We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

USS Projected DB Pension mostly worse Since April 2024

Comments

-

Maybe those directly materially affected should send a formal complaint and then follow up with Pension Ombudsman?BikingBud said:

I feel a letter coming to USS asking for illustrations of the different scenarios, ERF and uplift payments before and after Apr 24 and also confirming when they knew they would be moving the ERF change implementation date to Oct 24.Simes122 said:Shambles indeed! Was planning on going end Apr. New factors announced making that a poor decision. So damaged limited it by going end March, forgoing a months salary, and the one off uplift payment, and the one off uplift x3 on my lumpsum. Not to mention a lot of stress! This protected my position but was materially worse than it would have been had I waited till end Apr. If they’ve pushed back the date now, I am materially disadvantaged by several k. Do I have the right to some kind of redress here? Loss of earnings, loss of lump sum catch up payment etc?

They certainly didn't tell me about it on my illustration and subsequent discussion in mid March.1 -

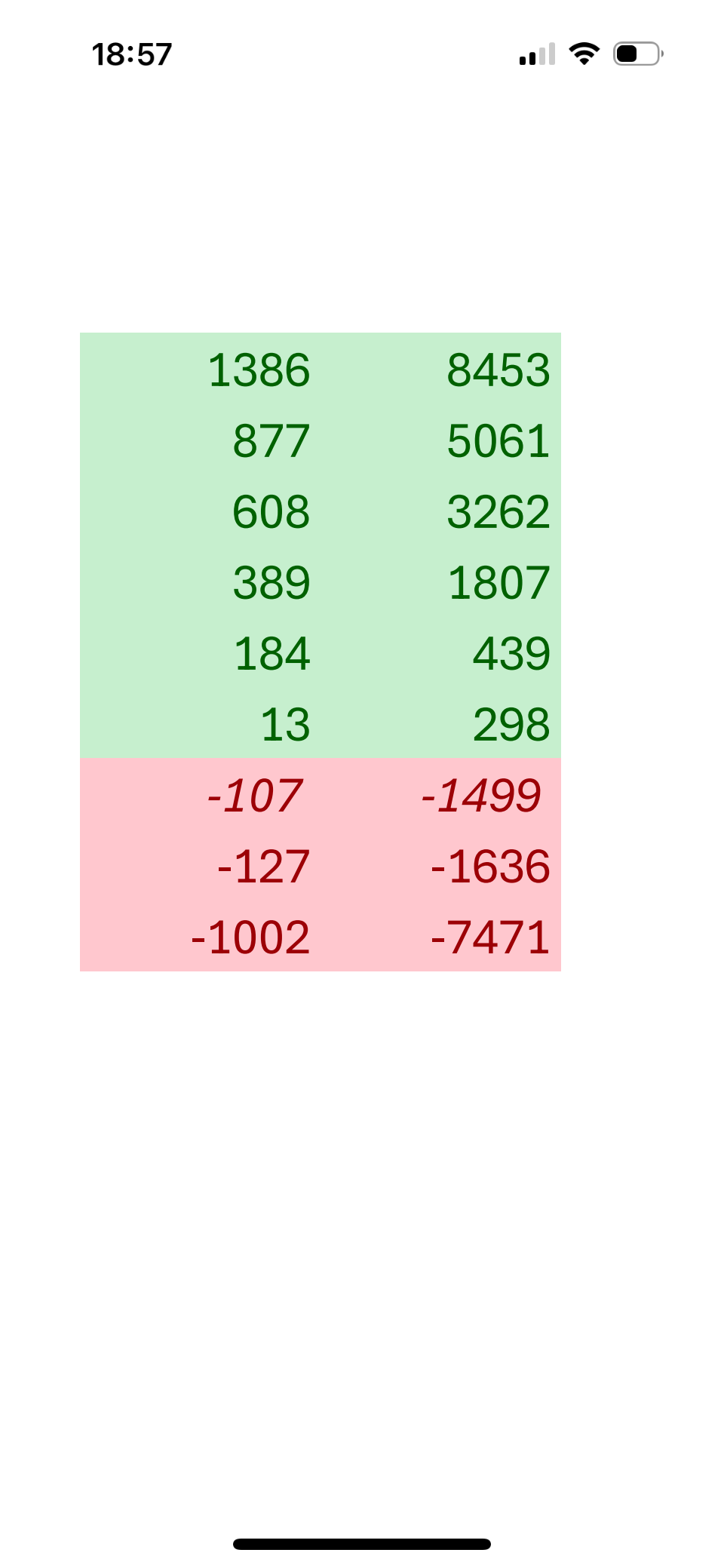

I've now done a direct comparison of various projections run from the modeller pre and post 3rd Apr 24

I have kept everything else the same and also added the uplift to the outcome. What you see below is the DIFFERENCE between the pre and post Apr projection - 1st column is PA pension and 2nd is TFLS.

The rows represent ages 66 to 60 going downwards (italics is an extra 60y1month projection), then jumping down again to 57.

So I just about do better if I retire at 61 (in about 4 years) but no earlier. I can probably live with being £100 a year worse off at 60 though but it might make my “flex at 57” plans more tricky…

I might ask for another full quote though given the discussion on “not implementing - or whatever” the new ERFs till October! 2

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards