We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Transition Arrangements for PCLS following abolition of LTA in April

Comments

-

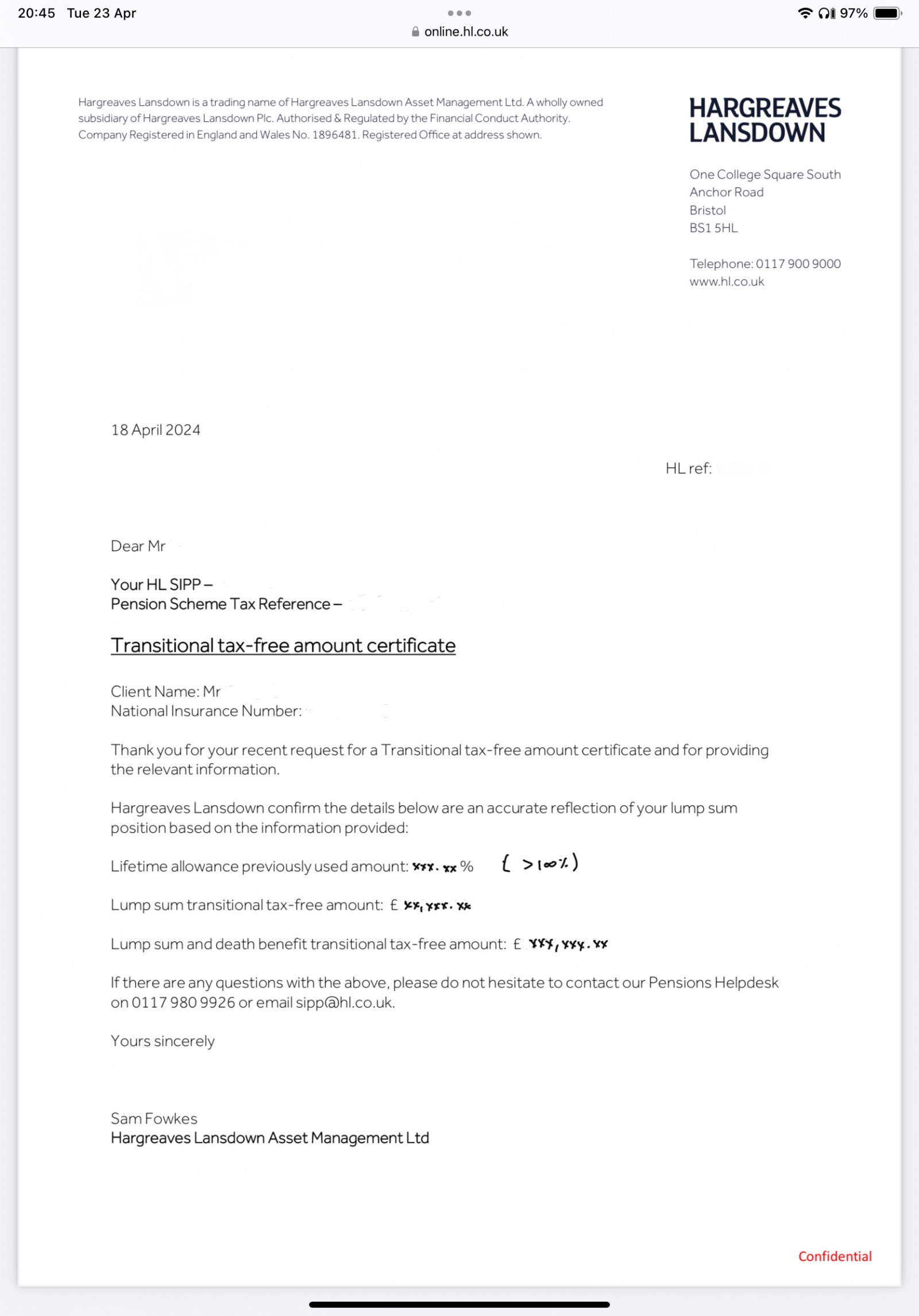

Well, I got my transitional certificate via secure message today so Hargreaves Lansdown produced it in a week. This is what it looks like, for your information, actual figures redacted for privacy.

1 -

Thanks so much for this, certainly helps my 'negotiations'0

-

Oh my goodness. I thought i understood the impact of the new Lump Sum Allowance rules and I thought i have significant more headroom in the Lump Sum Allowance than I may actually have.

My situation:

I received my Armed Forces Pension DB Pension (AFPS 75) in May 2015 aged 49. I received an immediate pension and a tax free lump sum. I also did a resettlement commutation that gave me an extra £15k (I think) tax free for a small reduction in pension, which was then restored back to where it would have been at aged 55. I believe this additional tax free commutation amount does not count towards the Lump Sum Allowance (tell me if i am wrong).

So, in May 2015 the figures were 61.59% LTA used and a tax free PCLS of c£100k (I need to find the exact figure).

I also have a SIPP and have had one since 2007.

In September 2020 (at 55) I used a further 23.76% of LTA and took a PCLS from the SIPP of £64,500

In March 2023 i used a further 3.66% of LTA and took a PCLS of c£10000.

I haven't taken any pension benefits form the SIPP above the PCLS. and i have used 89.01% of the old LTA.

The above means that in money terms so far I have received (£100k + £64.5k + £10k ) + £174.5.5K in Tax Free PCLS. Leaving me with about £94K left to use, or so i thought,

Using the formula seen in this post

Remaining lump sum allowance = £268,275 – (25% x previously used % of lifetime allowance on 5 April 2024 x £1,073,100).

In my case:

Remaining LSA = £268,275- 25% of 89.01% x £1073100 = £238791. Which means it says I have used about £63k more PCLS than I have actually received.

Am I doing something wrong here? Does this mean I have to apply for some form of transitional certificate so that I am able to take my actual full LSA of £268750?

Any help appreciated as this has some significant ramifications on future pension and retirement planning!

0 -

If you do NOT apply for a transitional certificate you can take a maximum PCLS of £268,275 - £238,791 = £29,284.peterg1965 said:Oh my goodness. I thought i understood the impact of the new Lump Sum Allowance rules and I thought i have significant more headroom in the Lump Sum Allowance than I may actually have.

My situation:

I received my Armed Forces Pension DB Pension (AFPS 75) in May 2015 aged 49. I received an immediate pension and a tax free lump sum. I also did a resettlement commutation that gave me an extra £15k (I think) tax free for a small reduction in pension, which was then restored back to where it would have been at aged 55. I believe this additional tax free commutation amount does not count towards the Lump Sum Allowance (tell me if i am wrong).

So, in May 2015 the figures were 61.59% LTA used and a tax free PCLS of c£100k (I need to find the exact figure).

I also have a SIPP and have had one since 2007.

In September 2020 (at 55) I used a further 23.76% of LTA and took a PCLS from the SIPP of £64,500

In March 2023 i used a further 3.66% of LTA and took a PCLS of c£10000.

I haven't taken any pension benefits form the SIPP above the PCLS. and i have used 89.01% of the old LTA.

The above means that in money terms so far I have received (£100k + £64.5k + £10k ) + £174.5.5K in Tax Free PCLS. Leaving me with about £94K left to use, or so i thought,

Using the formula seen in this post

Remaining lump sum allowance = £268,275 – (25% x previously used % of lifetime allowance on 5 April 2024 x £1,073,100).

In my case:

Remaining LSA = £268,275- 25% of 89.01% x £1073100 = £238791. Which means it says I have used about £63k more PCLS than I have actually received.

Am I doing something wrong here? Does this mean I have to apply for some form of transitional certificate so that I am able to take my actual full LSA of £268750?

Any help appreciated as this has some significant ramifications on future pension and retirement planning!

If you DO apply for a transitional certificate you can take a maximum PCLS of £268,275 - £174,500 = £93,775.

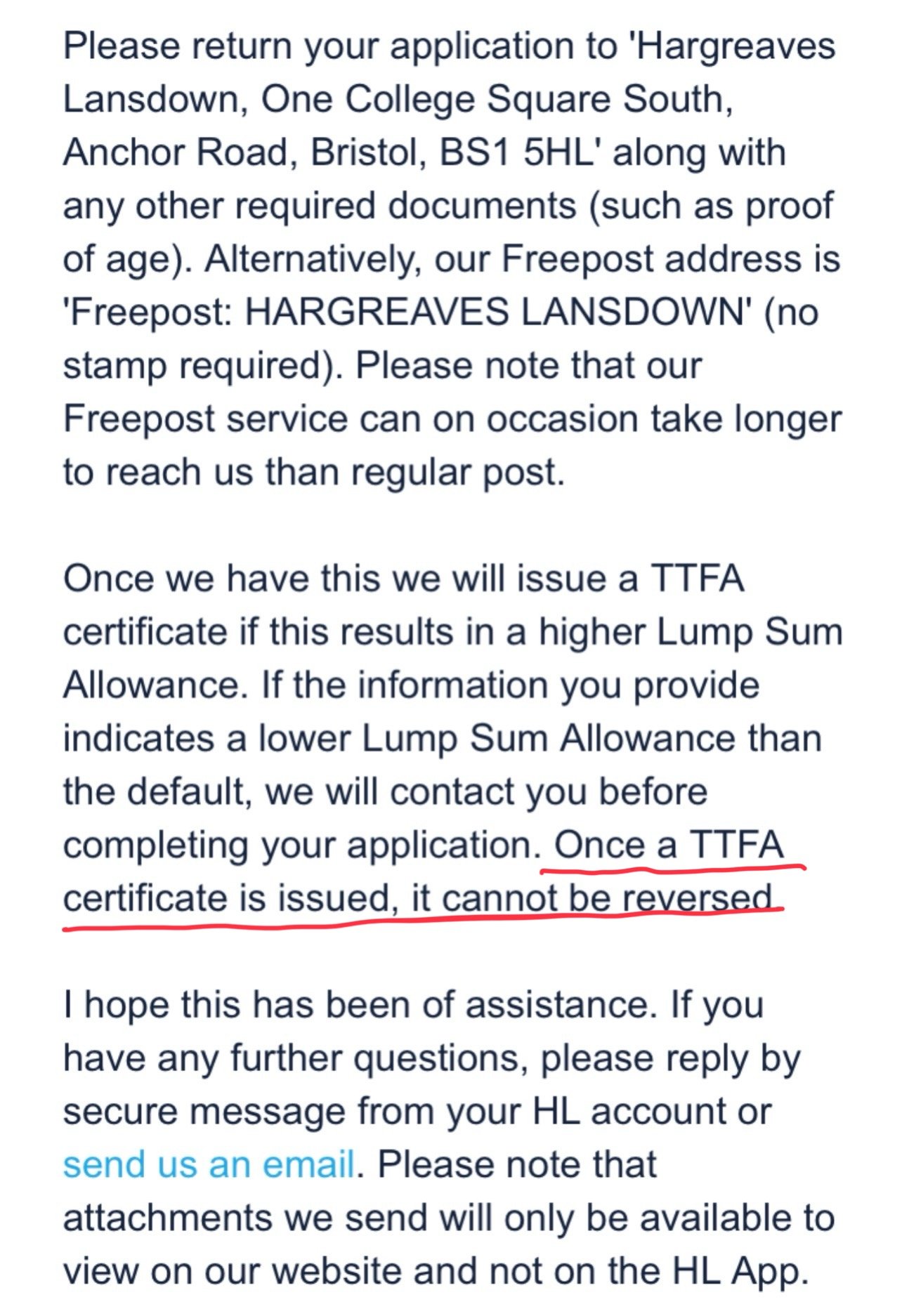

You must not crystallise ANY PENSION between 6 April 2024 and receipt of the certificate otherwise it is invalid.The certificate will state the above figure as an amount. Once you get a certificate you cannot change your mind. Hopefully this means that a labour government cannot invalidate it either.

EDIT: Assumes the additional tax free commutation has no impact - adjust my second figure down accordingly if it does.4 -

That’s great thank you and a bit of a relief to be honest. I was about to start the process of taking a further PCLS, in complete ignorance, so thankful I stumbled across this post! I just thought it would be done on actual monetary figures, not %s - silly me!

Do you know what form I need to complete and assume it goes to HMRC?0 -

I sent my provider the following message (actually two messages, combined here so may appear repetitive), you may be able to send similar to yours …peterg1965 said:That’s great thank you and a bit of a relief to be honest. I was about to start the process of taking a further PCLS, in complete ignorance, so thankful I stumbled across this post! I just thought it would be done on actual monetary figures, not %s - silly me!

Do you know what form I need to complete and assume it goes to HMRC?

Hi

Please refer to FAQ 7 and 8 here …

https://www.gov.uk/government/publications/pension-schemes-newsletter-155-january-2024/newsletter-155-january-2024

Even though i have used 100% LTA I did not take any tax free cash from my XYZ defined benefit pension so i do have some tax free cash available after April.

It appears that it is yourselves that need to generate the transitional lump sum certificate per the above guidance as this is the scheme i wish to draw the available tax free cash from.

I plan to apply for a TTFA Certificate before crystallising any further pension benefits. This is because despite not having any LTA left, I did not take any tax free cash when putting my XYZ defined benefit pension into payment.

I understand that the earliest I can apply for a certificate is 6 April 2024.

Can you please send me any forms I need to complete to obtain this TTFA transitional lump sum certificate so I can obtain the certificate asap after 6 April as I am retiring in June.

0 -

The amount on the transitional certificate is a monetary amount. As stated above once you get one you cannot change your mind.peterg1965 said:That’s great thank you and a bit of a relief to be honest. I was about to start the process of taking a further PCLS, in complete ignorance, so thankful I stumbled across this post! I just thought it would be done on actual monetary figures, not %s - silly me!

Do you know what form I need to complete and assume it goes to HMRC?

0 -

I can’t see why I wouldn’t do this as it’s the difference between £29k (not good) and £95k (good) If the information i provide is correct why would it be something that I wouldn’t do, acknowledging that once issued it cannot be reversed?FIREDreamer said:

The amount on the transitional certificate is a monetary amount. As stated above once you get one you cannot change your mind.peterg1965 said:That’s great thank you and a bit of a relief to be honest. I was about to start the process of taking a further PCLS, in complete ignorance, so thankful I stumbled across this post! I just thought it would be done on actual monetary figures, not %s - silly me!

Do you know what form I need to complete and assume it goes to HMRC?0 -

Absolutely no idea - maybe some odd cases. For me it was a choice between no PCLS (no LTA left) or a PCLS of over £20k. So why not indeed. Shame I needlessly paid LTA charges in 2022/23 before the budget when I could have left that in excess of LTA uncrystallised. C’est la vie.peterg1965 said:

I can’t see why I wouldn’t do this as it’s the difference between £29k (not good) and £95k (good) If the information i provide is correct why would it be something that I wouldn’t do, acknowledging that once issued it cannot be reversed?FIREDreamer said:

The amount on the transitional certificate is a monetary amount. As stated above once you get one you cannot change your mind.peterg1965 said:That’s great thank you and a bit of a relief to be honest. I was about to start the process of taking a further PCLS, in complete ignorance, so thankful I stumbled across this post! I just thought it would be done on actual monetary figures, not %s - silly me!

Do you know what form I need to complete and assume it goes to HMRC?1 -

Really appreciative of the time you took to respond, thanks @FIREDreamer

One last question, which provider would i apply to for the transitional certificate, and does it matter? My SIPP is with InvestAcc (Minerva SIPP) and my workplace pensions is Scottish Widows, via the Mercer Master Trust Company Retirement scheme. My intent is to make a partial transfer out of the MMT workplace scheme and into my SIPP, so I can crystalize another portion of the funds to get the PCLS.So, i guess it makes sense to ask InvestAcc0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards