We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Abolished N.I - state pension system

Comments

-

I don't see any benefit. We'd still pay the same amount - whatever anybody else thinks and would we all really like it if taxes on our pension income rose drastically? No? So a lower tax rate for that then. No different to now.0

-

The Chancellor stated "This is the second fiscal event where we have reduced employee and self-employed national insurance. ... Our long -term ambition is to end this unfairness. ... we will continue to cut National Insurance as we have done today so we truly make work pay."Sarahspangles said:Some posts I’ve read seem to be people assuming that pensions are being abolished!

That appears to refer only to employee (and sole-trader) NI. There appears to be nothing related to employer NI.

He did not state that it was intended to abolish the State Pension.

https://www.gov.uk/government/speeches/spring-budget-2024-speech

In The Martin Lewis Money Show aired on ITV yesterday (12th March) there is an attempt at explaining why changes to NI and changes to SP are not linked.

It may be possible to view the programme on ITV Player or other streaming services.1 -

The thresholds/limits are based on earnings and there is no reason why they would not still exist.TheGardener said:Sorry if I'm being dim and I have tried to find answers in existing threads...I heard the government wants to abolish N.I. and we all just pay into 'one tax pot'. If this happens - how will the state pension entitlement be worked out?

Remember that you do not need to pay NI to qualify as if you have been paying NI.I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

What is the benefit?westv said:I don't see any benefit. We'd still pay the same amount - whatever anybody else thinks and would we all really like it if taxes on our pension income rose drastically? No? So a lower tax rate for that then. No different to now.

a) Fairer as people pay the same amount of tax on earned and non-earned income (so employees would pay a bit less and rich pensioners would pay more).

b) Simpler as there is one tax with one set of thresholds, which means easier to understand and cheaper for employers.

Yes pensioners would pay more and would need some protection, easily provided by raising tax thresholds specifically for pensioners, e.g. if we assume basic rate goes up by less than the % of NI because of the extra tax payers. I think basic rate would be 25%, give pensioners an extra £3500 personal allowance, those under £30,000 would pay less while those on £30,000 and above would start to pay more tax.

Disadvantages

- It is a change so there will be winners and losers.

- Simplified taxes might make some types of avoidance easier.

- Need to calculate entitlements associated with NI differently?3 -

In my experience "simplified" is just another word for "more expensive".0

-

The Chancellor used his Budget earlier this month to set out a 2p cut in national insurance from April with a vague promise to deliver a simpler tax system by eventually getting rid of it altogether.

Giving evidence to the Treasury Committee on Wednesday, the Chancellor said: “It won’t happen in one Parliament, but it’s a long-term ambition.”

He also said: “This is going to be the work of many Parliaments.

1 -

People don’t talk enough about this, but it is so important in our discussions on benefits.MattMattMattUK said:

Highly unlikely to be introduced by the Conservatives because it would be their target demographic and voters who would get means tested out of getting a pension and unlikely to be introduced by Labour because it would end up causing the death of the state pension overall which would go against their ideology. Plus, pensioners generally vote, both parties want to court that and in reality I am not voting for a party that attempts to take away something I would have spent my life paying in for.SouthCoastBoy said:That could be the point when you introduce means testing?

Also, abolishing NI is not likely to be practical, at least in a pure tax cut sense, if NI drops then Income Tax would likely need to rise proportionately, so we can have no NI, but then we would also need 28% starting rate of Income Tax. As we cannot afford the previous 2% cut or the new 2% cut, we certainly cannot afford a further 8% cut.

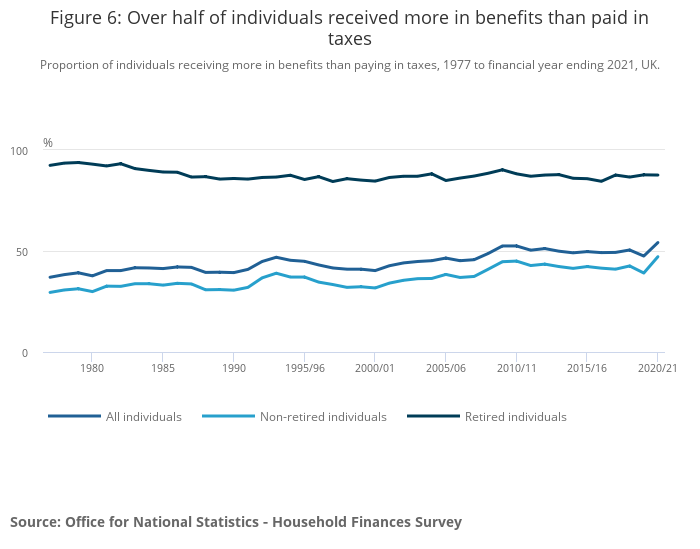

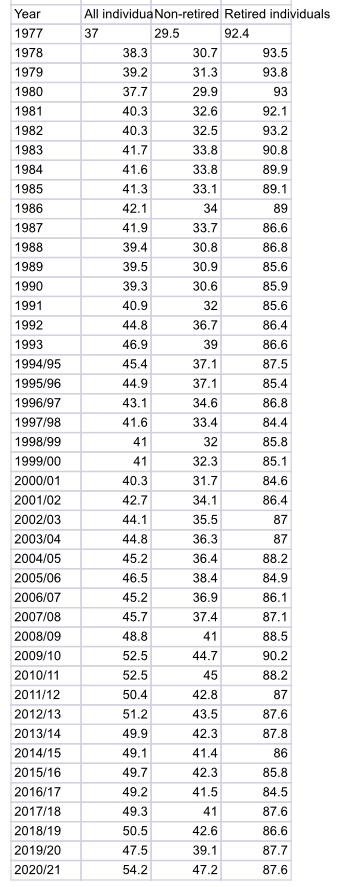

Follow the trend line from 1977 (37%) and you will see that fewer and fewer of all households make a NET positive contribution to the public purse.

It’s now over 50% (54.2% for Year Ending 2021 with the furlough) NET draining. 53.8% for Year Ending 2022.

When you look at working age households it’s nearly 50% NET taking now also.

This doesn’t look sustainable to me longer term. With less than half of UK households making a NET tax contribution after benefits received.

Which is why the SP will become means tested in my view. Data is here:2

Data is here:2 -

It is worth recalling that 2 years ago as Chancellor of the Exchequer, Rishi Sunak announced a big increase to the rate of National Insurance (to 15.05%) and also that the basic rate of income tax would be reduced to 19% in 2024, and then separately pledged during 2022 that income tax would be reduced to 16% by 2029.

Given such a significant change of direction in taxation policy over such a short period, questions have to be asked about whether there is a long-term commitment to a strategy of NI reduction, or whether it is just political opportunism.

In the betting market, the Conservatives are currently given a 10% chance of winning most seats at the next Election, so any long-term ambitions may be of little relevance anyhow.0 -

While not disagreeing with your general point, the chart ending during COVID is probably not a good place to set any assessment against. That was a very exceptional period. Any assessment possibly needs to consider up to 2019-20 and then from 2022-23 so that COVID distortions are mitigated.BlackKnightMonty said:

Follow the trend line from 1977 (37%) and you will see that fewer and fewer of all households make a NET positive contribution to the public purse.

In some ways, a simpler tax system might then make it easier to close loopholes.2 -

Here is the data (excluding year ending 2022 which is 53.8%). It’s been neigh on 50% for a decade. Grumpy_chap said:

Grumpy_chap said:

While not disagreeing with your general point, the chart ending during COVID is probably not a good place to set any assessment against. That was a very exceptional period. Any assessment possibly needs to consider up to 2019-20 and then from 2022-23 so that COVID distortions are mitigated.BlackKnightMonty said:

Follow the trend line from 1977 (37%) and you will see that fewer and fewer of all households make a NET positive contribution to the public purse.

In some ways, a simpler tax system might then make it easier to close loopholes.

Sorry it has added it above - I can’t seem to fix that!

0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards