We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Understanding old deferred DB pension & GMP

Whiterose23

Posts: 269 Forumite

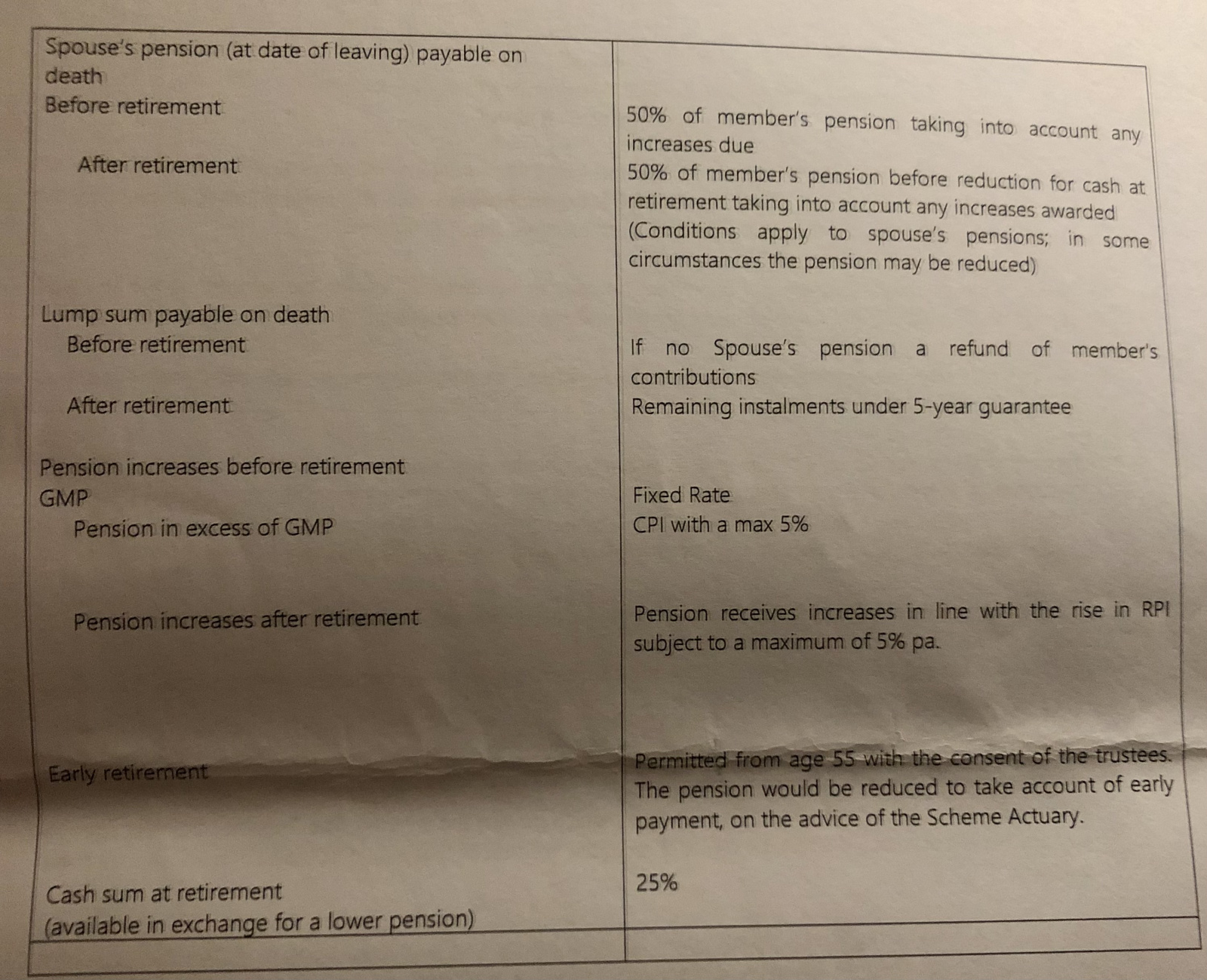

Please could any pension-savvy members read the attached statement and help me understand the GMP element and how it is likely to affect my pension and when etc? I’ve tried to understand how this is calculated by reading articles online but am struggling. This is a statement I received from the scheme in 2021 when I queried the transfer value.

Thank you.

0

Comments

-

When you were a member of this scheme, you were contracted out of the State Earnings Related Pension Scheme (SERPS).

You and your employer paid a lower rate of National Insurance.

This meant that you were not accruing state pension above the Basic State Pension but you were accruing a scheme pension

that was at least as great as the pension you would have accrued had you been contracted in to SERPS.

This is your Guaranteed (by the scheme) Minimum Pension, due from 60 (F) 65 (M).

You joined the Scheme post 1988 and therefore your GMP was all accrued post 1988.

In 1997, the GMP system came to an end in favour of what was known as the Scheme Reference Test.

Under the SRT, members had to receive a pension at least broadly equivalent to 1/80th of band earnings with a spouse's pension

of 50% on death.

You left the Scheme in 2000, becoming a deferred pensioner.

Your GMP and excess revalue differently in deferment.

The GMP is revaluing at Fixed Rate - in your case at 6.25%.

The excess over GMP is revaluing at CPI capped at 5%.

According to the statement, pensions in payment increase at RPI capped at 5%.

HOWEVER, in your place I would be inclined to ask the Administrator if in fact the revalued post 88 GMP will increase at a

maximum 3% after GMP age and if any increase will be paid on the pre 97 excess.

https://techzone.abrdn.com/anon/public/pensions/Tech-guide-guaranteed-min-pen

1 -

OP - before going any further, you might check with your scheme how they are going to equalise GMPs. They are inherently different for men and women and thus 'discriminatory'. All schemes are having to go through an incredibly elaborate, lengthy and expensive exercise to remedy this. You don't want the full gory detail of what the scheme is having to do - just what it means for members, so that's the question you need to ask.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1

-

I joined the scheme in 1991 and left in 2000, and am female. Am I right in thinking the GMP part is will be paid separately from age 60? If I’m to be paid anything at all?Another letter I have from 2019 states the GMP included was £36,336, pre-1997 benefits were £34,382, and post 1997 were £22,731.0

-

you might check with your scheme how they are going to equalise GMPs

There are some notes on GMPE in the link referenced in my previous.

1 -

No; your pension will be paid as 'one pension'.Whiterose23 said:I joined the scheme in 1991 and left in 2000, and am female. Am I right in thinking the GMP part is will be paid separately from age 60? If I’m to be paid anything at all?Another letter I have from 2019 states the GMP included was £36,336, pre-1997 benefits were £34,382, and post 1997 were £22,731.

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0 -

How old will you be at NRD?

Have you yet obtained a state pension forecast?

https://www.gov.uk/check-state-pension

0 -

NRD is 65 and my state pension is at maximum.xylophone said:How old will you be at NRD?

Have you yet obtained a state pension forecast?

https://www.gov.uk/check-state-pension1 -

NRD is 65

https://techzone.abrdn.com/anon/public/pensions/Tech-guide-guaranteed-min-pen

Deferring beyond 60/65

If the member retires more than seven weeks later than their 60th birthday (women) / 65th birthday (men), their accrued GMP must be increased by at least 1/7% for each complete week thereafter.

1 -

Am I correct to assume the forecasts I receive do not take into account the GMP recalculation and that will only happen when I opt to start drawing down the pension or when I turn 60?

Or does the fact that my statement includes a figure for the GMP element mean that the figures quoted are accurate now?

Sorry for all the questions.0 -

Why not do as I've suggested and ask for information from the scheme about GMP equalisation and how it impacts you (if at all)? An up to date statement could be requested at the same time.Whiterose23 said:Am I correct to assume the forecasts I receive do not take into account the GMP recalculation and that will only happen when I opt to start drawing down the pension or when I turn 60?

Or does the fact that my statement includes a figure for the GMP element mean that the figures quoted are accurate now?

Sorry for all the questions.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.1K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.7K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards