We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Transition Arrangements for PCLS following abolition of LTA in April

Comments

-

In my post above i said …peterg1965 said:Really appreciative of the time you took to respond, thanks @FIREDreamer

One last question, which provider would i apply to for the transitional certificate, and does it matter? My SIPP is with InvestAcc (Minerva SIPP) and my workplace pensions is Scottish Widows, via the Mercer Master Trust Company Retirement scheme. My intent is to make a partial transfer out of the MMT workplace scheme and into my SIPP, so I can crystalize another portion of the funds to get the PCLS.So, i guess it makes sense to ask InvestAcc

Please refer to FAQ 7 and 8 here …

https://www.gov.uk/government/publications/pension-schemes-newsletter-155-january-2024/newsletter-155-january-2024

In this document we have …“The application must be made by the member, and guidance will confirm that we expect applications to be made to the scheme from which the first lump sum is being paid post after 6 April 2024.”

Makes sense because you lose the right to a certificate if you crystallise post April 2024 without obtaining one.

….. So who do you intend crystallising with first post April 2024? That’s your answer.") 1

1 -

One last question, which provider would i apply to for the transitional certificate, and does it matter?You apply to the one you intend to take the drawdown from.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Emailed my SIPP provider this morning - InvestAcc (Minerva SIPP) and received an email this afternoon with the application form for the TTFAC. I have now located all of the supporting paperwork for my 3 x Benefit Crystallisation Events. The 2nd and 3rd, both taken when I was with Fidelity are very clear, with plan number, tax free amount and LTA %. The first was received on initial receipt of my AFPS DB pension, which states the amount of pension, LTA % and the 'Terminal Grant of £100,426.59' which I assume my SIPP administrators will interpret as the tax free PCLS amount.

I intend to review again tomorrow, complete the form, scan it all and send to the SIPP administrators. Will report back when I get (a hopefully) favourable response!

1 -

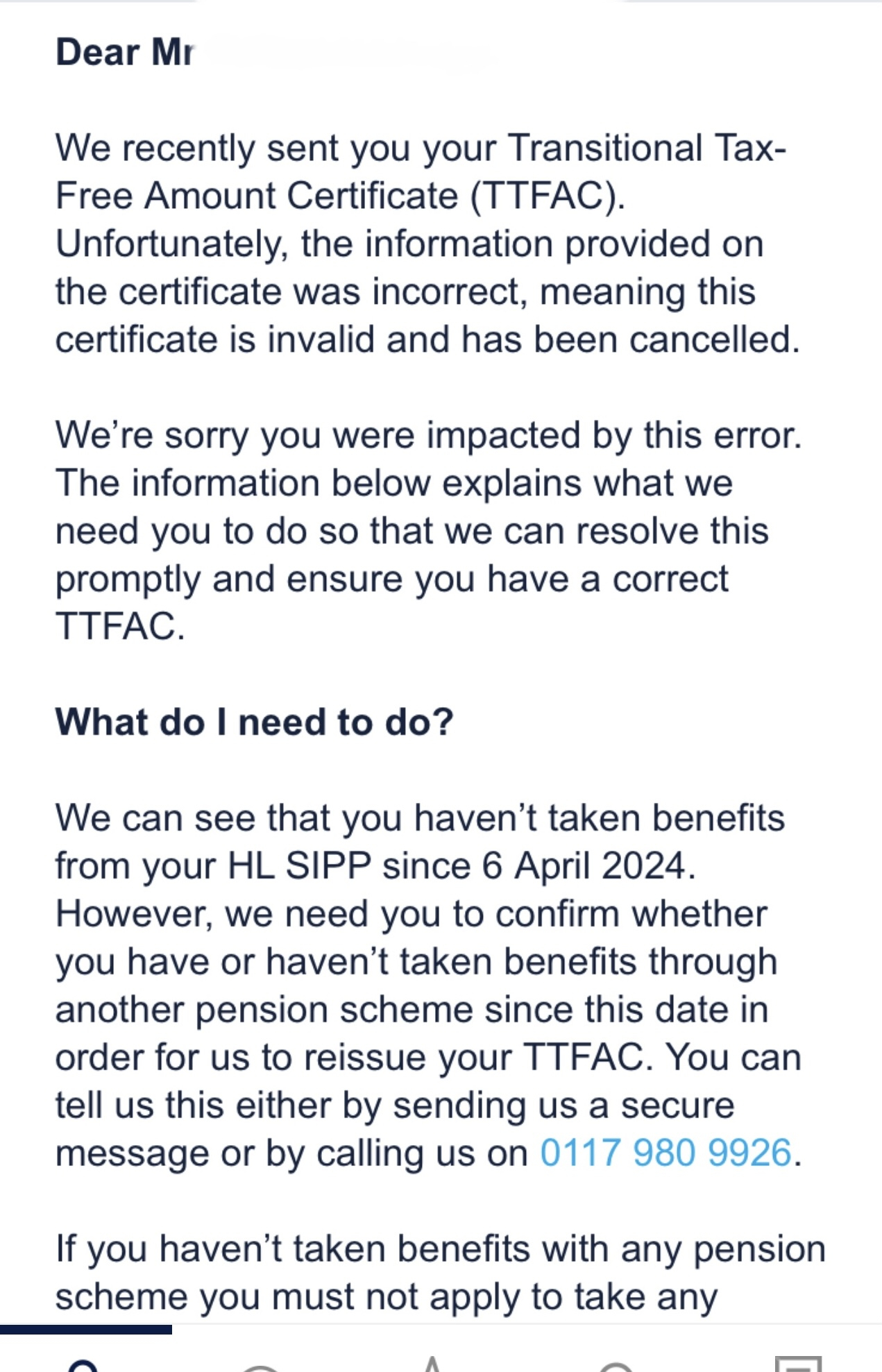

Oh fudge, wonder what the issue is.

0 -

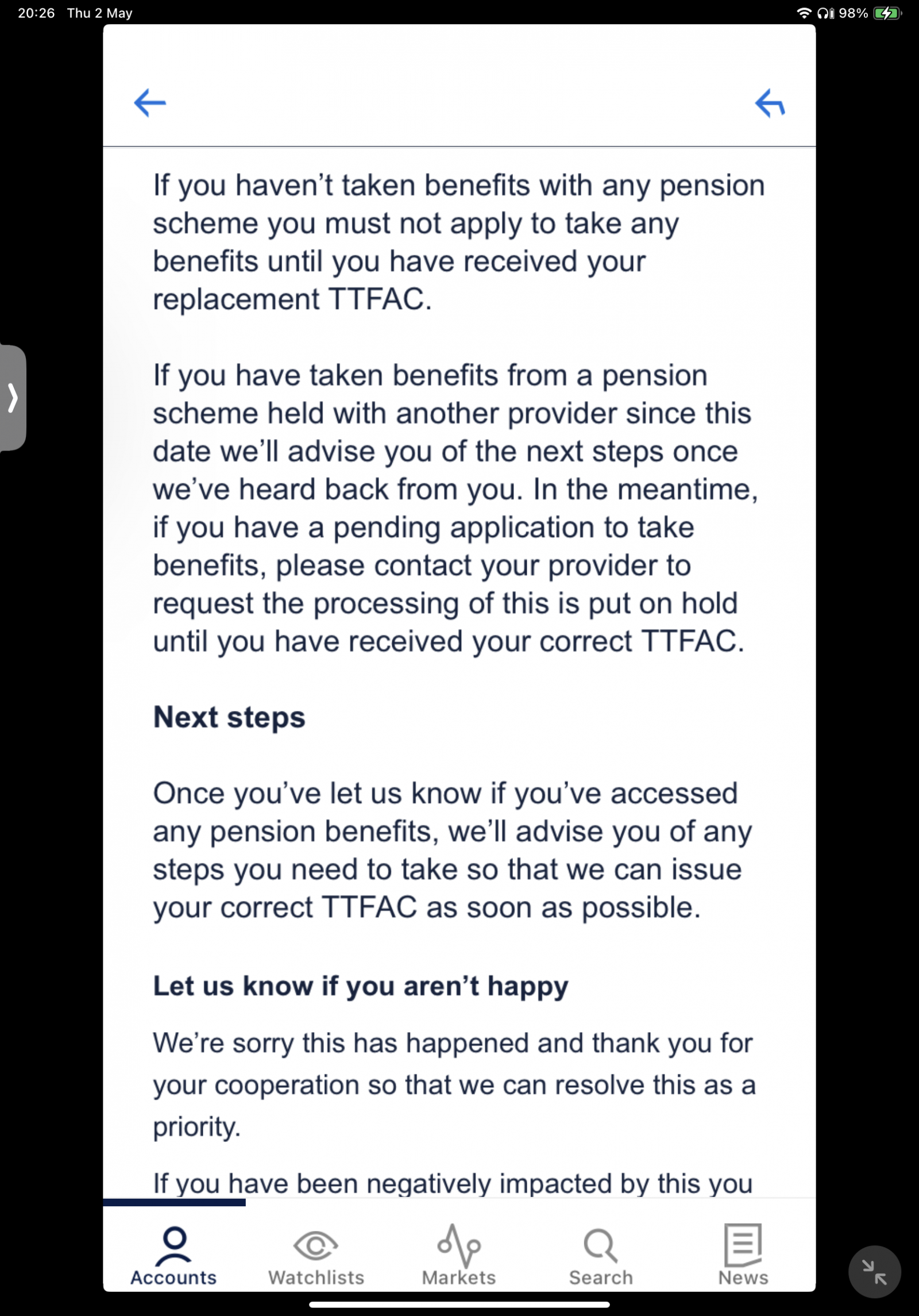

Well if that message is complete then it seems they just want you to confirm that since April 6th you've not taken any tax-free amounts from anywhere else - my understanding is that taking money from a crystallised pot is ok, but you can't access any new tax-free money from 6th April onwards and then afterwards ask for a TTFAC.FIREDreamer said:Oh fudge, wonder what the issue is.

Though I wonder what would happen if after receiving the certificate you did take tax-free money out from somewhere else or even from HL? Hopefully they could still reissue it.0 -

Though I wonder what would happen if after receiving the certificate you did take tax-free money out from somewhere else or even from HL? Hopefully they could still reissue it.As the rules currently stand, you cannot amend a TTFAC. They can only be cancelled and then reapplied for. However, if you have done a BCE after it has been cancelled, you cannot then apply for a new one and you lose out.

Many of the providers are not rushing out TTFACs because of a range of issues and the risks involved. They don't want to get caught out with some bits still unresolved pending further legislation.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

I had already confirmed that though. Have confirmed it again. Rest of message …Notepad_Phil said:

Well if that message is complete then it seems they just want you to confirm that since April 6th you've not taken any tax-free amounts from anywhere else - my understanding is that taking money from a crystallised pot is ok, but you can't access any new tax-free money from 6th April onwards and then afterwards ask for a TTFAC.FIREDreamer said:Oh fudge, wonder what the issue is.

Though I wonder what would happen if after receiving the certificate you did take tax-free money out from somewhere else or even from HL? Hopefully they could still reissue it.

1 -

So if you have taken some PCLS from a DB pension, and got an LTA% at the time, recalculation seems to mean you will have more deducted from the fixed TFC allowance than you actually received in cash.Does the residual amount allowed by the calculation then a) get reduced as an amount by the £ value of any future TFC from a DC pension, or b) do further calculations have to be made?I feel a) should be the case, but would be interested to confirm.0

-

If you crystallised when the LTA was higher eg at £1.8 million you could have got far more tax free cash than the default transitional calculation assumes. So applying for a TTFA could reduce tax free cash available.FIREDreamer said:

Absolutely no idea - maybe some odd cases.peterg1965 said:

I can’t see why I wouldn’t do this as it’s the difference between £29k (not good) and £95k (good) If the information i provide is correct why would it be something that I wouldn’t do, acknowledging that once issued it cannot be reversed?FIREDreamer said:

The amount on the transitional certificate is a monetary amount. As stated above once you get one you cannot change your mind.peterg1965 said:That’s great thank you and a bit of a relief to be honest. I was about to start the process of taking a further PCLS, in complete ignorance, so thankful I stumbled across this post! I just thought it would be done on actual monetary figures, not %s - silly me!

Do you know what form I need to complete and assume it goes to HMRC? 0

0 -

I crystallised my pensions when the LTA was £1.05m and £1.073m. Some DB was taken with no tax free cash. No LTA left. With no certificate I have no tax free cash available.zagfles said:

If you crystallised when the LTA was higher eg at £1.8 million you could have got far more tax free cash than the default transitional calculation assumes. So applying for a TTFA could reduce tax free cash available.FIREDreamer said:

Absolutely no idea - maybe some odd cases.peterg1965 said:

I can’t see why I wouldn’t do this as it’s the difference between £29k (not good) and £95k (good) If the information i provide is correct why would it be something that I wouldn’t do, acknowledging that once issued it cannot be reversed?FIREDreamer said:

The amount on the transitional certificate is a monetary amount. As stated above once you get one you cannot change your mind.peterg1965 said:That’s great thank you and a bit of a relief to be honest. I was about to start the process of taking a further PCLS, in complete ignorance, so thankful I stumbled across this post! I just thought it would be done on actual monetary figures, not %s - silly me!

Do you know what form I need to complete and assume it goes to HMRC?

I have received a revised certificate today and the numbers in it look like they were calculated by Diane Abbott and are clearly wrong.

Rounding the figures here for privacy. I have already taken tax free cash of £245,000 and have no LTA left. My “corrected” certificate states …

Lump sum transitional tax-free amount: £245,000.00

Lump sum and death benefit transitional tax-free amount: £245,000.00

🤣🤣🤣

Its obvious what the error this time is. The former should be deducted from £268,275 (to give £23,275) and the latter deducted from £1,073,100 (to give £828,100).No apology for the previous error which seems to be just £90 too high on the first transitional tax free cash figure and presumably the same on the death benefit figure. No confirmation from them of what the error was either. The £90 error is based on me calculating the correct figure myself.

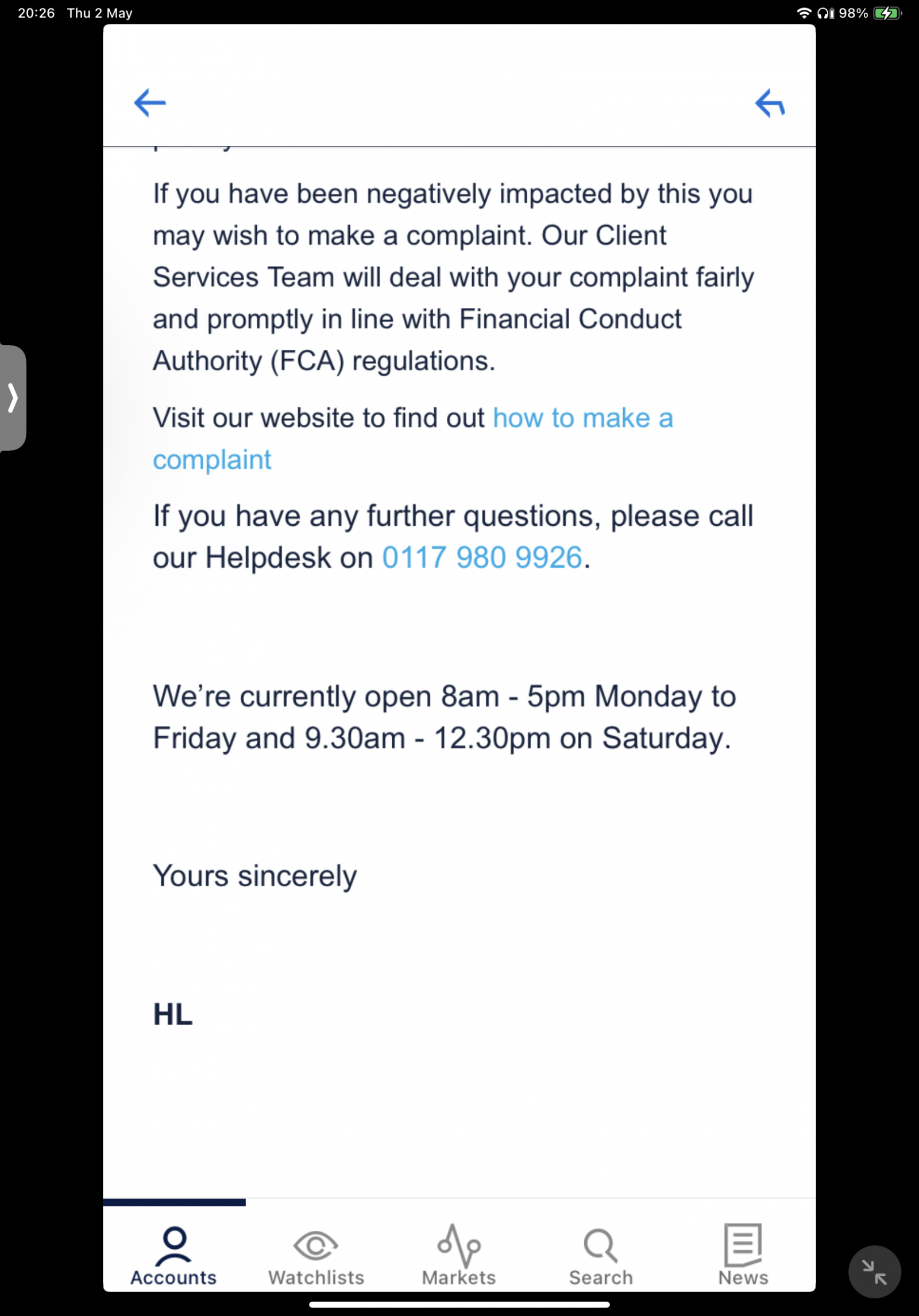

I don’t think there is an excuse for producing figures on the certificate that are clearly garbage. Complaint raised.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards