We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

TSB refusing to change default date - Scottish Trust Deed

I have been in a protected Trust Deed since January 2023 and TSB are refusing to change the default date of my Credit Card to be aligned to the PTD. I have raised a complaint with them that they have not upheld and the FOS won't help either as they are saying the issue is over 6 months ago so won't help.

I was under the impression that the default date should be aligned with when the PTD was granted?

Any help will be greatly appreciated

Comments

-

Not necessarily, if it pre-dates the trust deed, that is OK.

How far out of line are we talking here, months/years?

A few months either way won`t hurt.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

The default date for the Mastercard is showing as August 2023 while the PTD was signed in January 2023. TSB are refusing to change.Currently in a Protected Trust Deed - 17 payments until DEBT FREE - February 20270

-

Unsure if Scottish law differs from rest of UK, but that is clearly wrong.

If FOS won`t do anything, then your stuck with it, you could raise the matter with the ICO, they deal with anything data related, if you do decide to complain to them, make sure you say you only just noticed the discrepancy, as the 6 month rule may apply to them as well.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

Just wanted to resurrect this with another quick query.

With default dates on a Trust Deed/IVA - should they in theory be aligned with the date the deed was signed or when it became protected?

Currently in a Protected Trust Deed - 17 payments until DEBT FREE - February 20270 -

I am not a Scottish adviser and I am not sure if there is one that posts here regularly.

FWIW, my guess is that the default date should be when the creditor accepted the TD, and the date it became protected for creditors that did not accept the TD.0 -

Hello ryanb92… I'm a bit late to the party with this one, but I have just had my Trust Deed drop off my credit file on the 25th March 2026. The Trust Deed was protected two months after this and some companies tried to align the default date to that, but that is incorrect. It is the date your Trust Deed started.

The TSB comment caught my eye when browsing online for something, as I've just discovered issues with a past Halifax and MBNA credit card and this post came up when I was looking for evidence online.

The issue you face is the exact one I faced, but it took multiple complaints and up to 18 months with one of the complaints to get it updated. They admitted in their letter that they have INTERNAL POLICIES that override the industry guidance!

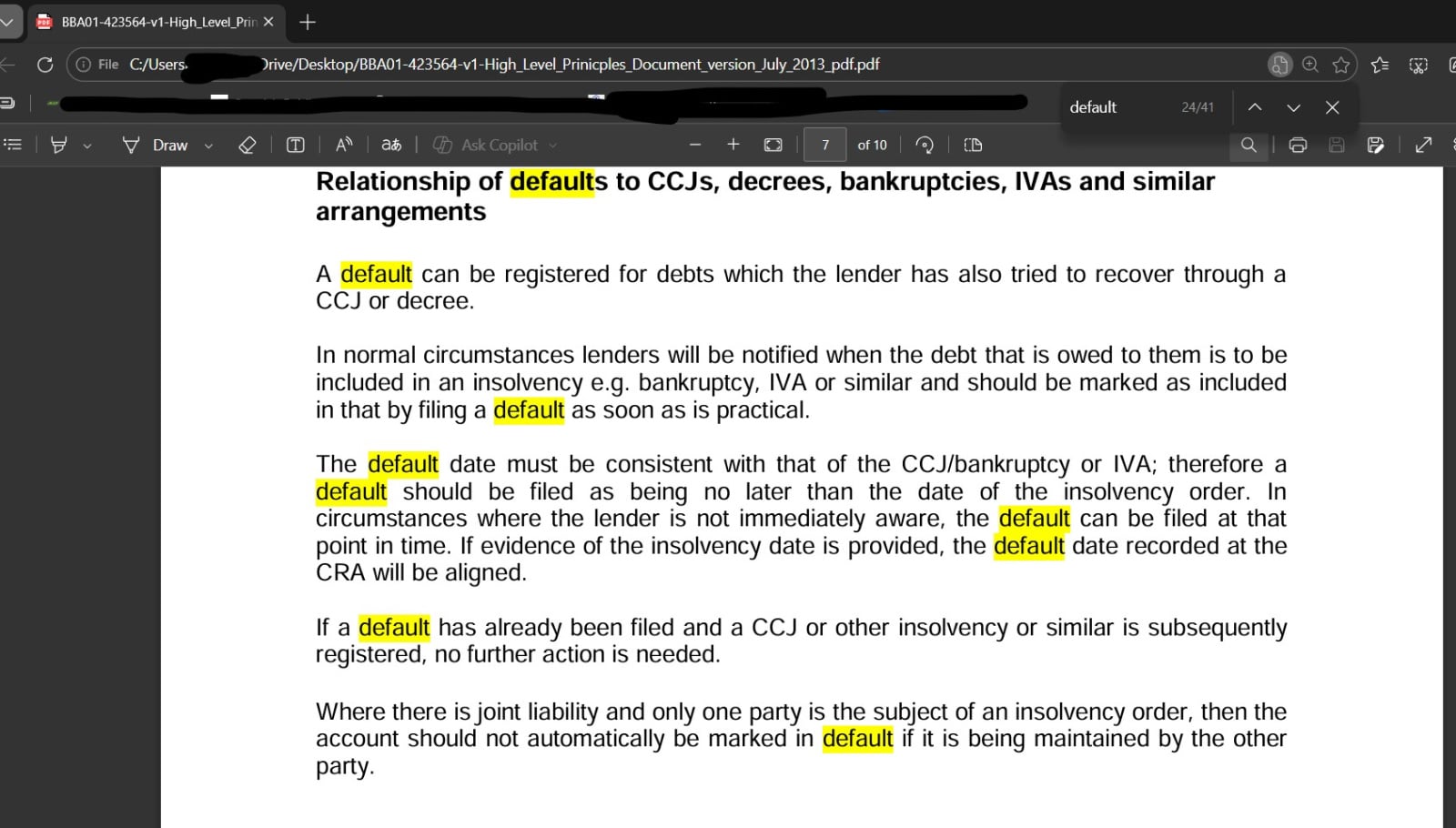

The guidance from the Information Commissioner’s Office (ICO) clearly states from page seven of their High Level Prinicples Document:

Relationship of defaults to CCJs, decrees, bankruptcies, IVAs and similar arrangements

The default date must be consistent with that of the CCJ/bankruptcy or IVA; therefore a default should be filed as being no later than the date of the insolvency order. In circumstances where the lender is not immediately aware, the default can be filed at that point in time. If evidence of the insolvency date is provided, the default date recorded at the CRA will be aligned.

If a default has already been filed and a CCJ or other insolvency or similar is subsequently registered, no further action is needed.

I can't upload the full document, as it won't let me upload a PDF, but I've got a screenshot below for you. If you haven’t already, put in another complaint and also put one in with the ICO and contact them for a copy of the document. Some of the information is available online, but don’t let them or any other company away with it.

The Trust Deed affects you for six years and it is a long time and an awful process to go through, so despite what others say, a few months here and there don’t matter, as it does… Best of luck, but don’t let them away with it. Their letter to me clearly stated they were reviewing these policies, but from your post, it is clear they haven’t…

0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards