We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

40k at zero interest SHOCKER!

Comments

-

I'd have thought that the Coventry account would be suitable - easy to manage on line via PC.1

-

Or the HSBC bonus saver at 4% if you don’t make any withdrawals in the month if he doesn’t want to change banks1

-

elkiedee said:OP says this relative would like something similar to the rates he's getting (well over 4% I think), can be online and limited access but not app only based. HSBC savings rates are literally better than nothing, but they're not going to match that. On 40K, 1% is £400.

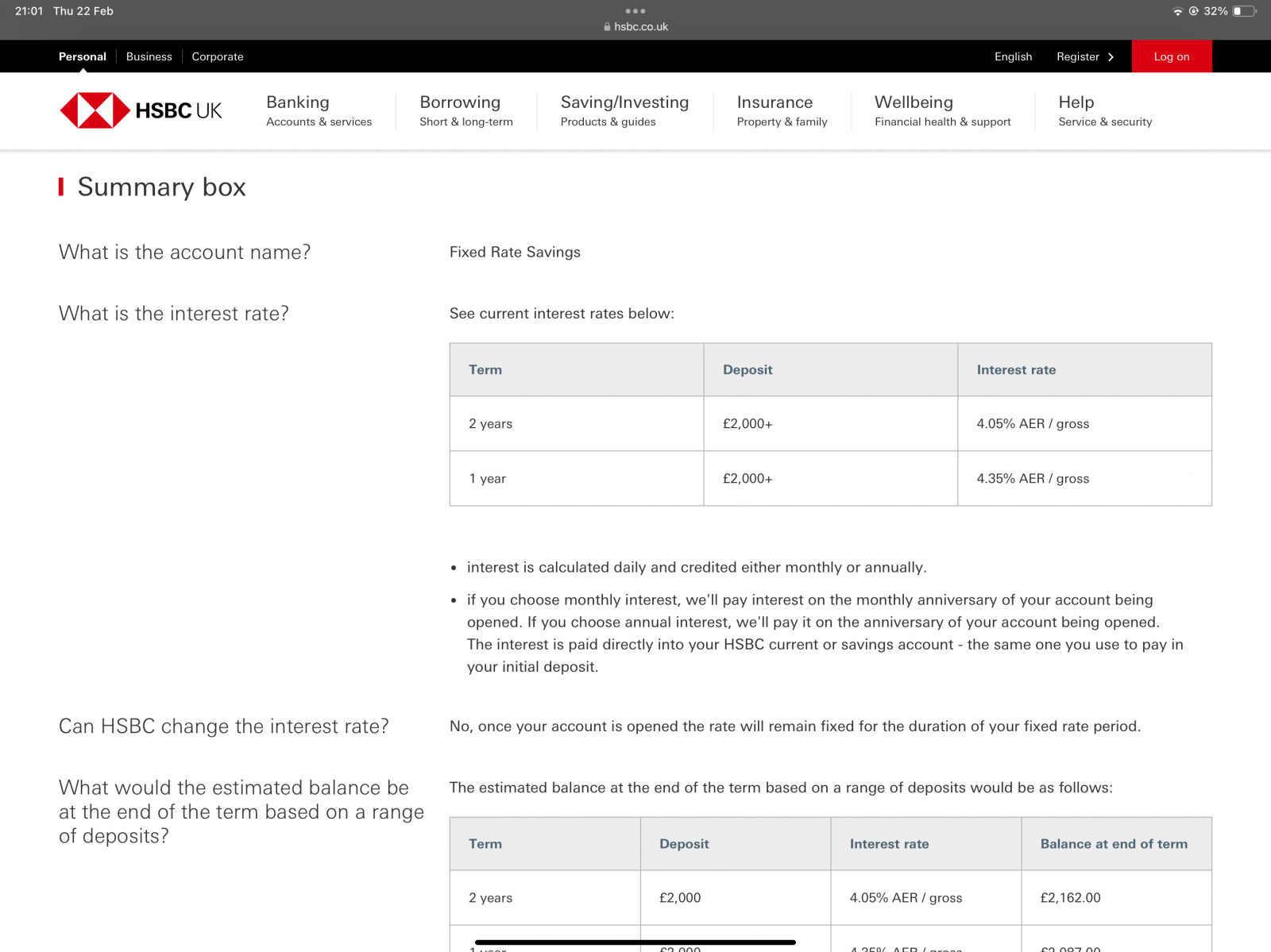

HSBC have 1 year fixed rate at 4.35% for >£2000, and a bit more for longer fixes (half-way down my link. Instant access at banks tends to be poor, but it can still be worth keeping a small amount at that rate for flexibility, if your current account is with them.

1 -

Most savings providers are not app based. Many will have an app but you are not obliged to use it.elkiedee said:OP says this relative would like something similar to the rates he's getting (well over 4% I think), can be online and limited access but not app only based. HSBC savings rates are literally better than nothing, but they're not going to match that. On 40K, 1% is £400.

1 -

That has been the usual norm, but currently you typically get a lower rate of interest for fixing for a few years.jacksonreed003 said:As your family member doesn't need regular access to the money then they could explore options like certificates of deposit (CDs) or longer-term saving accounts because they typically offer higher interests rates in exchange for locking in the funds for a set period of time. Or advice them to diversify their savings across multiple accounts to maximize their returns while still maintaining accessibility to their funds.

That is because it is expected that prevailing interest rates will slowly drop off in the coming couple of years.2 -

Hi. Isn't the devil in the details. Is that on the whole amount?LHW99 said:elkiedee said:OP says this relative would like something similar to the rates he's getting (well over 4% I think), can be online and limited access but not app only based. HSBC savings rates are literally better than nothing, but they're not going to match that. On 40K, 1% is £400.

HSBC have 1 year fixed rate at 4.35% for >£2000, and a bit more for longer fixes (half-way down my link. Instant access at banks tends to be poor, but it can still be worth keeping a small amount at that rate for flexibility, if your current account is with them.

I have noticed banks offer good rates and then the small print says "on the first [insert small amount here]"0 -

That's why you need to read the terms but this looks straightforward:JamesNoBonds said:

Hi. Isn't the devil in the details. Is that on the whole amount?LHW99 said:elkiedee said:OP says this relative would like something similar to the rates he's getting (well over 4% I think), can be online and limited access but not app only based. HSBC savings rates are literally better than nothing, but they're not going to match that. On 40K, 1% is £400.

HSBC have 1 year fixed rate at 4.35% for >£2000, and a bit more for longer fixes (half-way down my link. Instant access at banks tends to be poor, but it can still be worth keeping a small amount at that rate for flexibility, if your current account is with them.

I have noticed banks offer good rates and then the small print says "on the first [insert small amount here]" 0

0 -

I have already made that mistake with my own money. On a 3 year fixed saver. Though I was under the impression that the interest rate remains fixed even it it were to down overall in say year 2.Albermarle said:

That has been the usual norm, but currently you typically get a lower rate of interest for fixing for a few years.jacksonreed003 said:As your family member doesn't need regular access to the money then they could explore options like certificates of deposit (CDs) or longer-term saving accounts because they typically offer higher interests rates in exchange for locking in the funds for a set period of time. Or advice them to diversify their savings across multiple accounts to maximize their returns while still maintaining accessibility to their funds.

That is because it is expected that prevailing interest rates will slowly drop off in the coming couple of years.0 -

I agree lots of savings providers are not app-only based and have other options for use - but I think I was responding to someone who suggested that someone could get a phone and pay for it with the interest earned. Which is kind of missing the point. I have a phone and have sorted out being able to check balances, but for opening savings accounts, moving money and paying bills, I prefer to log in on a larger screen. My partner is a few years older than me but he's very comfortable doing these things on his phone.Albermarle said:

Most savings providers are not app based. Many will have an app but you are not obliged to use it.elkiedee said:OP says this relative would like something similar to the rates he's getting (well over 4% I think), can be online and limited access but not app only based. HSBC savings rates are literally better than nothing, but they're not going to match that. On 40K, 1% is £400.1 -

Some misunderstanding.JamesNoBonds said:

I have already made that mistake with my own money. On a 3 year fixed saver. Though I was under the impression that the interest rate remains fixed even it it comes down overall in say year 2.Albermarle said:

That has been the usual norm, but currently you typically get a lower rate of interest for fixing for a few years.jacksonreed003 said:As your family member doesn't need regular access to the money then they could explore options like certificates of deposit (CDs) or longer-term saving accounts because they typically offer higher interests rates in exchange for locking in the funds for a set period of time. Or advice them to diversify their savings across multiple accounts to maximize their returns while still maintaining accessibility to their funds.

That is because it is expected that prevailing interest rates will slowly drop off in the coming couple of years.

If you have a fixed term account then the interest rate stays the same for the whole of the fixed term.

However interest rates in the market for easy access accounts, the Bank of England rate etc will change during the period of that fixed term.

So when the savings provider offers you that fix term rate ( for 3 years for example) they take a view on how interest rates in the market will develop over that 3 years. As the consensus is that interest rates will come down, then the rate you get offered for fixing for 3 years is currently actually less than you can earn in an easy access account. What you hope to gain by fixing for 3 years, is that after one or two years the interest rate will be better than you can get in an easy access account at that time.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards