We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Investment need in FTSE All World Index Fund/ETF to earn £20,000 a year

Comments

-

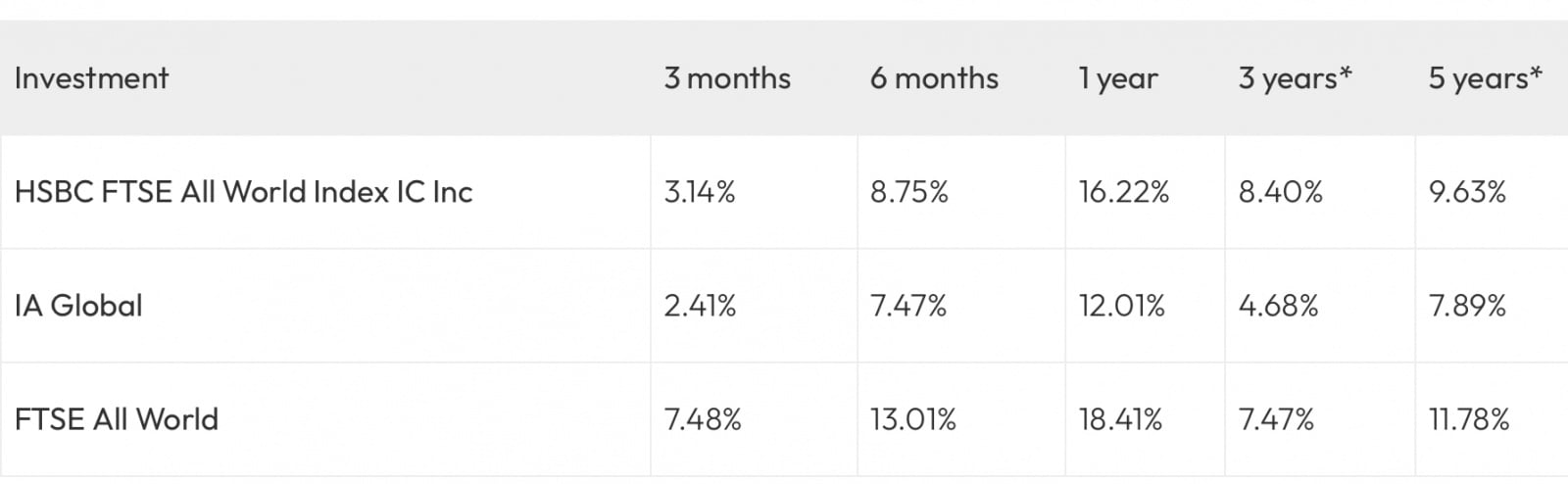

Here’s some examples over 5 years…..

0 -

Hopefully your investing knowledge extends beyond copying what other people are talking about on social media. The markets can be an easy way of losing money, .Tonys101 said:

I don't get this 1.6% your tallking about where is that number coming from?1 -

Might be correct for the data google's looking at. Possibly slightly outdated compared to the fund factsheet you showed earlier, possibly a different find type (inc vs acc)Tonys101 said: google says this just wanted other peoples advice/information

google says this just wanted other peoples advice/information

0 -

Using a Total Return type approach a starting point would be to apply the usual safe withdrawal rules of thumb that will give you an excellent chance of providing an index linked income for at least 30 years. So just divide 20k by 4%. So you will need £0.5M - of course that is a ridiculously simple "napkin" estimate and there are is an enormous list of caveats, but it's a start.Tonys101 said:Hi

How much would i need invested in a FTSE All World Index Fund/ETF to earn £20,000 a year?

Also how much would i need to leave in my investment if I took out £20,000 a year taking into account market downturns.

I never plan to have all my money in one investment and currently don't.

my portfolio is made up of currently

Cash

Shares of one company (Gotten from a employee share save scheme)

a portfolio of crypto

HSBC all world index fund

Just looking for some information to work offAnd so we beat on, boats against the current, borne back ceaselessly into the past.0 -

How much you can take out of a portfolio is not as simple as looking at the average annualized returns. You have to think about yearly variations in return and inflation. The table you posted does not show the times when there were significant losses. So research "Safe Withdrawal Rates".Tonys101 said:google says this just wanted other peoples advice/information And so we beat on, boats against the current, borne back ceaselessly into the past.1 -

The 1.6% is the dividend yield. That is strictly speaking the income you can generate each year without selling any shares and taking some capital gains...if you did that it would be a "Total Return" approach.Tonys101 said:I am simply asking , how much would I need to have invested to earn £20,000 in a world index fund/etf

I don't get this 1.6% your tallking about where is that number coming from?

HSBC all world is up this much see below

Basicly what is the average it goes up by each yearAnd so we beat on, boats against the current, borne back ceaselessly into the past.1 -

Don't rely on that as an indication of future returnsTonys101 said:google says this just wanted other peoples advice/information

a) 20 years ago takes you back to just after one of the worst periods on the stockmarket for generations. So, it only includes the recovery from that.

b) 10 years back disregards the credit crunch falls but includes some of its recovery.

c) 5 years back ignores the Q4 2018 falls but includes their recovery

d) last year ignores the 2022 falls but includes the recovery.

its a bit of a coincidence that the timescales all line up like that but each is painting a better picture than had they includes a year or several years earlier.

Plus, as mentioned, this is total return and that is not what you were asking in the first post of this thread.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.5 -

I cannot get the data for the FTSE All World but the FTSE World will not be wildly different.....Tonys101 said:I am simply asking , how much would I need to have invested to earn £20,000 in a world index fund/etf

I don't get this 1.6% your tallking about where is that number coming from?

HSBC all world is up this much see below

Basicly what is the average it goes up by each year

The average annual return since 1/1/2001 is 8.1% which would mean £246K to return £20K

But the returns from an index can be highly volatile. Looking at 5-year periods:

Years / Average annual return/ average Lump sum to return £20K/year

1/1/2001-31/12/2005 : negative: you would never make a £20K gain.

1/1/2006/-31/12/2011 : 4.5% : £444K

1/1/2006-31/12/2010 : 5.9% : £339K

1/1//2011- 31/12/2015 : 8.6% : £232K

1/1/2016 - 31/12/2020 : 14.9% : £134K

There is no reason why the returns for the next 24 years or so should have an average close to 8.1%. Future returns are just random within wide bounds.

0 -

Drawing a fixed regular income from the total return of a stock market index fund is a very poor approach because if the stock market crashes 50% at the start and takes a few years to recover you damage your asset valuation early selling high quantities of fund units at low prices. It would be preferable to use a multi-asset portfolio to manage the risk of needing to sell low.3

-

Here are some charts which show the problem of using high risk investments to fund income.

They show £1666.67 pm being drawn from 1st January 2000 to date.

One major limitation - this is £1666.67 pm level. In reality, you would be increasing that draw periodically

First chart is starting at £600k:

In the first few months, you are thinking everything is great. You are drawing £20k p.a. and your value has gone up. By winter 2003 you are leaking brown stuff big time as your value has more than halved. Things get better for a few years before it goes down further.

Now lets change your starting balance to £400k:

Nothing has changed apart from the starting amount. But you get a very different chart And you start the spiral of erosion and have run out of money by 2024.

Now lets change it to £300,000. Recent returns data may make you think that is plenty to get £20k level income from but lets see:

Well, you didn't make it to 2014, let alone 2024.

Lets just see how that £400k works if we introduce bonds/gilts etc and take sector average in the mixed investment sectors:

Risk works very nicely when you are paying in, but when you are drawing out, the larger drops in negative periods hurt more when you are drawing and can cause a terminal decline. This is why you mitigate those periods by using lower-risk strategies such as cash floats, bucketing, yielding bias, or adjusting your draw in negative years (which is nice in theory but usually not practical).

And remember, this was £20k p.a. without change. In reality, you would have increased your draw due to inflation.I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.12

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards