We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Taking 25% taxfree cash lumpsum out of large DC pension pot

Comments

-

-

Thanks SarahPosted on bogleheads as well :Cheers

0 -

Interest, as far as Vanguard is concerned.BlisteringBarnacles said:Thanks SarahPosted on bogleheads as well :Cheers

Full details.: UK investor : US VMFXX Vanguard Federal Money Market Fund - Interest or dividend ?1 -

Thanks for confirming HMRC can pre populate seft assessment form.Sarahspangles said:

HMRC have been pre-populating interest details for Self Assessment and Simple Assessment for a while. Though I don’t think I’d want to rely on this.Dazed_and_C0nfused said:I think that must be new, haven't heard of pre-population of interest details before.

And some people simply prefer not to have their tax code messed with for things like tax underpaid. Not very MSE but it suits some people!I agree I’d rather not have my notice of coding messed with! Right now as someone on PAYE I’m owed tax from 2023-24 as I’m waiting on my P800 and my notice of coding for 2024-25 has been updated in real time for interest received this tax year to date and assumes this is additional to, not instead of the interest received last year. So I’m overpaying tax this year as well.

To reconfirm I just got all the statements I have accounts with issued in May or June approximately, these showed the interest amounts and it looked to me any returns or increase in MMFs are just labeled interest and the self assessment eform just appeard to have the same data, and obviously not rocked science.

0 -

RogerPensionGuy said:

250K could be plonked in gilts if that suited.Because Individual gilts are capital gains tax free, correct ? But then you would have to pay tax on the "coupon" , i.e interest payment, right ? I saw a couple of articles about low coupon gilt but it went over my head. I have seen yieldgimp but could not make any sense of the columns.Thanks.0 -

Gilts look at bit strange, but I read a bit, looked in here and a few good videos on YouTube~pensioncraft especially cones to mind.BlisteringBarnacles said:RogerPensionGuy said:

250K could be plonked in gilts if that suited.Because Individual gilts are capital gains tax free, correct ? But then you would have to pay tax on the "coupon" , i.e interest payment, right ? I saw a couple of articles about low coupon gilt but it went over my head. I have seen yieldgimp but could not make any sense of the columns.Thanks.

My take.

A person whants to enjoy capital growth, but rather not pay on CGT on it.

Gilts prices do go up and down, look at historic graphs.

Gilts pay a coupon or interest call it.

So a simple example.

A gilt that matures in October 2027 and pays back £1 is 90 pence today, maybe it pays 0.125% interest or coupon.

So buy it today, buy as many as you like.

Twice a year you will receive interest or coupon payment, this will be half of 0.125% so 0.0625% approximately, this interest is potentially taxable if above the £500 or 1K allowance per annum.

If you just do nothing, you get back £1 in October 2027 and that 10 pence is not taxed and you stop getting the interest or coupon.

Over the next 3 years the price of the gilt will tend to slide up to £1, if it jumps up in value during this period, you can sell it if you like the numbers.

However price can slide down, look at the Truss effects in 2022, so selling in these zones look nasty, however Truss effect was a nice time to buy.

In my opinion these gilts really work well for big tax payers of say 40,45% Income or CGT incomes over the limit.

So the people in the paragraph about are happy to pay a bit over the odds as they win more if you see what I mean.

CGT unfortunately has gone from 12.6K IIRC to just 3K in a few years, so gilts look more attractive to the upper income or wealth people.

Getting back to YouTube, look for gilt ladder, basically pick a few years to maturaty gilts, buy if you like, get very small interest or coupon typically and get back all them £1s on maturity.

Some gilts can be over a £1 and may pay big interest if you like, maybe £1.08 matures in 3 years and pays 6% or similar, they are issued and people buy them, so obviously suits some people.

It's a shame these vehicles are not as effective for lower incomes or wealth people like premium bonds as an example.

I hope the above is close to helpful or accurate.

Enjoy all the reading and YouTube videos.

Cheers Roger.3 -

This is an extreme example. Priced over £150 in 2020 maturing at £100 in 2071. Yield to maturity was about 1% - a terrible investment. A much better proposition now.RogerPensionGuy said:

Gilts look at bit strange, but I read a bit, looked in here and a few good videos on YouTube~pensioncraft especially cones to mind.BlisteringBarnacles said:RogerPensionGuy said:

250K could be plonked in gilts if that suited.Because Individual gilts are capital gains tax free, correct ? But then you would have to pay tax on the "coupon" , i.e interest payment, right ? I saw a couple of articles about low coupon gilt but it went over my head. I have seen yieldgimp but could not make any sense of the columns.Thanks.

My take.

A person whants to enjoy capital growth, but rather not pay on CGT on it.

Gilts prices do go up and down, look at historic graphs.

Gilts pay a coupon or interest call it.

So a simple example.

A gilt that matures in October 2027 and pays back £1 is 90 pence today, maybe it pays 0.125% interest or coupon.

So buy it today, buy as many as you like.

Twice a year you will receive interest or coupon payment, this will be half of 0.125% so 0.0625% approximately, this interest is potentially taxable if above the £500 or 1K allowance per annum.

If you just do nothing, you get back £1 in October 2027 and that 10 pence is not taxed and you stop getting the interest or coupon.

Over the next 3 years the price of the gilt will tend to slide up to £1, if it jumps up in value during this period, you can sell it if you like the numbers.

However price can slide down, look at the Truss effects in 2022, so selling in these zones look nasty, however Truss effect was a nice time to buy.

In my opinion these gilts really work well for big tax payers of say 40,45% Income or CGT incomes over the limit.

So the people in the paragraph about are happy to pay a bit over the odds as they win more if you see what I mean.

CGT unfortunately has gone from 12.6K IIRC to just 3K in a few years, so gilts look more attractive to the upper income or wealth people.

Getting back to YouTube, look for gilt ladder, basically pick a few years to maturaty gilts, buy if you like, get very small interest or coupon typically and get back all them £1s on maturity.

Some gilts can be over a £1 and may pay big interest if you like, maybe £1.08 matures in 3 years and pays 6% or similar, they are issued and people buy them, so obviously suits some people.

It's a shame these vehicles are not as effective for lower incomes or wealth people like premium bonds as an example.

I hope the above is close to helpful or accurate.

Enjoy all the reading and YouTube videos.

Cheers Roger.

1 -

A nice graphic above, just imagine getting 268K TFLS in November 2019 and plonking that 268K in to that gilt in December 2019 and thinking you may like to sell them gilt five years later in November 2024.FIREDreamer said:

This is an extreme example. Priced over £150 in 2020 maturing at £100 in 2071. Yield to maturity was about 1% - a terrible investment. A much better proposition now.RogerPensionGuy said:

Gilts look at bit strange, but I read a bit, looked in here and a few good videos on YouTube~pensioncraft especially cones to mind.BlisteringBarnacles said:RogerPensionGuy said:

250K could be plonked in gilts if that suited.Because Individual gilts are capital gains tax free, correct ? But then you would have to pay tax on the "coupon" , i.e interest payment, right ? I saw a couple of articles about low coupon gilt but it went over my head. I have seen yieldgimp but could not make any sense of the columns.Thanks.

My take.

A person whants to enjoy capital growth, but rather not pay on CGT on it.

Gilts prices do go up and down, look at historic graphs.

Gilts pay a coupon or interest call it.

So a simple example.

A gilt that matures in October 2027 and pays back £1 is 90 pence today, maybe it pays 0.125% interest or coupon.

So buy it today, buy as many as you like.

Twice a year you will receive interest or coupon payment, this will be half of 0.125% so 0.0625% approximately, this interest is potentially taxable if above the £500 or 1K allowance per annum.

If you just do nothing, you get back £1 in October 2027 and that 10 pence is not taxed and you stop getting the interest or coupon.

Over the next 3 years the price of the gilt will tend to slide up to £1, if it jumps up in value during this period, you can sell it if you like the numbers.

However price can slide down, look at the Truss effects in 2022, so selling in these zones look nasty, however Truss effect was a nice time to buy.

In my opinion these gilts really work well for big tax payers of say 40,45% Income or CGT incomes over the limit.

So the people in the paragraph about are happy to pay a bit over the odds as they win more if you see what I mean.

CGT unfortunately has gone from 12.6K IIRC to just 3K in a few years, so gilts look more attractive to the upper income or wealth people.

Getting back to YouTube, look for gilt ladder, basically pick a few years to maturaty gilts, buy if you like, get very small interest or coupon typically and get back all them £1s on maturity.

Some gilts can be over a £1 and may pay big interest if you like, maybe £1.08 matures in 3 years and pays 6% or similar, they are issued and people buy them, so obviously suits some people.

It's a shame these vehicles are not as effective for lower incomes or wealth people like premium bonds as an example.

I hope the above is close to helpful or accurate.

Enjoy all the reading and YouTube videos.

Cheers Roger.

I guess a nicer example was buying a shorter term gilt during the Truss effect, enjoy any coupon/interest and sell it when felt appropriate.

I'll try putting a picture on this post below if I can.

***

https://markets.businessinsider.com/news/currencies/charts-liz-truss-resignation-uk-markets-gilts-pound-dollar-treasurys-2022-10

0 -

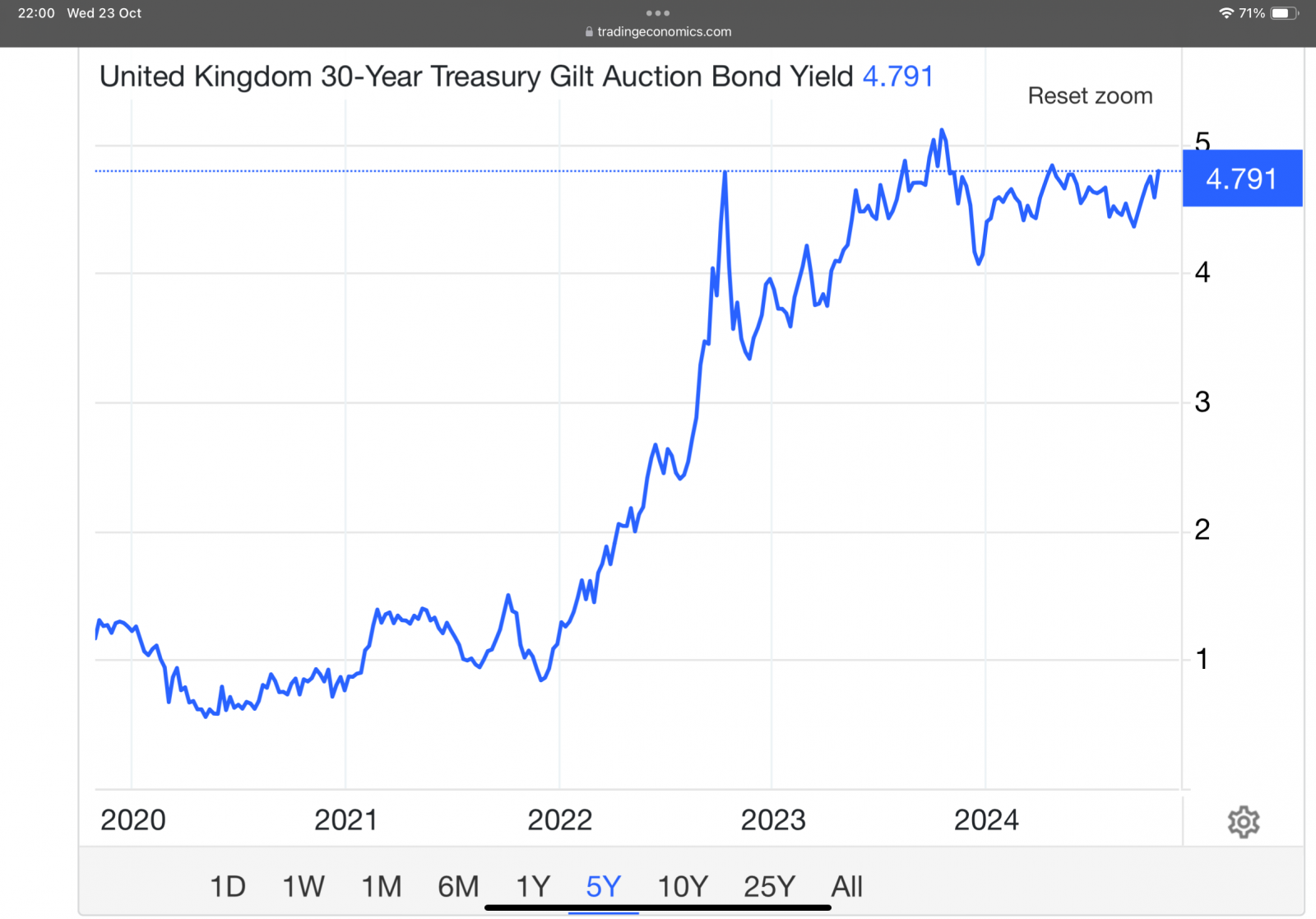

Thought I posted this pic yesterday but it seems to have vanished. This shows the increase in 30 year gilt yields in the last five years…

1 -

Regarding Vanguard Money market fund, in the post below, EdSwippet has clarified that the dividend distributions will be taxed as bank interest.EdSwippet said:

Interest, as far as Vanguard is concerned.BlisteringBarnacles said:Thanks SarahPosted on bogleheads as well :Cheers

Full details.: UK investor : US VMFXX Vanguard Federal Money Market Fund - Interest or dividend ?But I have couple of questions about Money market Accumulation funds held in taxable account. Roger has clarified below that the "growth" in such funds will also be taxed as interest ( unless it uses complex instruments such as swaps etc : Eg : CSH2 ETF). But how is this "growth" calculated ? If you dont sell the fund/ETF, is there no tax to pay ?RogerPensionGuy said:https://monevator.com/money-market-funds/#:~:text=Money market funds will often,and shares ISA, or pension.

***

My experience is filling out my 2023/2024 online self assessment.

I got my yearly statements from my banks, NS&I and GIA accounts, I'm 99% sure all money market funds income or growth was called interest.Examples would be :1) If I hold for example "BlackRock Cash Class D - Accumulation (GBP)" in my Interactive Investor UK Taxable account.2) I hold the ETF ZPR1 : "SPDR Bloomberg 1-3 Month T-Bill UCITS ETF (Acc)" US dollar denominated ETF in my offshore Interactive Brokers US dollar account on which I pay UK tax on arising basis ?Thanks

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards