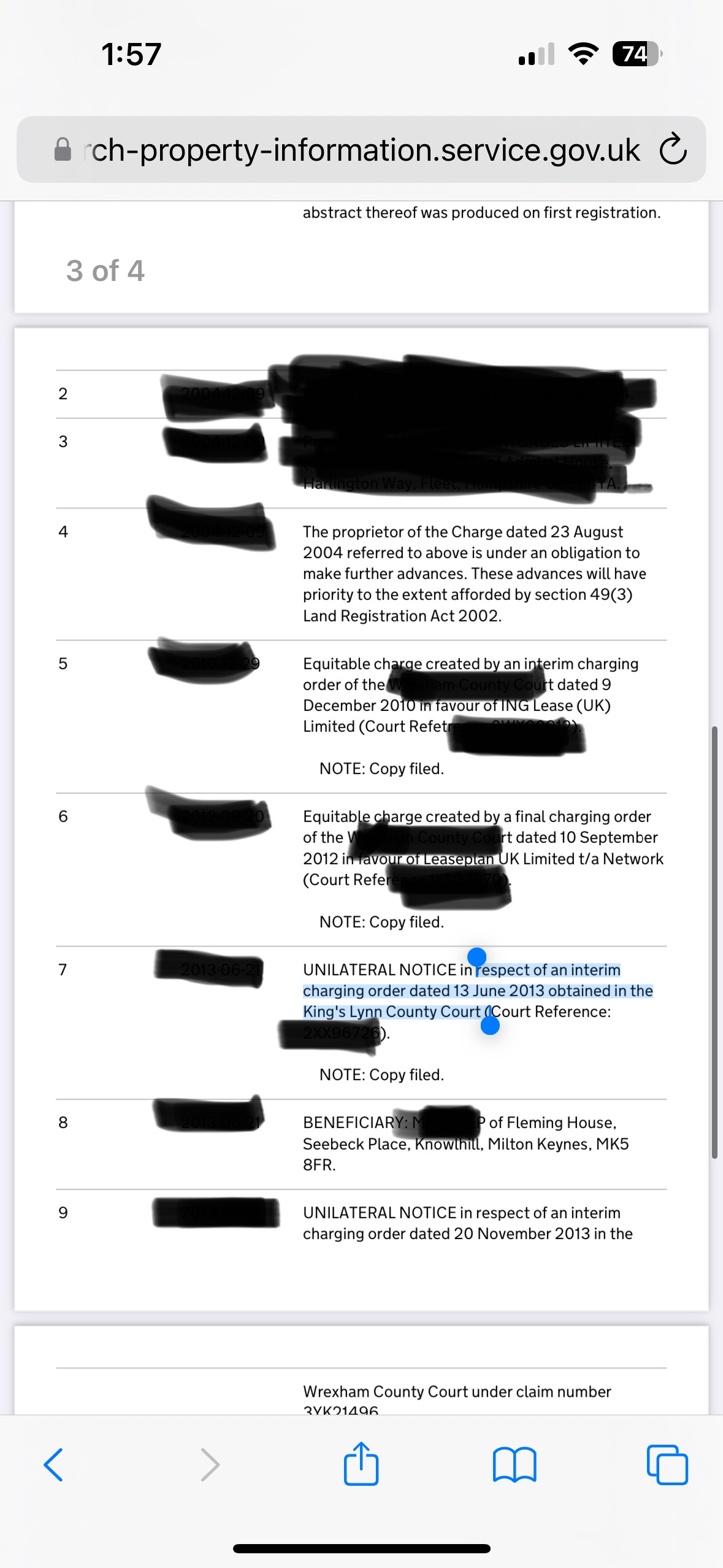

These are some of the orders- some have beneficiary and some say unilateral notice. No idea what that means.

These are some of the orders- some have beneficiary and some say unilateral notice. No idea what that means.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards