We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Commute 25% tax free lump sum - Deferred Pension

goldengoldensky

Posts: 10 Forumite

Hello,

I'm new to the forum and I have a question regarding a deferred pension. I should start by saying that I have little knowledge on this topic so any advice/comments from more experienced users would be greatly appreciated. I apologise in advance for the long post! Not sure what information is necessary to provide so I thought more is better than less to provide context.

In the early nineties I was a member of a defined benefit pension plan for a large manufacturing company. I worked there and contributed for approximately 3 years. I never transferred the plan so it has been investing for around 30 years. I am currently 51 and will turn 55 in March 2028.

Last year (June 2023) I contacted the company's pension department to ask for more information on my benefits, specifically regarding early retirement (at 55). They told me that I can claim my pension benefits for retirement from my 55th birthday and that an early retirement factor will be applied (I think it is 0.69 factor for 10 years early) and the following options;

• Full annual pension payable on a monthly basis, or

• Commute 25% for a tax free lump sum and the reduced annual pension payable on a monthly basis.

They also included a letter which states the scale pension per annum as of the date I left the plan, as well as the amount of the deferred pension per annum (revalued as of last June).

My question is regarding the 25% tax-free lump sum. Is there:

a) a way I can find out what the 25% amount is to date (as of now, just to get an idea)? or

b) a way to estimate what the 25% tax-free lump sum might be when I turn 55 by using the per annum figures from the 2023 letter and an estimated inflation rate for the remaining years?

Thanks in advance for any advice/comments.

I'm new to the forum and I have a question regarding a deferred pension. I should start by saying that I have little knowledge on this topic so any advice/comments from more experienced users would be greatly appreciated. I apologise in advance for the long post! Not sure what information is necessary to provide so I thought more is better than less to provide context.

In the early nineties I was a member of a defined benefit pension plan for a large manufacturing company. I worked there and contributed for approximately 3 years. I never transferred the plan so it has been investing for around 30 years. I am currently 51 and will turn 55 in March 2028.

Last year (June 2023) I contacted the company's pension department to ask for more information on my benefits, specifically regarding early retirement (at 55). They told me that I can claim my pension benefits for retirement from my 55th birthday and that an early retirement factor will be applied (I think it is 0.69 factor for 10 years early) and the following options;

• Full annual pension payable on a monthly basis, or

• Commute 25% for a tax free lump sum and the reduced annual pension payable on a monthly basis.

They also included a letter which states the scale pension per annum as of the date I left the plan, as well as the amount of the deferred pension per annum (revalued as of last June).

My question is regarding the 25% tax-free lump sum. Is there:

a) a way I can find out what the 25% amount is to date (as of now, just to get an idea)? or

b) a way to estimate what the 25% tax-free lump sum might be when I turn 55 by using the per annum figures from the 2023 letter and an estimated inflation rate for the remaining years?

Thanks in advance for any advice/comments.

0

Comments

-

If the pension was deferred before 6/4/97 you will have a Guaranteed Minimum Pension.

It is possible that this revalues at fixed rate.

Do you have the Scheme Pension Guide and a statement of deferred benefits at date of leaving showing GMP and excess?

The statutory position is here

https://www.barnett-waddingham.co.uk/comment-insight/blog/revaluation-for-early-leavers/

but your scheme may be more generous.

With regard to PCLS see (under Defined Benefit Schemes)

https://techzone.abrdn.com/public/pensions/Tech-guide-tax-free-cash

And check out the situation with regard to earliest age at which you may take benefits.

See

https://www.thisismoney.co.uk/money/pensions/article-13370461/Can-private-pension-55-bizarre-birth-year-quirk-STEVE-WEBB-replies.html

And also check the position with increases in payment on pre 97 accrual.

See https://forums.moneysavingexpert.com/discussion/comment/80688308/#Comment_80688308

Have you obtained a state pension forecast?

https://www.gov.uk/check-state-pension

2 -

Before I took my DB I was given a list of options with guaranteed periods and with or without lump sums but each option had the numbers that would be paid.

I assume your DB administrators would have given you the amounts in 2023. I would suggest that given the security of the vast majority of DB pensions the numbers will have gone up. But with 3 years service it's possibly not a lot. They won't have changed significantly but you should ask for them again before making your decision.

DB pensions are not like DC ones that have a fund value. DB by their very definition aren't dependent on stock markets in the same way that will increase or decrease the value of your pension. Some DB schemes might give you a fund value but this is a useless figure unless you can transfer the money to another DB scheme or if you are going through a divorce and need to consider pension sharing.I’m a Forum Ambassador and I support the Forum Team on Debt Free Wannabe, Old Style Money Saving and Pensions boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.

Click on this link for a Statement of Accounts that can be posted on the DebtFree Wannabe board: https://lemonfool.co.uk/financecalculators/soa.php

Check your state pension on: Check your State Pension forecast - GOV.UK

"Never retract, never explain, never apologise; get things done and let them howl.” Nellie McClung

⭐️🏅😇🏅🏅🏅🏅🏅1 -

Realistically the only way to get a ball park figure is from the scheme's administrators - who may not be willing to provide this (not their decision; that will be an instruction from the trustees).goldengoldensky said:Hello,

I'm new to the forum and I have a question regarding a deferred pension. I should start by saying that I have little knowledge on this topic so any advice/comments from more experienced users would be greatly appreciated. I apologise in advance for the long post! Not sure what information is necessary to provide so I thought more is better than less to provide context.

In the early nineties I was a member of a defined benefit pension plan for a large manufacturing company. I worked there and contributed for approximately 3 years. I never transferred the plan so it has been investing for around 30 years. I am currently 51 and will turn 55 in March 2028.

Last year (June 2023) I contacted the company's pension department to ask for more information on my benefits, specifically regarding early retirement (at 55). They told me that I can claim my pension benefits for retirement from my 55th birthday and that an early retirement factor will be applied (I think it is 0.69 factor for 10 years early) and the following options;

• Full annual pension payable on a monthly basis, or

• Commute 25% for a tax free lump sum and the reduced annual pension payable on a monthly basis.

They also included a letter which states the scale pension per annum as of the date I left the plan, as well as the amount of the deferred pension per annum (revalued as of last June).

My question is regarding the 25% tax-free lump sum. Is there:

a) a way I can find out what the 25% amount is to date (as of now, just to get an idea)? or

b) a way to estimate what the 25% tax-free lump sum might be when I turn 55 by using the per annum figures from the 2023 letter and an estimated inflation rate for the remaining years?

Thanks in advance for any advice/comments.

If you're taking your benefits 10 years early, and only had 3 years of scheme membership, it isn't going to be a huge amount - a comment made to temper your expectations, not depress you!

Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!1 -

A lot depends on how much your salary was when you left the company. If for example it was £30K, then taking into account inflation and some other guesswork, the 25% tax free could be in the region of say £12K, give or take a few grand.1

-

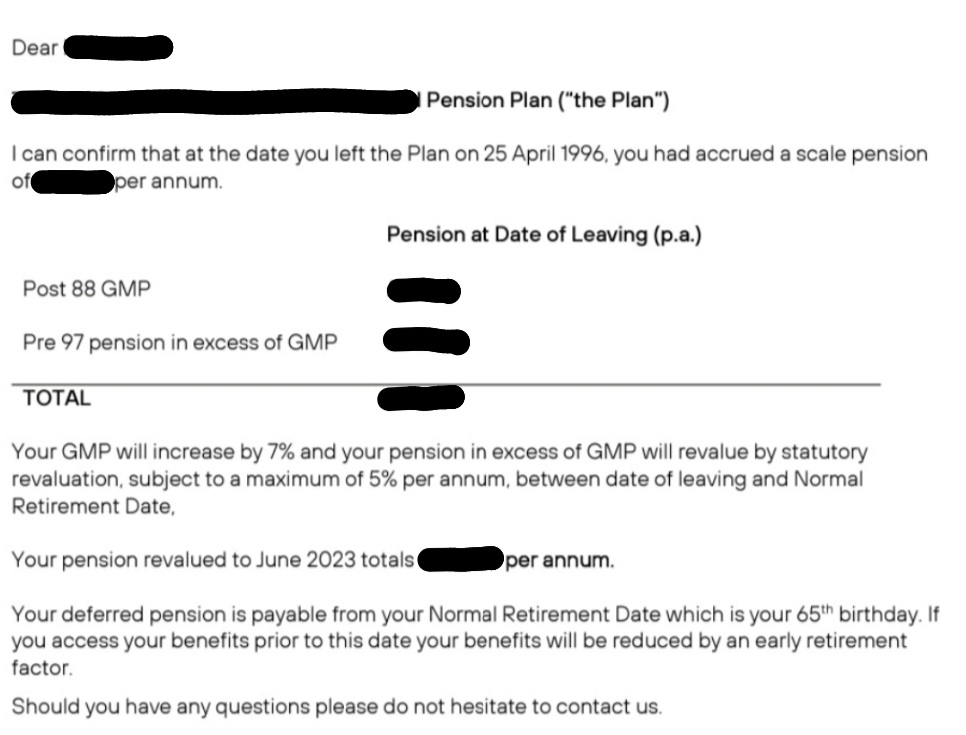

Thanks all for your responses/comments (and links, which I have looked at).

The only thing I have been provided with is the June 2023 letter below (I have removed personal information). In the same email, they told me that I can claim my pension benefits for retirement from my 55th birthday (an early retirement factor will be applied) and that I will be offered the following options;

• Full annual pension payable on a monthly basis, or

• Commute 25% for a tax free lump sum and the reduced annual pension payable on a monthly basis.

The letter only provides details of the per annum amount. I assume there must be a total sum from which they calculate the per annum figure. Is it common to also be given details of the "total" amount to date? If so, is this something I can calculate myself (using the per annum figure from the letter) or do I need to request this information from my provider?

Thanks once again for your time (and patience).

0 -

Being able to take your pension 10 years early, subject to an early payment reduction, and being able to commute (give up) some of your pension for additional tax free cash are all very standard.

BUT. Before you get too excited and mentally spend your cash, your actual options may not be standard. You have just 3 years pensionable service, which includes a GMP. Your GMP has been increasing in deferment at a higher rate than your non GMP 'excess' pension. Briefly, when you opt to take your pension, it can't be reduced below the GMP rate. It is possible that your actuarily reduced pension at 55 will meet the GMP test, but unlikely that you would be able to further reduce your pension by commutation.2 -

Thanks Silvertabby for your response.

It sounds like I'll have to wait until nearer the time to find out more details/my options.

Question for "Brie".

You mentioned that "Before I took my DB I was given a list of options with guaranteed periods and with or without lump sums but each option had the numbers that would be paid."

How long before did you reach out to the administrators to request this information?

Thanks1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards