We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Civil Service Classic Pension - Exchanging 25% Tax Free for Added Pension

Julezy101

Posts: 87 Forumite

Hello,

Am I correct in thinking the 12:1 ratio applies if you want to exchange your max 25% tax free portion for extra annual pension?

e.g. if annual pension is 4k, 25% tax free is 12k, could you then exchange the 12k for an extra 1k to make it 5k?

If this is correct and say at age 67 (full SP) you would end up paying 20% tax on this extra 1k so £200 tax. Overall an extra £800 per annum. So you'd need to live 15+ years to start to get the benefit of this?

Thanks

Am I correct in thinking the 12:1 ratio applies if you want to exchange your max 25% tax free portion for extra annual pension?

e.g. if annual pension is 4k, 25% tax free is 12k, could you then exchange the 12k for an extra 1k to make it 5k?

If this is correct and say at age 67 (full SP) you would end up paying 20% tax on this extra 1k so £200 tax. Overall an extra £800 per annum. So you'd need to live 15+ years to start to get the benefit of this?

Thanks

0

Comments

-

No, the inverse commutation factors are age dependent on can be found on the MyCSP site.

They aren't particularly attractive imho. As an example a 67 year old giving up a £10k lump sum will get additional pension of £591 per annum.

Also you are confusing matters with reference to 25% tax free. The standard lump sum in Classic is 3 x pension but you can commute more.1 -

@Phoenix72 and @xylophonexylophone said:

Thanks for that,

So £4.58 for every £100 at age 60

So for £12k that's only £550 extra per annum which is a lot less than I thought and as you say not particularly attractive.0 -

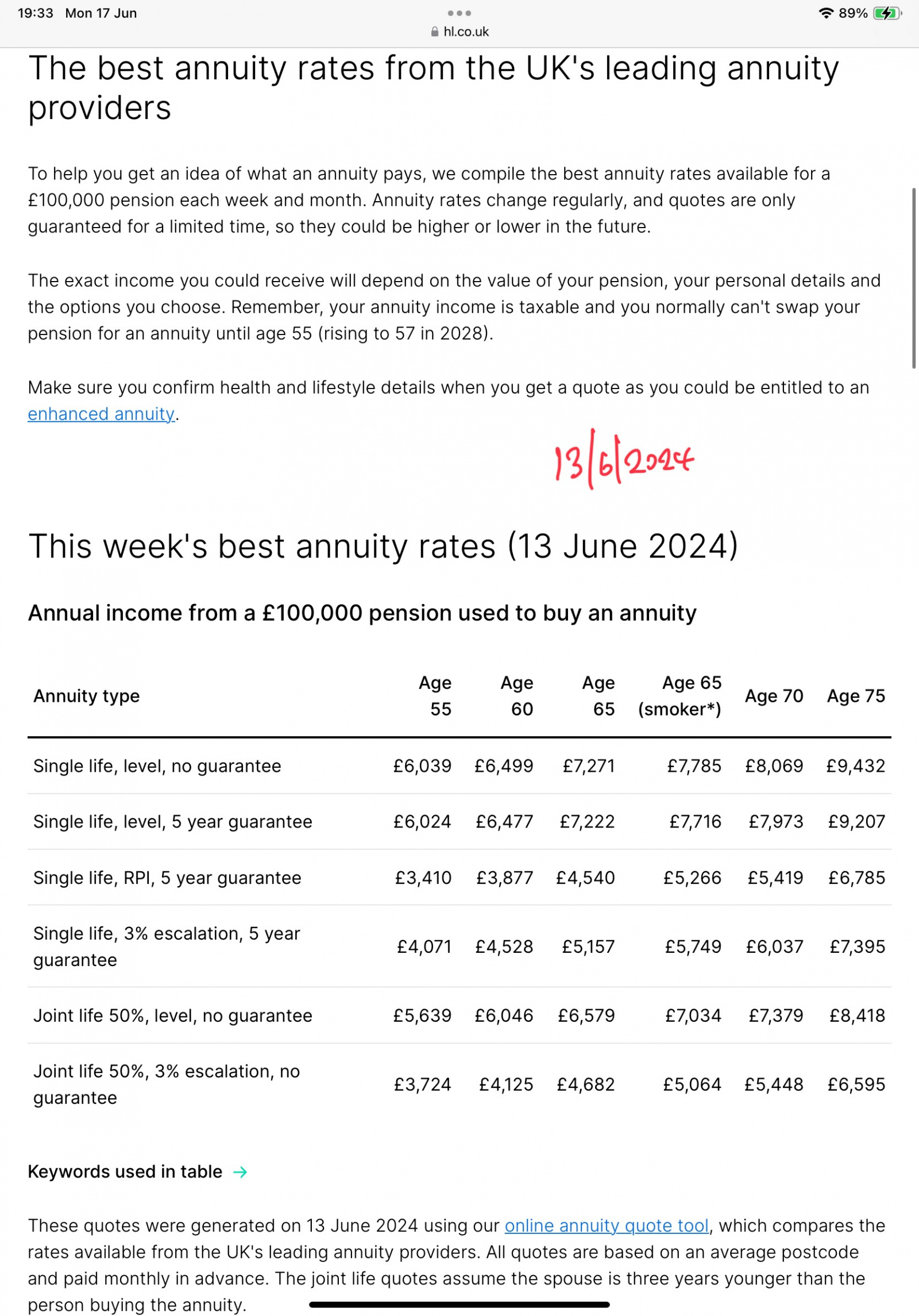

Even with higher annuity rates currently available in the insurance market, these rates you have here beat those quite nicely.Julezy101 said:

@Phoenix72 and @xylophonexylophone said:

Thanks for that,

So £4.58 for every £100 at age 60

So for £12k that's only £550 extra per annum which is a lot less than I thought and as you say not particularly attractive.

e.g. single life with rpi is currently £3.87 per annum per £100 at age 65.

0 -

Remember that with inverse commutation you are exchanging tax-free money for taxable income. Whereas with annuity purchase you usually take the 25% tax free lump sum and use the 75% remaining (taxable) to purchase an annuity. That is a big difference even for a basic rate taxpayer - adjust for this and the rates are very similar.

RPI is also about 1 percentage point higher than CPI.

So it is not a like-for-like comparison.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards