We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Unfair Modification to IVA?

Hi all,

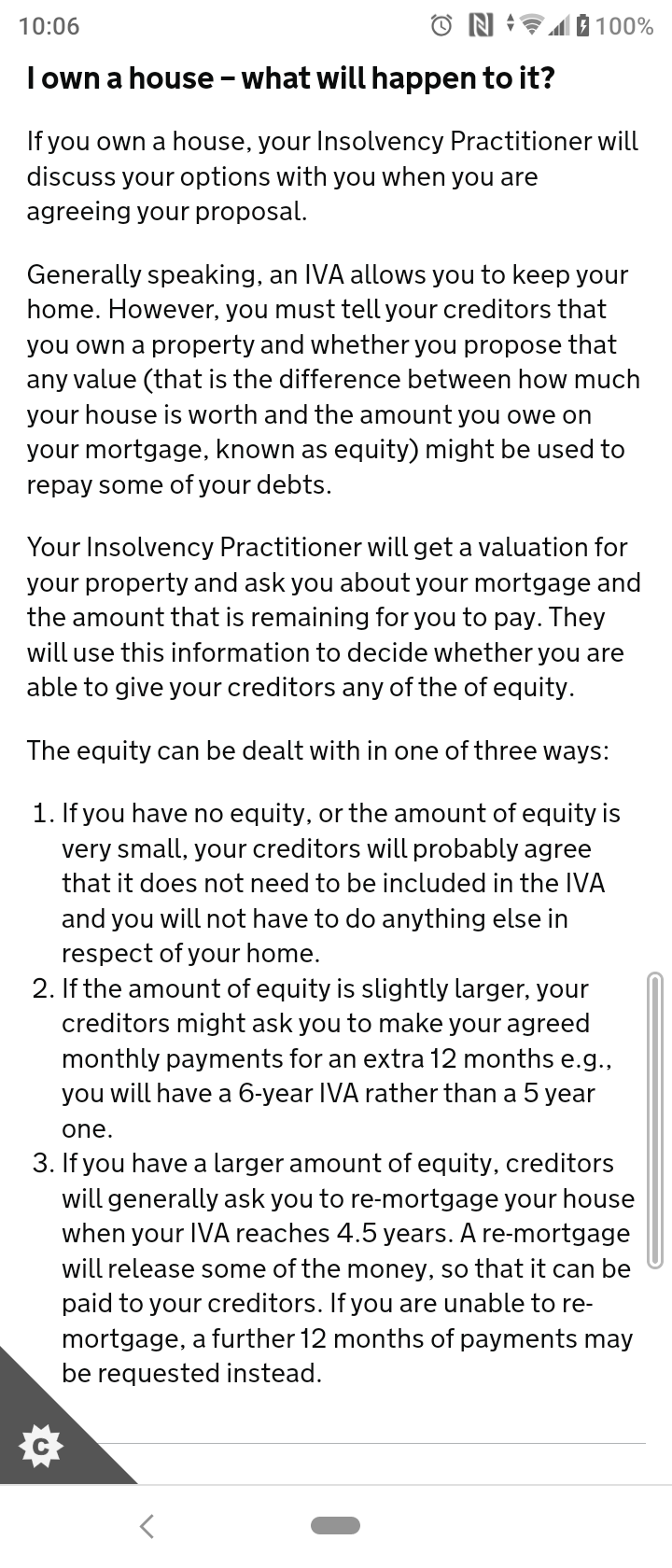

We are currently looking to go through an IVA - We have approx 54k of debt and our family home we'd rather not lose. A large portion of the debt is to HMRC (self employed tax debts)

We've been going through with The Advice Center for our IVA, and negotiations have come to a close, with HMRC adding a modification which essentially negates the whole point of an IVA:

"If the debtor is unable to release the equity within the property(s) by month 60 of the arrangement the property(s) shall be placed for sale on the open market with a minimum of two professional agents at their recommended asking price(s). If open market sale(s) are not achieved within a further 6 months (by 60 of the arrangement) taking into account the vending agents’ full recommendations, the Supervisor shall immediately make arrangements with the debtor for the sale by public auction of their property(s). Net sale proceeds not exceeding 100 pence in the pound plus statutory interest to be introduced to the arrangement following sale of the property(s)."

As an IVA nukes our credit rating, I'm not hopeful for us to be able to remortgage and release the equity they're after.

This follows other modifications like pushing it to 72 months, and increasing the proposed monthly payable amount.

I'm really not sure what to do now. If I was to approach another IVA Practitioner, are they likely to be able to negotiate a different deal?

I've approached Business Helpline and was told I'd get a call back, I've been dealing with citizens advice as well but it seems like my agent goes on annual leave every other week.

Feeling very stuck at the moment.

Any advice at all please?

Thanks!

We are currently looking to go through an IVA - We have approx 54k of debt and our family home we'd rather not lose. A large portion of the debt is to HMRC (self employed tax debts)

We've been going through with The Advice Center for our IVA, and negotiations have come to a close, with HMRC adding a modification which essentially negates the whole point of an IVA:

"If the debtor is unable to release the equity within the property(s) by month 60 of the arrangement the property(s) shall be placed for sale on the open market with a minimum of two professional agents at their recommended asking price(s). If open market sale(s) are not achieved within a further 6 months (by 60 of the arrangement) taking into account the vending agents’ full recommendations, the Supervisor shall immediately make arrangements with the debtor for the sale by public auction of their property(s). Net sale proceeds not exceeding 100 pence in the pound plus statutory interest to be introduced to the arrangement following sale of the property(s)."

As an IVA nukes our credit rating, I'm not hopeful for us to be able to remortgage and release the equity they're after.

This follows other modifications like pushing it to 72 months, and increasing the proposed monthly payable amount.

I'm really not sure what to do now. If I was to approach another IVA Practitioner, are they likely to be able to negotiate a different deal?

I've approached Business Helpline and was told I'd get a call back, I've been dealing with citizens advice as well but it seems like my agent goes on annual leave every other week.

Feeling very stuck at the moment.

Any advice at all please?

Thanks!

0

Comments

-

Hi. I work for CA and they do give me a lot of annual leave, which I use through the summer. Don't think it's me though.

I agree that clause is unreasonable, and is probably something that HMRC is likely to stick to, whichever IP approaches them.

It may be worth a second approach though. Have TAC given up or are they prepared to argue?

How much equity is in the property? Is it jointly owned? Is the debt solely in your name?1 -

Are the debts joint or just yours?

Is the property jointly owned?

Does your partner have their own income?

0 -

yes ivas can have modification rules, here's the general rules

Christians Against Poverty solved my debt problem, when all other debt charities failed. Give them a call !! ( You don't have to be a Christian ! )

https://capuk.org/contact-us0 -

How much do you owe HMRC?

They will not agree to something they feel isn't a big enough payment and if pushed they will make you bankrupt.

You need a serious financial rethink very quickly.If you go down to the woods today you better not go alone.0 -

As you have discovered HMRC are not going to write off debt when you have equity in your property (rightly so imo). The majority of people don't get a choice when it comes to paying tax before the mortgage so that is the approach HMRC will take in this situation.0

-

Thanks for the replies guys.

The IVA was going through in both mine and my wifes name as some of the debts are joint. However the HMRC debt is in my name, and is about £30k.

Weve been down other paths such as trying to remortgage but as our credit limit has been reached, no one will give any additional lending.

Regarding the stuff stu12345_2 has posted, that was our general understanding too, in that if we cannot release equity they will push the IVA for another year. However for them to even accept the IVA they've requested:

72 month term

An increase in what we pay per month to the IVA

This clause that will basically leave us homeless if we can't release equity. No further extension.

I don't know how much equity is in the property exactly. At a guess I'd say £70k? But currently I cannot touch it without selling the house.

I have 2 young kids, I'm not driving a lamborghini or sailing yachts. Just a normal bloke whos income dropped, ended up picking up a second job that's paye (so I am paying some tax) and made sure my kids were fed and our other bills were paid.

The house is the only thing we really have, and it's not something I can let go of easily.0 -

It feels like they're giving up. I've asked them to go back and see what alternatives they'd consider like make the IVA even longer etc. But not heard anything since.fatbelly said:Hi. I work for CA and they do give me a lot of annual leave, which I use through the summer. Don't think it's me though.

I agree that clause is unreasonable, and is probably something that HMRC is likely to stick to, whichever IP approaches them.

It may be worth a second approach though. Have TAC given up or are they prepared to argue?

How much equity is in the property? Is it jointly owned? Is the debt solely in your name?0 -

Surely if you owe HMRC £30K you must have had some idea you were not paying enough tax and didn't you save for the tax?

If things do go pear shaped you could end up having to sell your house to get hold of the money.If you go down to the woods today you better not go alone.0 -

Yes it's built up over a number of years and due to financial issues, family issues etc. I'd prioritised our welfare. I'm working 2 jobs currently, my wife is on maternity leave, so we have no spare cash and have no where we could move to if we sold the house, as most of the equity would go to the debts, and our family is basically none existent any more.Grumpelstiltskin said:Surely if you owe HMRC £30K you must have had some idea you were not paying enough tax and didn't you save for the tax?

If things do go pear shaped you could end up having to sell your house to get hold of the money.

I hold my hands up that I've not made the best decisions leading to this point. What I don't need is hindsight, just how I can possibly move forward from here without losing our home.0 -

TAC are one of the IVA pushers we see a lot of here. They typically want their 4-figure fees for filling in a couple of forms, not an extended negotiation with HMRC

I can see that with your share of equity being 35k and the HMRC debt being 30k then they are playing hardball and may consider issuing a statutory demand to which you would suggest a voluntary charge.

A couple of thoughts

Would they consider a monthly instalment direct to them of whatever the iva payment was?

Would a more customer focused IP like Payplan or one local to you, put in a bit more effort to get an IVA over the line?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards