We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Want to become a Forum Ambassador? Visit the Community Noticeboard for details on how to apply

Civil Service Classic Pension queries

Comments

-

All the statements will be sent out by 31st March 2025, which is before the handover to Capita takes place. Although as members with pensions in payment which may change based on their decision have 12 months to reply, Capita will be dealing with a decent number of member responses.m_c_s said:The next two years could be quite chaotic when all the Mcloud remedy calculations are sent to potentially 1 million current and ex public sector employees. Let's hope the handover to Capita right in the middle of when the statements are being sent out goes well!0 -

Interesting that now the preserved lump sum is x3 pension, as you would expect, and that the uprating lump sum from 1994 to the latest revaluation is in line with the revaluation Silvertabby wrote in the second post of this thread.kjs31 said:I finally have a response to some of the queries that I raised with the scheme administrator. They have uplifted my lump sum to something that looks a bit more reasonable but haven’t answered why the uplift to my lump sum is larger than that of my annual pension, and why the start date shows (correctly) as April on the website but as August in the app. They are supposed to be sending me a new statement, so baby steps and I’ll wait for that to arrive before asking any further questions. I’ve got until December to get it all sorted (might take that long at this rate 😆)

It still looks like the April 2024 revaluation has been applied to the revalued lump sum but not the revalued annual pension. If you apply it to the revalued annual pension, then the revalued lump sum is x3 the revalued annual pension, as you would expect.

Maybe once we get into April it will all start showing properly.2 -

hugheskevi said:Interesting that now the preserved lump sum is x3 pension, as you would expect, and that the uprating lump sum from 1994 to the latest revaluation is in line with the revaluation Silvertabby wrote in the second post of this thread.

It still looks like the April 2024 revaluation has been applied to the revalued lump sum but not the revalued annual pension. If you apply it to the revalued annual pension, then the revalued lump sum is x3 the revalued annual pension, as you would expect.

Maybe once we get into April it will all start showing properly.I think I’ll wait until April and then log in again and reassess. I’m rather hoping that the statement that is being produced will be dated April but knowing my luck it will be end of March. Just as well I started following it up with a year to go before the pension starts paying out …0 -

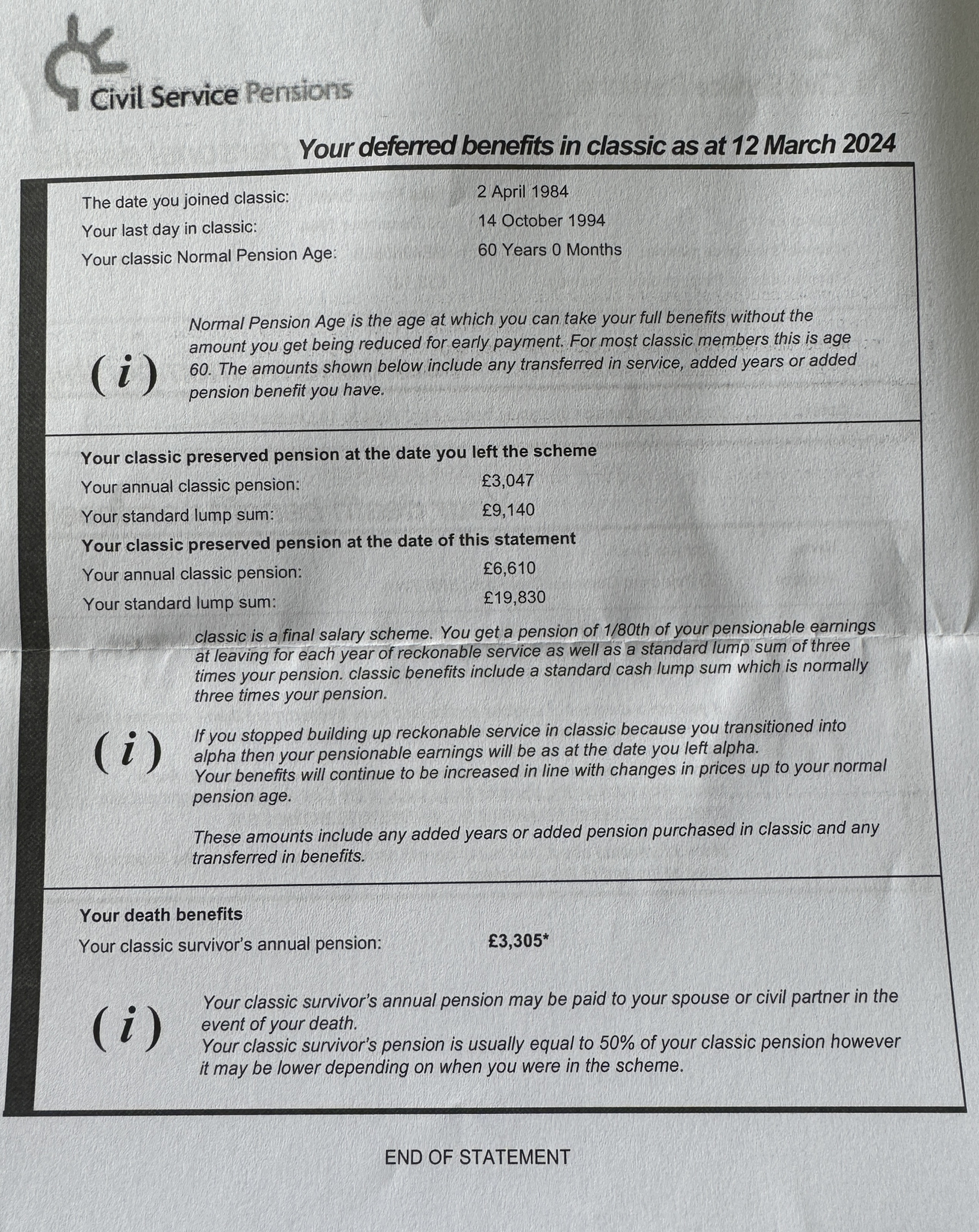

And just like that the pension statement has arrived in the post. The lump sum is different from what they have just corrected it to in their website (see screenshot above). How can I work out what it should be please? I have completely lost faith in their process! Also just checking that the lump sum is tax free.The website says that I should give 4 months notice of my intention to retire (before the date I hit 60 presumably). I actually thought they would contact me rather than the other way round. Given how slow they are should I be giving more notice than that? I don’t think I will benefit in any way if I defer my pension a little. For tax reasons it’s better if I don’t draw on it until tax year 25/26 but will take it regardless if I don’t stand to gain anything.If I’m late telling them I want to retire do they backdate it or do they just pay from the point that I tell them?

0

0 -

Yes, as the statement clearly stated, "A standard lump sum of three times your pension" Since your revalued pension is £6,610 on the paperwork, it makes perfect sense that it is a tax-free lump sum of £19,830.kjs31 said:And just like that the pension statement has arrived in the post. The lump sum is different from what they have just corrected it to in their website (see screenshot above). How can I work out what it should be please? I have completely lost faith in their process! Also just checking that the lump sum is tax free.

0 -

This statement actually looks correct, given it is as at 12th March 2024 and so does not contain an uplift for 2024 revaluation. The screenshot in the post above seemed to apply 2024 revaluation to the lump sum but not to the annual pension.kjs31 said:And just like that the pension statement has arrived in the post. The lump sum is different from what they have just corrected it to in their website (see screenshot above). How can I work out what it should be please? I have completely lost faith in their process! Also just checking that the lump sum is tax free.The website says that I should give 4 months notice of my intention to retire (before the date I hit 60 presumably). I actually thought they would contact me rather than the other way round. Given how slow they are should I be giving more notice than that? I don’t think I will benefit in any way if I defer my pension a little. For tax reasons it’s better if I don’t draw on it until tax year 25/26 but will take it regardless if I don’t stand to gain anything.If I’m late telling them I want to retire do they backdate it or do they just pay from the point that I tell them?

In just under a month the lump sum should return to the value in the screenshot, and annual pension increase to about £7,050 p/a, when April uprating is applied.

The lump sum is tax free.

There is no benefit in deferring a claim beyond age 60 except if moving the tax liability on pension paid from one year to a future year would be beneficial (eg if you will be moving from being a higher rate taxpayer to a lower rate taxpayer).

As you are a deferred member, if the pension payments are commenced after age 60 you will receive arrears back to age 60 (plus the tax-free lump sum and on-going pension).

3 -

I was more wanting to calculate whether the pension was actually correct. I know the lump sum should be 3 x pension. The letter I received says “check the information AGAINST your own records to make sure it’s correct”. I had expected the calculations to be correct, not to have to check them, but given that the website has been updated incorrectly twice now I find myself having to ensure that the figures are correct.JoeCrystal said:Yes, as the statement clearly stated, "A standard lump sum of three times your pension" Since your revalued pension is £6,610 on the paperwork, it makes perfect sense that it is a tax-free lump sum of £19,830.0 -

Thanks. I would prefer to delay drawing the pension until 25/26 as I’m trying to mitigate hitting the personal allowance taper in the next tax year. Although it’s not a huge amount I would rather keep under 100k next year if I can. If I can start the pension in April 2025 and get the arrears paid then too that will be perfect. I expect to be a basic rate tax payer in 25/26 so there are other tax advantages too.hugheskevi said:

There is no benefit in deferring a claim beyond age 60 except if moving the tax liability on pension paid from one year to a future year would be beneficial (eg if you will be moving from being a higher rate taxpayer to a lower rate taxpayer).

As you are a deferred member, if the pension payments are commenced after age 60 you will receive arrears back to age 60 (plus the tax-free lump sum and on-going pension).0 -

Ah, I see what you mean now. My apologies for misunderstanding you. You can always work out your expected pension based on the relevant index linking, as you already have the preserved pension from when you initially left.kjs31 said:

I was more wanting to calculate whether the pension was actually correct. I know the lump sum should be 3 x pension. The letter I received says “check the information AGAINST your own records to make sure it’s correct”. I had expected the calculations to be correct, not to have to check them, but given that the website has been updated incorrectly twice now I find myself having to ensure that the figures are correct.JoeCrystal said:Yes, as the statement clearly stated, "A standard lump sum of three times your pension" Since your revalued pension is £6,610 on the paperwork, it makes perfect sense that it is a tax-free lump sum of £19,830.1 -

I am currently in the process of retiring, last day is the end of April. I still haven't received my figures which according to MyCSP should be with me 8 weeks before I retire - I am supposed to check and sign them and then send them back and if I do that with a month to go I should get my pension from May. However, as I haven't received the figures I contacted them to be told they won't be produced until the end of this month - when I queried how I am supposed to get it back to them with a month to go when I won't actually receive it before that date has gone past I was told all dates are 'fluid'.

I wouldn't mind so much but I put in my application with 6 months to go, so good luck with your application!Mortgage free!

Debt free!

And now I am retired - all the time in the world!!2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.9K Work, Benefits & Business

- 603.5K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards