We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

VOTE now! Proposed take over of Virgin Money - Nationwide members should be given a vote

Comments

-

From the most recent 2023 Glossarymasonic said:26left said:

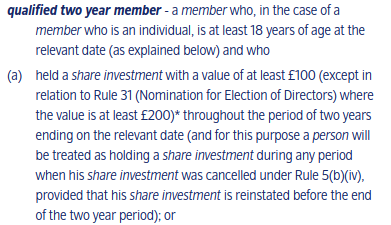

Have you checked that? I think most savings and current accounts (i.e. deposit accounts) are classed as a “share investment” under the rules? I think that would mean you DO qualify, provided you maintained a balance of £100 or more?masonic said:Did Mikael have any view about the requirement to be a two year qualifying member, meaning that they must have held either a share account or a mortgage for two years? This requirement excludes me for example as I only hold savings with Nationwide.Also, if the process is started today, then it must be completed by 6th July, but in 14(d)(ii), such a request will be denied if the meeting would need to fall between 5th May - 4th September.

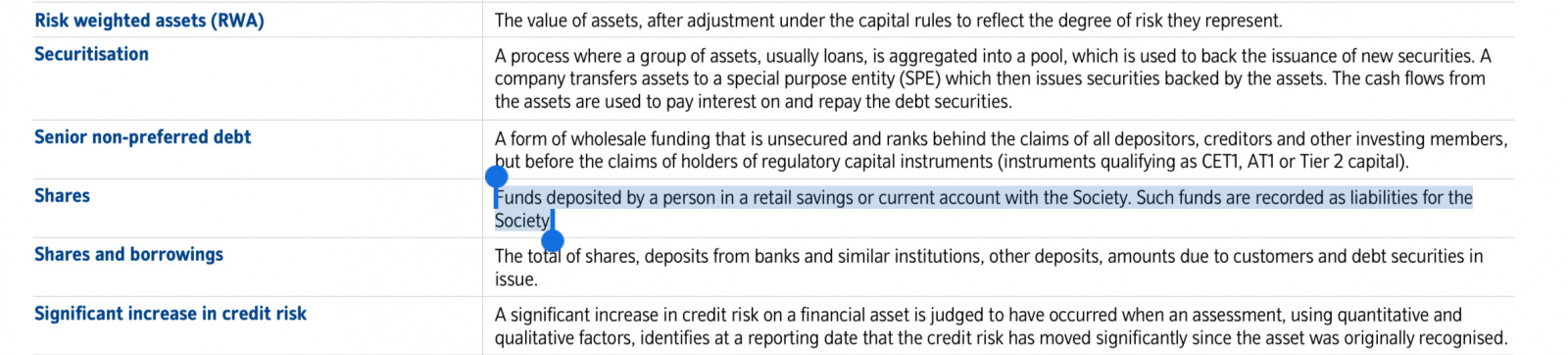

I've checked the T&Cs of my accounts and there is no mention of my savings being classed as shares.

I've checked the T&Cs of my accounts and there is no mention of my savings being classed as shares.

https://www.nationwide.co.uk/-/assets/nationwidecouk/documents/about/how-we-are-run/results-and-accounts/2022-2023/glossary-2023.pdf

You may also want to check with list here

https://www.nationwide.co.uk/about-us/fairer-share/terms-and-conditions/

Most current and savings accounts qualify.

Do your account T&Cs make reference to you being a member of the society and bound by its rules? Then I would wager it is a “share investment” account: you are investing - and you are sharing in membership.1 -

26left said:

From the most recent 2023 Glossarymasonic said:26left said:

Have you checked that? I think most savings and current accounts (i.e. deposit accounts) are classed as a “share investment” under the rules? I think that would mean you DO qualify, provided you maintained a balance of £100 or more?masonic said:Did Mikael have any view about the requirement to be a two year qualifying member, meaning that they must have held either a share account or a mortgage for two years? This requirement excludes me for example as I only hold savings with Nationwide.Also, if the process is started today, then it must be completed by 6th July, but in 14(d)(ii), such a request will be denied if the meeting would need to fall between 5th May - 4th September.I've checked the T&Cs of my accounts and there is no mention of my savings being classed as shares.

https://www.nationwide.co.uk/-/assets/nationwidecouk/documents/about/how-we-are-run/results-and-accounts/2022-2023/glossary-2023.pdfThen there are contradictory statements within the results and accounts vs the memorandum and rules of the society. The memorandum and rules has a whole section on Share Investments (rule 5), and it treats them as different than taking deposits in rule 4.But there's something of greater concern I missed earlier:

What are the chances that 500th qualifying two year member, even under the more generous definition proposed, will complete the required actions to enable this date not to already be in the past when the request becomes effective? And is it possible to countermand rule 14(f)'s requirement for due notice to be provided?26left said:The template email demands a meeting before 19th April.

1 -

Sweet, looking forward to voting on such a resolution at the meeting if it happens then26left said:

0 -

Section 14 f) stipulates maximums, not minimums. I read elsewhere that someone has asked the secretary of the society to specify how quickly a meeting can be called and held given the urgency.masonic said:26left said:

From the most recent 2023 Glossarymasonic said:26left said:

Have you checked that? I think most savings and current accounts (i.e. deposit accounts) are classed as a “share investment” under the rules? I think that would mean you DO qualify, provided you maintained a balance of £100 or more?masonic said:Did Mikael have any view about the requirement to be a two year qualifying member, meaning that they must have held either a share account or a mortgage for two years? This requirement excludes me for example as I only hold savings with Nationwide.Also, if the process is started today, then it must be completed by 6th July, but in 14(d)(ii), such a request will be denied if the meeting would need to fall between 5th May - 4th September.I've checked the T&Cs of my accounts and there is no mention of my savings being classed as shares.

https://www.nationwide.co.uk/-/assets/nationwidecouk/documents/about/how-we-are-run/results-and-accounts/2022-2023/glossary-2023.pdfThen there are contradictory statements within the results and accounts vs the memorandum and rules of the society. The memorandum and rules has a whole section on Share Investments (rule 5), and it treats them as different than taking deposits in rule 4.But there's something of greater concern I missed earlier:

What are the chances that 500th qualifying two year member, even under the more generous definition proposed, will complete the required actions to enable this date not to already be in the past when the request becomes effective? And is it possible to countermand rule 14(f)'s requirement for due notice to be provided?26left said:The template email demands a meeting before 19th April.

I think section 4 of the rules are more generic, not contradictory, because they define what the society does - taking share investments and providing mortgages are the membership parts, but they do offer other borrowing (eg personal loans) and take some deposits (eg from businesses) that fall outside the membership model.The chance is zero if people do nothing. The chance is higher if motivated people act.I think April 19th is relevant as that is the scheme convening date (ie court date) mentioned in the takeover docs.0 -

26left said:

Section 14 f) stipulates maximums, not minimums. I read elsewhere that someone has asked the secretary of the society to specify how quickly a meeting can be called and held given the urgency.masonic said:

What are the chances that 500th qualifying two year member, even under the more generous definition proposed, will complete the required actions to enable this date not to already be in the past when the request becomes effective? And is it possible to countermand rule 14(f)'s requirement for due notice to be provided?26left said:The template email demands a meeting before 19th April.I think April 19th is relevant as that is the scheme convening date (ie court date) mentioned in the takeover docs.Yes, maximum timelines are specified, but also that due notice must be given (this is to enable members to be notified and give them the opportunity to arrange to attend if they so desire or nominate a proxy). Rule 22 covers notice and states that for meetings, notice of the meeting must be sent so as to reach each eligible member at least 21 days before the last date for receipt of proxies, which of course must be before the date of the meeting itself. But even if this were not the case, it is physically impossible to hold a meeting on 19th April if the conditions for calling the meeting aren't fulfilled until after 19th April. Unless you possess a time machine.However, I've double checked the template email and contrary to what you have said, it does not demand a meeting before 19th April. If you've modified the email you've sent to include this that could invalidate it.I don't think it will be possible to hold a meeting before 4th May cut-off for the AGM period. That would therefore kick it into September, near to when the deal is expected to complete. That would be just for the resolution to hold a vote. If that passes, another meeting would need to be convened, subject to the same notice period, in order to hold the vote itself.2 -

I fully support the principle of members being given a vote on this. And indeed my interpretation of Section 92A of the Building Societies Act 1986 is that Nationwide are legally obliged to hold a vote (since subsection 3 and 4 both seem to apply to the transaction). But Section 92A(1) is a strangely toothless bit of legislation. It basically says (I'm paraphrasing here) "You must hold a vote if the following apply ...", but then goes on to say that failure to comply with the requirement to hold a vote doesn't invalidate the transaction. A bit like having a law which says that murder is illegal, but then if you commit a murder anyway, then they aren't going to do anything about it!

However, there is zero chance of this being accepted by Nationwide in its current form, even if you get 500 qualifying members. Nationwide will want every single i dotting and every t crossing, and will use any excuse possible to avoid holding a vote. There are some obvious flaws in the mechanics by which this is being done, which quite clearly aren't compliant with Rule 14.

Nominations by email won't work. Rule 14(c) says "The request must be in writing and received at the Society’s head office." The Interpretation section says "Any reference to writing or written or any similar expression includes a reference to any method of reproducing words in a legible form.", so that would arguably allow email. But it then goes on to say (all the subsequent bolding and underlining of words is added by me):

"Any reference to receipt at the Society’s head office or any similar expression means a document in paper form having been received at the Society’s head office by the Secretary of the Society or such other person as the Society may from time to time specify for the purpose."

Rule 14 requires: "It may consist of one or several documents in similar form, each signed by one or more qualified two year members."

How are proposers going to "sign" an email? Again the Interpretation section says "Any reference to signature or to something being signed or executed shall include either: (i) a signature printed or reproduced by mechanical or other means; (ii) any stamp or other distinctive marking made by or with the authority of the person required to sign the document to indicate it is approved by such person; or (iii) to the extent that the Board has approved this for the relevant purpose, an electronic signature or other means of verifying the authenticity of an electronic communication."

I don't think (i) or (ii) are going to apply, as proposers aren't being asked to add this to the emails. Has the Board approved electronic signatures for this purpose in order to comply with (iii)? Highly unlikely I would have thought.

Rule 14 requires the requests for a SGM to provide the necessary details (name, address, account number etc) and to send a £50 deposit. Until Nationwide have both, it isn't a valid request, and I would guess Nationwide will just totally ignore it. They aren't required to reply to the email and provide details of how to pay the £50, nor are they required to explain the reasons the SGM requests are not valid.

In my view, you need signed paper forms, accompanied by a cheque for £50 x number of enclosed forms.

As masonic has said, proposers need to be qualified two year members. This isn't made clear in the instructions, so there will be many people completing forms who aren't eligible and will be rejected.

Also, in the past I seem to recall that a building society (can't remember which one - possibly Portman, which subsequently merged with Nationwide) rejected requests for resolutions and/or directors nominations because they claimed that the account numbers provided needed to include all of the account numbers held during the two qualifying years, even for closed accounts (even though the rules don't actually require this).

As I said at the top, I support the principle of a vote, but this has been bodged. The timescales simply don't work, as masonic has noted. If you get to 500 members, then there is zero chance of Nationwide agreeing to a vote before the end of 4 May. So it would be 4 September at the earliest.

Can I just ask why Mikael didn't go for proposing a resolution at the AGM instead? This doesn't require a £50 deposit, 'just' 500 qualifying members. Much better chance of people going for this if they don't have to stump up any money! Too late now though, as the request would have to have been submitted by 4 April.

Good luck with it, but I'm afraid it is doomed fail.5 -

Your Nationwide accounts will definitely be shares. There was a time when building societies could offer both deposit accounts and share accounts. Share accounts gave you membership rights, and deposit accounts didn't. This was outlawed by the Building Societies Act 1997, and virtually all accounts opened nowadays have to be share accounts (with some limited exceptions). Societies are allowed to offer current accounts as deposit accounts, but I believe Nationwide's are share accounts.masonic said:

I've checked the T&Cs of my accounts and there is no mention of my savings being classed as shares.

There is a good summary here: https://www.bsa.org.uk/information/consumer-factsheets/savings-and-banking/difference-between-a-shareholder-and-a-depositor

6 -

So I'm going to stick my oar in once more.

My previous effort was a bit clumsy; I think I gave the impression that I felt the Nationwide board knows best. I absolutely do not think that. Following the demutualisation frenzy of the mid 2000s, a number of changes took place within Nationwide that, in my opinion, were not for the better.

In summary, the idea grew (I think mainly pushed by two people whose arrogance and bravado exceeded their abilities) that Nationwide needed to become 'more commercial' to compete with the banks. As such, new aggressive sales methods, setting high targets for staff, and (again in my opinion) hounding long serving employees out of their jobs if these targets weren't met. These staff were replaced by 'more commercially minded people', mainly from the banking sector. I think it's fair to say that a lot, if not most of these, were not the success they were hoped to be. But I digress.

Back to the matter in hand; I have no idea if this move by NBS is good for the long term. I am not qualified to judge it on its own merits. But like others on here, I do question whether the NBS board and top management team have genuine mutual principles at heart.

Nationwide in my time there had always been run by 'Nationwide people', who had come up through the ranks, and for whom mutuality was non-negotiable. That method had its own problems sometimes, but I trusted it far more than the current system of always appointing the top jobs from the non-mutual sector.

One final comment; Nationwide's promise not to close branches. Debbie Crosbie closed a lot of branches whilst at TSB.3 -

There was some press coverage for the petition overnight:

https://www.thisismoney.co.uk/money/markets/article-13278655/Petition-calling-Nationwide-members-say-takeover-Virgin-Money-track-hit-target-needed-call-special-meeting.html

2 -

Foxhouse said:So I'm going to stick my oar in once more.

My previous effort was a bit clumsy; I think I gave the impression that I felt the Nationwide board knows best. I absolutely do not think that. Following the demutualisation frenzy of the mid 2000s, a number of changes took place within Nationwide that, in my opinion, were not for the better.

In summary, the idea grew (I think mainly pushed by two people whose arrogance and bravado exceeded their abilities) that Nationwide needed to become 'more commercial' to compete with the banks. As such, new aggressive sales methods, setting high targets for staff, and (again in my opinion) hounding long serving employees out of their jobs if these targets weren't met. These staff were replaced by 'more commercially minded people', mainly from the banking sector. I think it's fair to say that a lot, if not most of these, were not the success they were hoped to be. But I digress.

Back to the matter in hand; I have no idea if this move by NBS is good for the long term. I am not qualified to judge it on its own merits. But like others on here, I do question whether the NBS board and top management team have genuine mutual principles at heart.

Nationwide in my time there had always been run by 'Nationwide people', who had come up through the ranks, and for whom mutuality was non-negotiable. That method had its own problems sometimes, but I trusted it far more than the current system of always appointing the top jobs from the non-mutual sector.

One final comment; Nationwide's promise not to close branches. Debbie Crosbie closed a lot of branches whilst at TSB.That reflects my own perception of the situation. Those at the top talk the talk, but don't walk the walk of mutuality. Those nearer the bottom aren't empowered, and the membership doesn't have the tools to make sure the top keeps to the principles of mutuality.Nationwide has drifted away from being a mutual, and the very thing that was supposed to stop hostile demutualisation (the memorandum and rules) now stands as a barrier to the membership being able to do anything about it.So whilst I fear this petition won't achieve the objective of stopping the takeover (and it isn't clear whether the takeover is good or bad), what it is doing is shining a light on Nationwide's 'democracy' and how little accountability the SMT have to the membership.The folk on these threads who have been taunting other forum members who are trying to make a difference are doing a disservice to Nationwide. If they are now gleeful at the prospect of being able to vote to ensure the 500 lose their deposits then it just shows their lack of understanding about what mutuality is about. We've had clear examples of folk simply not understanding how the mutual model works and what it means to own a share of a mutual building society. Maybe Nationwide should use some of their excess profits and advertising space to explain the mutual model, rather than to misleading claim to be better than the other banks? I.e. Walk the walk.4

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards