We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Pension investment risk category dilemma

Comments

-

Appreciate the advice and link Marcon. I just wish i’d been more interested in all this ten years ago. Better late than never I suppose.Marcon said:

Looking at your responses, finding out the facts and options for your scheme would be a pretty good starting point.Loyalandtrue77 said:Any advice would be much appreciated, thanks.

Then some basic reading such as https://www.moneyhelper.org.uk/en/pensions-and-retirement/building-your-retirement-pot/pension-investment-options-an-overview should give you more confidence about taking decisions.0 -

Albermarle said:

Normally when you first join a workplace pension, you will be asked what investments in the pension you want your money to be held in. If you do not make any choice ( and I think that covers nearly 99% of people) your money goes into a default fund.Loyalandtrue77 said:

I wasn’t familiar with the term ‘lifestyling’ but have had a look around and have read the pros and cons. I’m not sure exactly, but can only recall being asked whether i’d like to stay in a medium risk investment or not. It’s something I need to look into asap and see what the options are.Marcon said:

Must you use a lifestyling option, which is what you're describing in your post? Are there alternatives?Loyalandtrue77 said:In the last year or so i’ve finally decided to set a goal of quitting my main career job at what will become the new private pension age of 57, and taking my pension. I’d continue to work, doing something more flexible. Freelance work maybe. It’s a good few years away yet (ten) and you never know what’s around the corner, but I think it makes sense to at least have a plan.The dilemma I currently have is whether or not to inform my workplace pension of my intention or not. I can do this very easily online but i’m aware of the fact that this will likely trigger a change in the investment risk category, since i’d be within ten years of taking my pension. Higher risk, as it is now, could ‘potentially’ scupper my plans but low risk would slow growth at a time when I want to increase my pot as much as possible. A difficult four or five years in our industry back in 2015 coupled with a lack of focus on my pension has left me making up for lost time.Any advice would be much appreciated, thanks.

This is typically medium risk, meaning it will be about 60% equities ( shares) and the rest mainly bonds/gilts.

However many pensions default is a so called Lifestyle fund. This means it starts off with a higher risk/higher growth strategy when you are younger ( say 75% equities), and then as you approach retirement age, it derisks by reducing the % of equities.

If you do not tell the pension provider anything different they will have 65 in their system as your retirement date. You can change this online easily normally.

Of course you can retire when you like and you can start to take from the pension from 55/57, but this lifestyling option will work with the date in their system.

Also if you are looking to buy an annuity you need to check you are in an Annuity lifestyle fund, which will derisk completely, or in a Lifestyle drawdown, which will only derisk to a point.

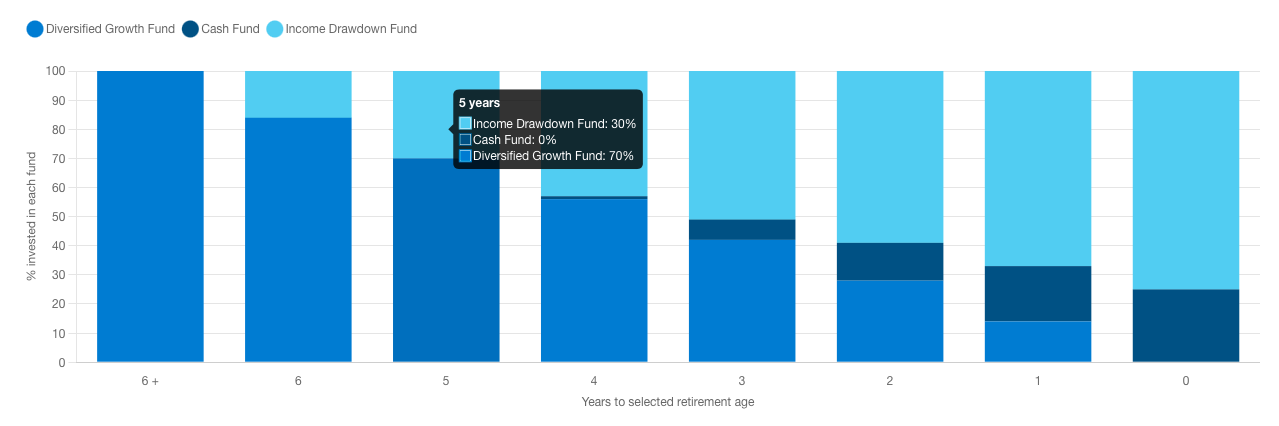

As an example, here's what one of my work pensions (administered by L&G) did on the default "Drawdown Lifestyle" pension profile. It was fully invested in the selected funds (the default was 100% in the Diversified Growth Fund) until 6 years before specified retirement date, then would gradually switched over to a mix of Income Drawdown Fund and Cash over the following 6 years.

This was the "Annuity Lifestyle" equivalent

It's pretty much the same thing, but invested in a different fund once into those final 6 years.1 -

Don't kick yourself too hard. Many people take an interest about a month before they decide to retire...!Loyalandtrue77 said:

Appreciate the advice and link Marcon. I just wish i’d been more interested in all this ten years ago. Better late than never I suppose.Marcon said:

Looking at your responses, finding out the facts and options for your scheme would be a pretty good starting point.Loyalandtrue77 said:Any advice would be much appreciated, thanks.

Then some basic reading such as https://www.moneyhelper.org.uk/en/pensions-and-retirement/building-your-retirement-pot/pension-investment-options-an-overview should give you more confidence about taking decisions.

Given the weird behaviour of the markets in recent years, there's no guarantee that 'taking an interest' would have done you any favours - but it would certainly be sensible to have a bit of a think now.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards