We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Sense Check Please!

Comments

-

The usual method is to take out £16,760 , by taking a UFPLS payments, which is 25% tax free and 75% taxable ( the 75% = exactly the standard personal allowance ) .

However if your way suits you, then it is fine. The only thing is you will have to take two separate payments, and you will have to wait a week or two after requesting the tax free cash, before you can request the taxable payment.

In both cases you may well find the taxable payment is taxed, and you have to claim it back.

0 -

do you use a provider that has separate pots for crystallised and uncrystallised funds? Some of the usual suspects operate a notional split eg ii.

HL I believe does the separate potsI’m a Senior Forum Ambassador and I support the Forum Team on the Pensions, Annuities & Retirement Planning, Loans

& Credit Cards boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com.

All views are my own and not the official line of MoneySavingExpert.0 -

I currently have my pension in my workplace Peoples Pension as it keeps it easy for salary sacrifice. When I retire I plan to switch to one of the "usual suspects" yet tbc.

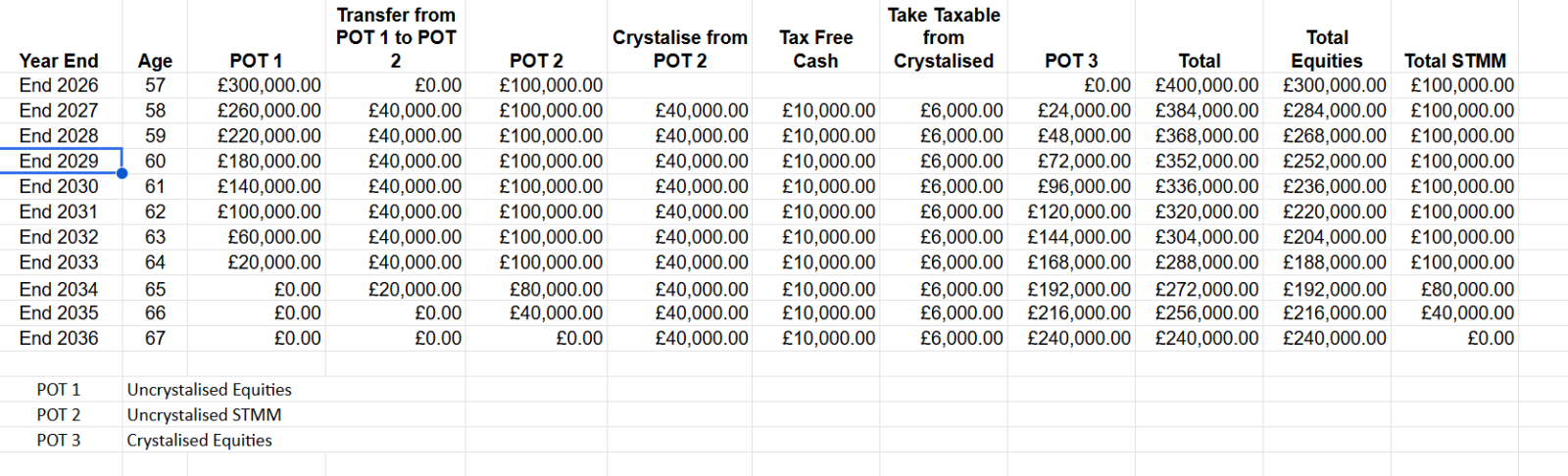

So how does the following sound. I would need to have 3 "Pots". Pot 1 starts at £300k uncrystallised and is invested in a global fund tbc 60 or 80 or 100% equities. Pot 2 starts at £100k uncrystallised in STMM. Pot 3 is the crystallised pot which can remain untouched for the foreseeable future, so can remain in 100% equities. I would therefore balance Pots 1 & 2 every year to ensure that £100k remains in Pot 2, something like this:

Does this seem a sensible approach, do any of you do anything similar? Are there providers who can accommodate this strategy?

0 -

I do not think ( maybe wrong) that you can have multiple pension pots at the same provider. Even if you could you would not be able to keep transferring money from one to the other.

You might have to have three separate providers.

0 -

What's the purpose of "Pot 2" in the above ? How is it different from having a single uncrystallised pot containing (initially) 300k in global fund and 100k in STMM, and then just moving investments within the single pot ?

0 -

The initial thinking behind it was to find a way to de-risk the £160k that I will be withdrawing over the next 10 years, whilst leaving the remaining amount in more adventurous investments, but it clearly needs a re-think!

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards