We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Early Pension and National Insurance Contributions

Comments

-

Hi therexylophone said:First check your forecast

https://www.gov.uk/check-state-pension

What exactly does it say at estimate to 5/4/23?

Will the tax year just ending be a qualifying year?

How many QY did you have at 5/4/16?

And from 6/4/16 to the tax year just ending?

Many thanks for your reply.

Sorry for being an idiot but could you clarify what ...

'How many QY did you have at 5/4/16?

And from 6/4/16 to the tax year just ending?'

means? Are these dates?0 -

Yes they are dates. There is an important distinction between years earned up to 5 April 2016 and after.The following 6 anonymous details tell everything about your pension and what you need to do, it is just fairly straightforward maths.Current weekly £££.pp amount accrued up to April 2023

Number of pre April 2016 NI years full

Number of post April 2016 NI years full

Tax year you reach state retirement

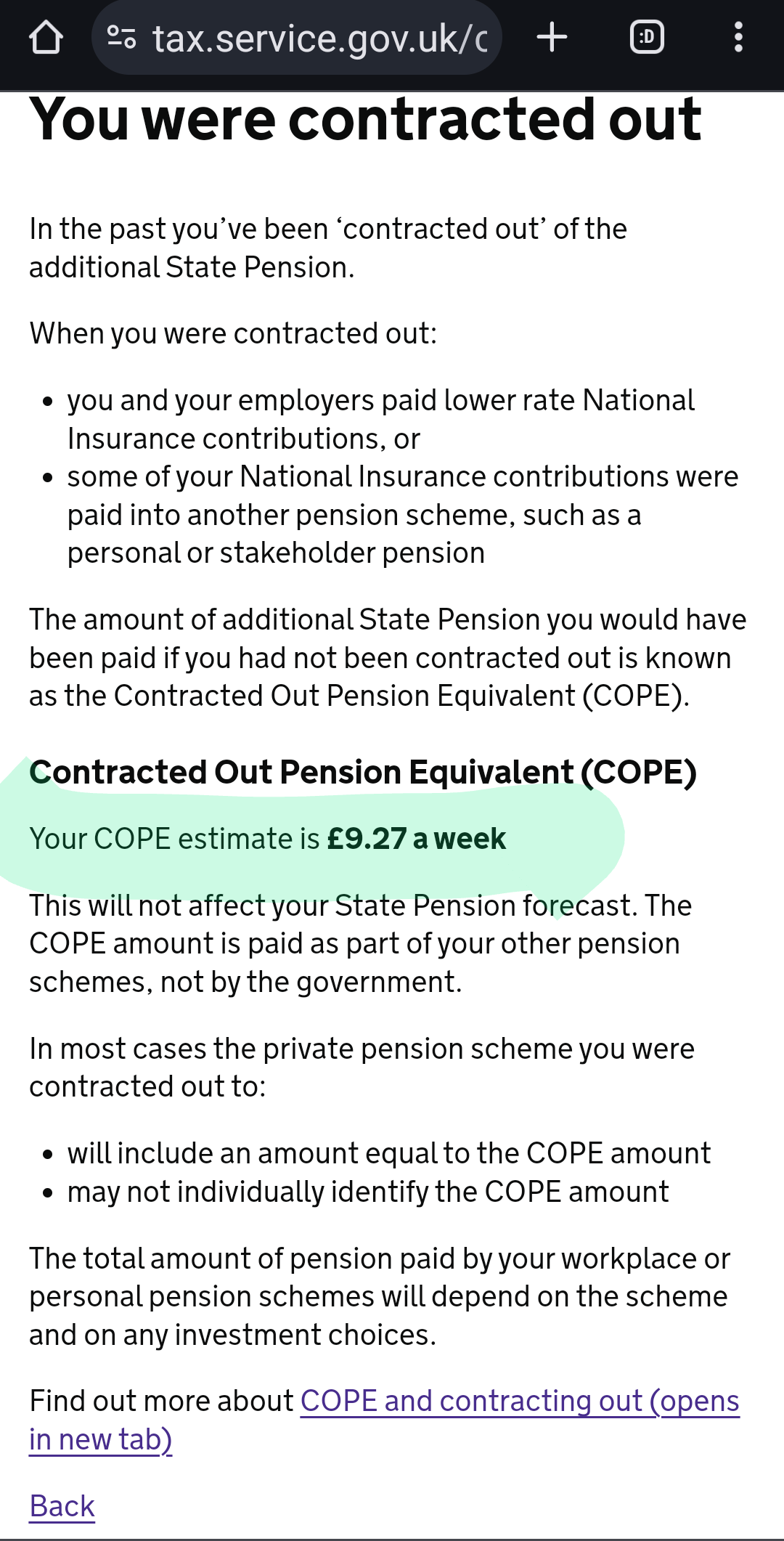

Any COPE amount shown, in a click link in "You've been in a contracted-out pension scheme", if there is one.

Years which show not full and prices

1 -

"You've been in a contracted-out pension scheme", if there is one.

If you were a member of TPS pre 6th April 2016 then you were in a Contracted Out (of Additional State Pension) Scheme and therefore there should definitely be a COPE ( rebate derived amount) shown.

0 -

Goodness me I didn't realise how thick I was! "Straightforward maths?' I'm afraid I understand very little from your message. What on earth do I do with those figures once I get them?molerat said:Yes they are dates. There is an important distinction between years earned up to 5 April 2016 and after.The following 6 anonymous details tell everything about your pension and what you need to do, it is just fairly straightforward maths.Current weekly £££.pp amount accrued up to April 2023

Number of pre April 2016 NI years full

Number of post April 2016 NI years full

Tax year you reach state retirement

Any COPE amount shown, in a click link in "You've been in a contracted-out pension scheme", if there is one.

Years which show not full and pricesI see no click link for "You've been in a contracted-out pension scheme" Or any mention of COPE. I assume you mean on the gov web page but even so I fail to understand the rest of it.I just phoned them up from the Gov website to be told. 'You will get the maximum pension because you have paid the full amount'

and what if I didn't pay any more NI contributions for the next 7 years?

'you have paid the full amount'

but I have a missing year in 2017 when I was ill?

'you have paid the full amount'.

So I don't/won't need to top up over the next 7 years? 'No, because you have paid the full amount'0 -

Looking at your figures for the next 5 years, do you have an emergency fund or savings. If not it looks rather tight.0

-

Goodness me I didn't realise how thick I was! "Straightforward maths?' I'm afraid I understand very little from your message. What on earth do I do with those figures once I get them?

The idea was that you post them up here and someone would decipher it all for you.

I just phoned them up from the Gov website to be told. 'You will get the maximum pension because you have paid the full amount'The pension forecast would tell you that, if you already had the maximum then it would tell you that you cannot improve the forecast.

0 -

What figures and how will it be tight? Very confused.[Deleted User] said:Looking at your figures for the next 5 years, do you have an emergency fund or savings. If not it looks rather tight.

0 -

I see no click link for "You've been in a contracted-out pension scheme" Or any mention of COPE.

Are you sure that you have obtained your forecast here?

https://www.gov.uk/check-state-pension

Were you a member of the Teachers' Pension Scheme (TPS) or any other contracted out pension scheme before 6th April 2016?

If so, there should definitely be a COPE and if there isn't (ie if your contracted out years have for some reason not been factored in to your record (which seems extraordinarily unlikely), then you cannot rely on what you have been told about your state pension.

On 6/4/16 (date), two calculations were done for all under State Pension Age to establish the 'starting amount" for New State Pension.

The starting amount was the HIGHER of

Old Rules

NI full years (aka qualifying years) (max 30) /30 x Full Basic State Pension + (Additional State Pension - (if applicable) Deduction for Contracting Out)

New Rules

{NIFY (max 35)/35 x Full New State Pension} - (if applicable) Contracted Out Pension Equivalent. (COPE).

Each person was in one of three positions

(a) starting amount equal to full NSP

(b) starting amount more than full NSP

(c) starting amount less than full NSP.

If in position (a) or (b), then while if under SPA, employed and earning the relevant amount the person would still have to pay NI up to SPA, it would not improve his starting amount. This would just revalue up to and beyond SPA under the rules for indexing state pensions.

If in position (c), then it would be possible to improve the "starting amount" up to (but not in excess of) a full New State Pension

by NI contributions or credits.

It is quite possible that you have reached full NSP through contributions from 6/4/16 onwards - if you supplied the information

requested and the COPE someone could check.

0 -

Sorry I wasn't clear. I am not talking about state pension stuff. You said on another thread the plan was to have £1500 a month for 5 years. This would be made up from £8000 a year from TP, the £25000 lump sum and the £25000 in pension pots. Obviously I am not allowing for pension pot growth or annual pension increase. I calculated 1500 a month for 5 years is 90000, which is exactly what your resources would equal. (5 x 8000 +25000 +25000) That is what I meant by tight if you have no other savings. I am not saying impossible but little room for error.jimmyjazz1992 said:

What figures and how will it be tight? Very confused.[Deleted User] said:Looking at your figures for the next 5 years, do you have an emergency fund or savings. If not it looks rather tight.0 -

Hi Jimmy, sharing these items above plus your COPE amount would let xylophone and/or others here do the calculation needed to explain how your pension has been worked out.xylophone said:First check your forecast

https://www.gov.uk/check-state-pension

What exactly does it say at estimate to 5/4/23?

Will the tax year just ending be a qualifying year?

How many QY did you have at 5/4/16?

And from 6/4/16 to the tax year just ending?

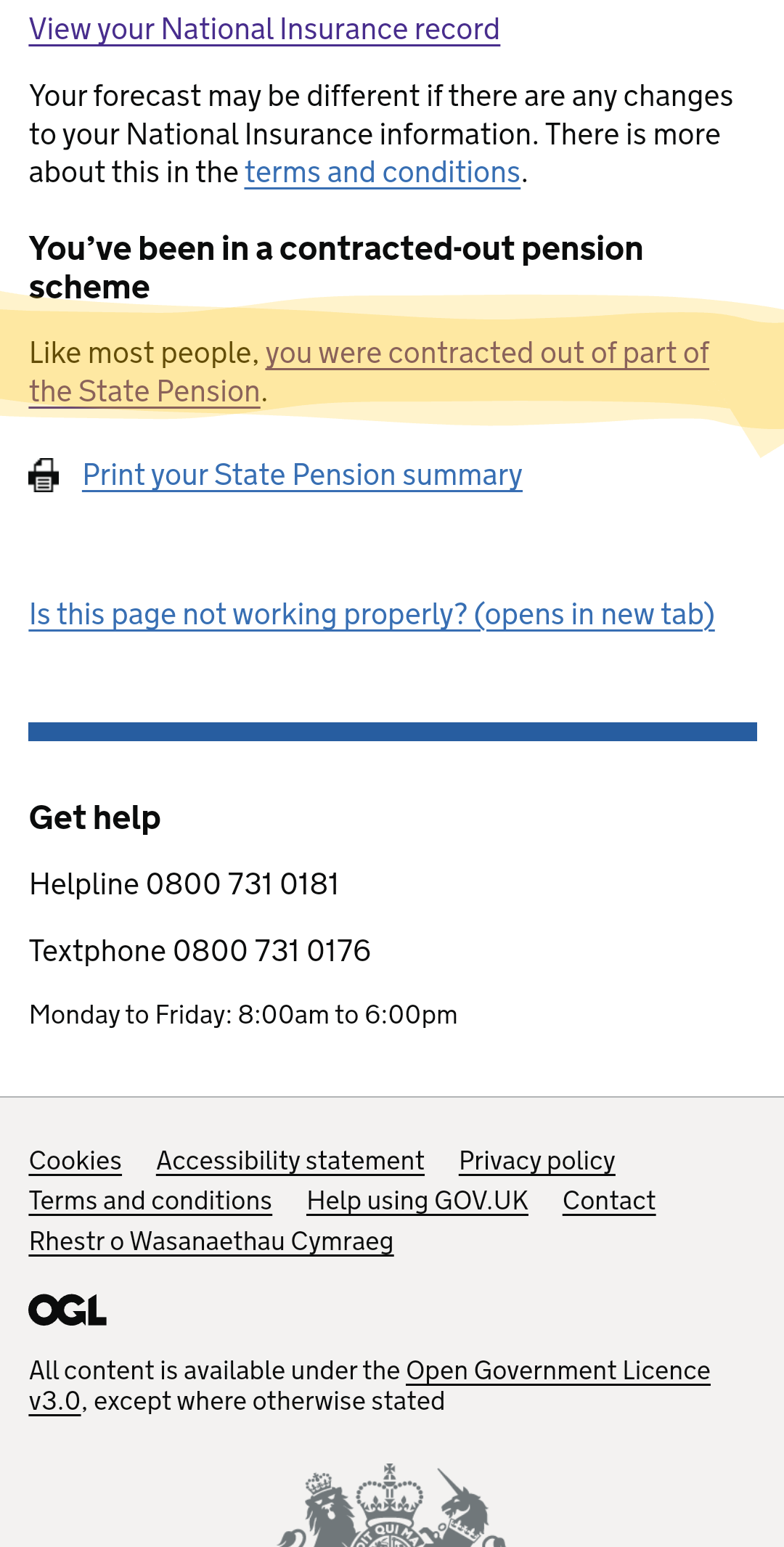

It is a bit alien if you're not used to it - I've put some screen shots below that might help, I've just obscured personal info where you would see your birthday when you reach state pension age, name etc.

Let us know what it says in the bit highlighted purple in my picture:

If you scroll down that same page, you will see a link to get your COPE amount - click on the link as shown in yellow in the pic below:

Clicking that link sends you to a new page which will give you your COPE amount - let us know what that is:

Then, go back to your forecast and click the link to view your national insurance history, on your history page count up the years that say they are full, from when you were a nipper, right up to and including 2015 to 16 - this is how many qualifying years you have prior to 6/4/2016, which xylophone asked for - let us know that figure.

Lastly, there are two more things that your pension forecast doesn't know yet but you can estimate, which might add a further two full years to what you already have:

- for the 2023-24 tax year, which is just about to end, are you likely to get a full NI year. If you are paid monthly then if your March payslip says your NI payment total for the year to date you could tell us that to see if it's likely to be enough.

- because you are planning to retire in September of the 2024-25 tax year, you will have had 5 or 6 months of pay in that year, so might have earned enough for that to also qualify as a full year - if you are happy to tell us an estimate of what you will earn in those 5/6 months in total we can make a guess.

Note: There is a really common misconception that everyone now needs 35 qualifying years to get the full state pension, but most people are in the transition period having worked both before and after 2016 when the new state pension came in, so everyone's calculation is different depending on their age and work history. I am a rare unicorn who actually does need 35 years on transitional rules - I have 20 now and need 15 more, but that is not the norm and you could need more or fewer years than 35. If you provide the info above someone can explain your personal calculation.

Apologies for the long post, I hope that helps a bit.6

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards