We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Debt help

Comments

-

what are the interest rates, what is the £250 other income, is it child maintenance ??, from what you have posted you could meet the min payments and with £450 left over.

but I'd say your groceries are too low for 3 people, you have left no money spent on entertainment, clothing or haircuts for 3 people..

you are living too frugally.

you have gave yourself no emergency fund.

you need to up your expenses., that is allowed

if you could then chuck some of the £450 excess left over which will be probably lower after upping expenses, you don't have to live so frugally. then the balances will drop faster.

but I think if you make only the min payments it will take far longer than you desire to drop the balances.

ultimately you want the interest stopped, but you aren't insolvent, you can meet the min payments. you will struggle to persuade your creditors youre insolvent and can't meet min payments

you will be able to tell them you have a change of circumstances at present and allow you room and time to recalculate your new finances.

if you went to a debt charity, they would see . that you could meet your mim repayments and still have money left over.

I don't think you are looking at any debt repayment plan yet, you are looking at chucking everything you can into the highest interest rate card and the min on the other cards whilst not living so frugally at the same time

Christians Against Poverty solved my debt problem, when all other debt charities failed. Give them a call !! ( You don't have to be a Christian ! )

https://capuk.org/contact-us0 -

firstly don't use these cards at all, cut them up. is there any possibility of doing a balance transfer to lower interest credit cards

if you presented this SAO to a debt charity or your creditors they would see you can meet your obligations on your repayments and more

. you will struggle to ask them to stop interest permanently

unless you seriously up your expenses in places I suggest you won't qualify at present for an organised official debt repayment plan or stopping of interest.

snowball everything you can into the highest interest card, clear that then attack the other cards in the same method.

but I'd ask you to DO A NEW SAO with money spent on clothes, emergency fund, haircuts , entertainment and up that grocery amount and see what you truly have left to give to creditors.

you can easily allow for £70 entertainment, £380 for shopping,( which includes cleaning products and toiletries)£60 for clothes, £5O for haircuts.( this is expected expenses spent and a debt charity and your creditors allows and accepts this)

the higher it realistically goes , then there is a chance of a debt management plan ( which should stop interest) or even a debt relief order which would clear your debts in 12 months

like I said living as frugally as you are doing could backfire on you, and as crazy as it sounds the more you have in realistic acceptable expenses the better chance of a formal debt solution

( many times the poorer you are (whilst living a reasonable quality of life, which you aren't) then the better chance of a formal or informal debt solution.)

and again it's the large amount of benefits and other income you get could actually do more harm in proving youre insolvent, as crazy as it may sound

let's see what others think

Christians Against Poverty solved my debt problem, when all other debt charities failed. Give them a call !! ( You don't have to be a Christian ! )

https://capuk.org/contact-us0 -

a little footnote why should avoid an IVA, an IVA would take all your £815 excess( but probably less after you include your new upped expenses) per month for 5 years,

that is only if you qualify,! as you are on benefits too. you need a regular set income amount for 5 years and benefits in your life could change and your income. and if anything goes up , more income , more benefits, then you have to pay another 50% of that that to into your plan !!

you could easily pay back much more than the £22000 you have in debt. IVA fees are around £4000 to £8000. which are added into your total owed.

so if you failed, to pay during it,stopped your IVA in the 5 years, you are left owing your debt balance and these fees too.

an IVA works for someone with a home , that doesn't want to go bankrupt , looks to pay only £100 min a month and owes a lot more than you do and has an income without benefits that is totally regular and guaranteed for 5 years

a debt relief order DRO would suit you far better than an IVA, that is only if you qualify for a DRO!Christians Against Poverty solved my debt problem, when all other debt charities failed. Give them a call !! ( You don't have to be a Christian ! )

https://capuk.org/contact-us0 -

Have added items that you need to include.Loyalroyal_2 said:[font=courier new][b]Statement of Affairs and Personal Balance Sheet[/b][b]Household Information[/b]Number of adults in household........... 1Number of children in household......... 2Number of cars owned.................... 0[b]Monthly Income Details[/b]Monthly income after tax................ 1150Partners monthly income after tax....... 0Benefits................................ 1120Other income............................ 250[b]Total monthly income.................... 2520[/b][b]Monthly Expense Details[/b]Mortgage................................ 0Secured/HP loan repayments.............. 0Rent.................................... 800Management charge (leasehold property).. 0Council tax............................. 237 - assume that you have applied for single person discount? Have you checked for any further reduction?Electricity............................. 167 - check your meters now. Are you in credit or deficitGas..................................... 0Oil..................................... 0Water rates............................. 32Telephone (land line)................... 0Mobile phone............................ 31 - OKTV Licence.............................. 15Satellite/Cable TV...................... 0Internet Services....................... 78 - this is high research optionsGroceries etc. ......................... 240 - this is just about doable if you need a budget month but £360 is more sustainableClothing................................ 0 - 2 teens needs more than this even if you go for charity shops plus new undies. £60.per monthPetrol/diesel........................... 0Road tax................................ 0Car Insurance........................... 0Car maintenance (including MOT)......... 0Car parking............................. 0Other travel............................ 20 - do you live within walking distance of everything?Childcare/nursery....................... 0Other child related expenses............ 30Medical (prescriptions, dentist etc).... 0 - even if you are all NHS registered you need £10.per month each.Pet insurance/vet bills................. 0Buildings insurance..................... 0Contents insurance...................... 12 - goodLife assurance ......................... 0 you have two kids. Does your job offer any death in service benefits, pensions?Other insurance......................... 0Presents (birthday, christmas etc)...... 15Haircuts................................ 0 - you need this £10 per month eachEntertainment........................... 0 £40 for the familyHoliday................................. 0 £60 per month, even if it only covers school tripsEmergency fund.......................... 0 £30 per month so you can replace the cooker or microwave is it blows up. Or thereGym..................................... 28[b]Total monthly expenses.................. 1705[/b][b]Assets[/b]Cash.................................... 0House value (Gross)..................... 0Shares and bonds........................ 0Car(s).................................. 0Other assets............................ 0[b]Total Assets............................ 0[/b][b]No Secured nor Hire Purchase Debts[/b][b]Unsecured Debts[/b]Description....................Debt......Monthly...APRCredit card ...................10000.....162.......NaNCredit card ...................5885......130.......NaNCredit card ...................6549......73........NaN[b]Total unsecured debts..........22434.....365.......- [/b][b]Monthly Budget Summary[/b]Total monthly income.................... 2,520Expenses (including HP & secured debts). 1,705Available for debt repayments........... 815Monthly UNsecured debt repayments....... 365[b]Amount left after debt repayments....... 450[/b][b]Personal Balance Sheet Summary[/b]Total assets (things you own)........... 0Total HP & Secured debt................. -0Total Unsecured debt.................... -22,434[b]Net Assets.............................. -22,434[/b][i]Created using the SOA calculator at www.LemonFool.co.uk.Reproduced on Moneysavingexpert with permission, using other browser.[/i][/font]

Your existing budget isn't sustainable. You need to include everything that that you need to spend each year, even if you haven't spent it since your break up. Other wise you'll have nothing with which to pay when things "crop up." And no access to credit.

You have two teens. They don't come cheap and you can bet that school will be asking for money for activities. They need clothing, it is reasonable to pay for one regular activity and they need some entertainment so they can socialise. Bored kids can get into trouble, kids who can't join mates get depressed etc. They may not get the flash trainers but you need to offer a half decent life.

And just to add that right now you need to think about winter. Things like draught exclusion pay for themselves in one year and make life much more pleasant. If necessary, you can make paper matches from free newspapers to fill gaps at skirtings etc. You need to be prepared to heat the person, so look for things like throws, second duvets, clothes you can layer (start with slightly undersized base layers and build up), rain proof gear, shoes and wellies, a warm coat each and hot water bottles. Thermos flasks can be bought in chazzers sometimes.If you've have not made a mistake, you've made nothing0 -

what about your 19 yr old son, does he work earn a wage, if not, then job seekers allowance, maybe he's at college with a bursary. any money he gets , he would be expected to contribute to household income and thus list what % he gives you as another fom of income into the house budget

as the debt charity and creditors would also expect that as he is actually classed as an adult, even though he's 19.

I also see your rent is high, I presume a private rental, check your tenancy agreement to see if any form of insolvency affects your tenancy, eg bankruptcy, a DRO.,

don't worry you're not at that stage.

you are in limbo land, not poor enough for a debt management plan, DRO or bankruptcy, but not rich enough to pay off these credit cards at a fast rate to clear them in a speedy fashion( interest is the killer)

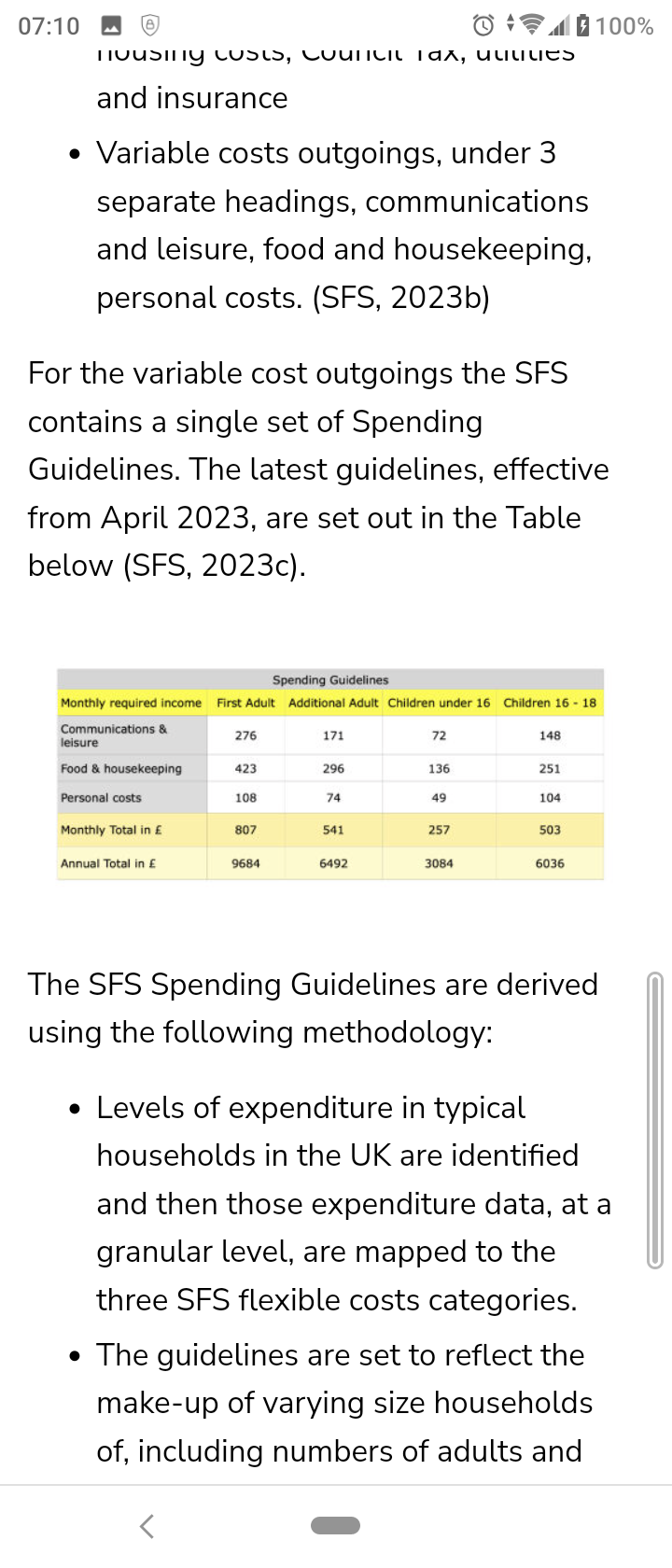

that's why I asked for a fresh SAO , a realistic one, not living like a nun or a hermit, so up all your flexible expenses,for the full family , it's a household outgoings, not just your own costs, clothes, shopping, gifts, emergency fund,haircuts, other travel such as going out in bus train to visit places, then a leisure amount to spend once you get there etc, and see what position you really are in

I attach the acceptable max limits in flexible expenses and you will see you are underspending

Christians Against Poverty solved my debt problem, when all other debt charities failed. Give them a call !! ( You don't have to be a Christian ! )

https://capuk.org/contact-us0 -

[font=courier new][b]Statement of Affairs and Personal Balance Sheet[/b][b]Household Information[/b]Number of adults in household........... 1Number of children in household......... 2Number of cars owned.................... 0[b]Monthly Income Details[/b]Monthly income after tax................ 1150Partners monthly income after tax....... 0Benefits................................ 850Other income............................ 262[b]Total monthly income.................... 2262[/b][b]Monthly Expense Details[/b]Mortgage................................ 0Secured/HP loan repayments.............. 0Rent.................................... 797Management charge (leasehold property).. 0Council tax............................. 237Electricity............................. 167Gas..................................... 0Oil..................................... 0Water rates............................. 35Telephone (land line)................... 0Mobile phone............................ 31TV Licence.............................. 15Satellite/Cable TV...................... 0Internet Services....................... 78Groceries etc. ......................... 360Clothing................................ 60Petrol/diesel........................... 0Road tax................................ 0Car Insurance........................... 0Car maintenance (including MOT)......... 0Car parking............................. 0Other travel............................ 40Childcare/nursery....................... 0Other child related expenses............ 30Medical (prescriptions, dentist etc).... 10Pet insurance/vet bills................. 10Buildings insurance..................... 0Contents insurance...................... 12Life assurance ......................... 10Other insurance......................... 0Presents (birthday, christmas etc)...... 15Haircuts................................ 10Entertainment........................... 50Holiday................................. 60Emergency fund.......................... 30(Unnamed monthly expense)............... 0gym..................................... 28appliance cover......................... 25[b]Total monthly expenses.................. 2110[/b][b]Assets[/b]Cash.................................... 0House value (Gross)..................... 0Shares and bonds........................ 0Car(s).................................. 0Other assets............................ 0[b]Total Assets............................ 0[/b][b]No Secured nor Hire Purchase Debts[/b][b]Unsecured Debts[/b]Description....................Debt......Monthly...APRcredit card....................10000.....162.......17credit card....................5885......130.......20credit card....................6549......0.........25Loan ..........................611.......18........29[b]Total unsecured debts..........23045.....310.......- [/b][b]Monthly Budget Summary[/b]Total monthly income.................... 2,262Expenses (including HP & secured debts). 2,110Available for debt repayments........... 152Monthly UNsecured debt repayments....... 310[b]Amount short for making debt repayments. -158[/b][b]Personal Balance Sheet Summary[/b]Total assets (things you own)........... 0Total HP & Secured debt................. -0Total Unsecured debt.................... -23,045[b]Net Assets.............................. -23,045[/b][i]Created using the SOA calculator at www.stoozing.com.Reproduced on Moneysavingexpert with permission, using other browser.[/i][/font]0

-

My son works but is only part time he pays me £12 a week , we are in a housing association property , can't claim for single occupancy as son is here,

posted new soa its more accurate than my first one

what happens next?

0 -

why is the £6549 card not getting any regular payments, surely the terms of the agreement states minimum payment due, and you don't want to be seen paying one creditor and not another, that's preferential treatment, which is a no no

any debt plan advice would have expected a regular payment due( even if you can't afford to,, but simply the terms and conditions of that card in your SAO, even if somehow or another the creditor has said no payments for a month or two

you have some choices , either up your expenses a little more and qualify for a DRO , you are only allowed £75 month excess.

or you lower expenses and do a lengthy debt management plan., don't advise, cus in reality you need a reasonable standard of living, not a pauper on a long dmp

then contact a debt charity like money wellness, stepchange , citizens advice bureau or the one I like christians against poverty who are excellent

and present them with a SAO, like this, but you can still up your expenses before you do present them with your income, overheads, cos at moment ,they are still too low in areas, they then give you their own forms like that you fill in.

they will contact creditors , stop interest if they have a solution that works, but if you keep your available amount to contribute at £152, they will say a debt plan will take 15 years to repay and that's too long, usual it's 6 years or under. and they will suggest another solution

I'm am still going towards a DRO, not an IVA cos you have no assets to protect , and as long as your landlord has no restrictions on insolvency when renting.

but you may not be allowed an emergency fund or gym membership in a dro, cos you will have up to £75 excess anyway a month to keep and do with you want.

you can give more room to up your haircuts , entertainment and shopping cos it's still low for a family of 3. but don't have a completely negative budget even if you can give your creditors nothing, and have done your priority bills and variable expenses,cos thar plan will be unworkable and not approved

step change , nation debt line dont do DROs but the other organisations i listed do

I know if you offer £152 a month, some of debt charities may wrongly suggest a 5 yr IVA, which you want to avoid, as i explained in my previous post.

a dro would suit you far better, 12 months debt free, it's just getting your budget to show you have £75 or under a month excess and it will stay that way for 12 months and it costs nothing for a DRO, no huge IVA £4000 fees, it's completely free to do.Christians Against Poverty solved my debt problem, when all other debt charities failed. Give them a call !! ( You don't have to be a Christian ! )

https://capuk.org/contact-us0 -

sorry that missing payment was an over sight0

-

[font=courier new][b]Statement of Affairs and Personal Balance Sheet[/b][b]Household Information[/b]Number of adults in household........... 1Number of children in household......... 2Number of cars owned.................... 0[b]Monthly Income Details[/b]Monthly income after tax................ 1150Partners monthly income after tax....... 0Benefits................................ 850Other income............................ 262[b]Total monthly income.................... 2262[/b][b]Monthly Expense Details[/b]Mortgage................................ 0Secured/HP loan repayments.............. 0Rent.................................... 797Management charge (leasehold property).. 0Council tax............................. 237Electricity............................. 167Gas..................................... 0Oil..................................... 0Water rates............................. 35Telephone (land line)................... 0Mobile phone............................ 31TV Licence.............................. 15Satellite/Cable TV...................... 0Internet Services....................... 78Groceries etc. ......................... 360Clothing................................ 60Petrol/diesel........................... 0Road tax................................ 0Car Insurance........................... 0Car maintenance (including MOT)......... 0Car parking............................. 0Other travel............................ 40Childcare/nursery....................... 0Other child related expenses............ 30Medical (prescriptions, dentist etc).... 10Pet insurance/vet bills................. 10Buildings insurance..................... 0Contents insurance...................... 12Life assurance ......................... 10Other insurance......................... 0Presents (birthday, christmas etc)...... 15Haircuts................................ 10Entertainment........................... 50Holiday................................. 60Emergency fund.......................... 30(Unnamed monthly expense)............... 0gym..................................... 28appliance cover......................... 25[b]Total monthly expenses.................. 2110[/b][b]Assets[/b]Cash.................................... 0House value (Gross)..................... 0Shares and bonds........................ 0Car(s).................................. 0Other assets............................ 0[b]Total Assets............................ 0[/b][b]No Secured nor Hire Purchase Debts[/b][b]Unsecured Debts[/b]Description....................Debt......Monthly...APRcredit card....................10000.....162.......17credit card....................5885......130.......20credit card....................6549......73........25Loan ..........................611.......18........29[b]Total unsecured debts..........23045.....383.......- [/b][b]Monthly Budget Summary[/b]Total monthly income.................... 2,262Expenses (including HP & secured debts). 2,110Available for debt repayments........... 152Monthly UNsecured debt repayments....... 383[b]Amount short for making debt repayments. -231[/b][b]Personal Balance Sheet Summary[/b]Total assets (things you own)........... 0Total HP & Secured debt................. -0Total Unsecured debt.................... -23,045[b]Net Assets.............................. -23,045[/b][i]Created using the SOA calculator at www.stoozing.com.Reproduced on Moneysavingexpert with permission, using other browser.[/i][/font]1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards