We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

USS drawdown options in early retirement

Comments

-

It still doesn't explain the bit of the statement that "you can usually take all of your Investment Builder pot as tax-free cash (depending on the size of your pot)" but hey, let's leave it to another day of learning !

That statement is assuming/covering members who haven't built up large Investment Builder pots. Many won't be making significant additional contributions, or they will be simply building it up from contributions above the threshold. People like many of us on here who are stuffing the IB for all it's worth, build up more than the maximum that can be taken tax free (determined using the calculation being discussed).

1 -

Thank you @MPLMPL - actually I have just editted that part in my response - to say yes if the pot is quite small then you CAN take it all out tax free (see the EDIT part pasted again below). I have already reached quite a bit of that level in my DC pot whilst still have about 25 years to work if to full state pension age, and there are reasons why I have to :-) volunteer contribute. So that size is quite small even in my case of very average salary not reaching the reinstated threshold (though to be fair I have put in more substantially recently because I am having some benefits, which will stop after kids go to uni). For now I will still keep adding volunteerily only what I must, because I anticipate some big sums of cash needed for other investments much before I retire.MPLMPL said:It still doesn't explain the bit of the statement that "you can usually take all of your Investment Builder pot as tax-free cash (depending on the size of your pot)" but hey, let's leave it to another day of learning !That statement is assuming/covering members who haven't built up large Investment Builder pots. Many won't be making significant additional contributions, or they will be simply building it up from contributions above the threshold. People like many of us on here who are stuffing the IB for all it's worth, build up more than the maximum that can be taken tax free (determined using the calculation being discussed).

EDIT: So if I insist to work out an ideal IB pot that can I can take all out tax free then based on the new understaning you give it is:(23*DB)/4 – 3*DB=DC

5.75*DB-3*DB=DC

2.75*DB=DC

That means to get all of the DC pot out tax-free, the size can only be 2.75 times the DB, in this case 2.75*20K=55K. Then the divided by 0.75 bit to make 73.33 K(I still need to settle my mind with this bit). - NOT 153K in my old wrong understanding of total pot.

and of course the DB*3 = 60K too (i also wrongly thought taking this will reduce the 20K/year DB income- annual income only reduces when one takes 25% tax free from the DB)

0 -

-

No worries. I have been there myself. It took me a looong time (much longer than you) to understand it in the first place.LL_USS said:") 1

1 -

Your next step is 2.75/0.75 = 3.6667LL_USS said:EDIT: So if I insist to work out an ideal IB pot that can I can take all out tax free then based on the new understaning you give it is:(23*DB)/4 – 3*DB=DC

5.75*DB-3*DB=DC

2.75*DB=DC

As others have said on here, for every £1 of DB you can take out an extra £3.6667 tax free from the IB.

So with a DB of £20k, the sum would be £20k x 3.6667 = £73,333

If you add in the 3 x DB lump sum, then the total tax-free lump sum will be DB x 6.6667.

Or £20k x 6.6667 = £133,3331 -

Thank you @gwt1965gwt1965 said:

Your next step is 2.75/0.75 = 3.6667LL_USS said:EDIT: So if I insist to work out an ideal IB pot that can I can take all out tax free then based on the new understaning you give it is:(23*DB)/4 – 3*DB=DC

5.75*DB-3*DB=DC

2.75*DB=DC

As others have said on here, for every £1 of DB you can take out an extra £3.6667 tax free from the IB.

So with a DB of £20k, the sum would be £20k x 3.6667 = £73,333

If you add in the 3 x DB lump sum, then the total tax-free lump sum will be DB x 6.6667.

Or £20k x 6.6667 = £133,333

I did write under that bit above about dividing it by 0.75 making 55k/0.75=73.33K as @NickBFS said (noting I accept that division but will have to settle my mind again on why exactly- and now with the extra bit of explanation I am getting there ;-).

0 -

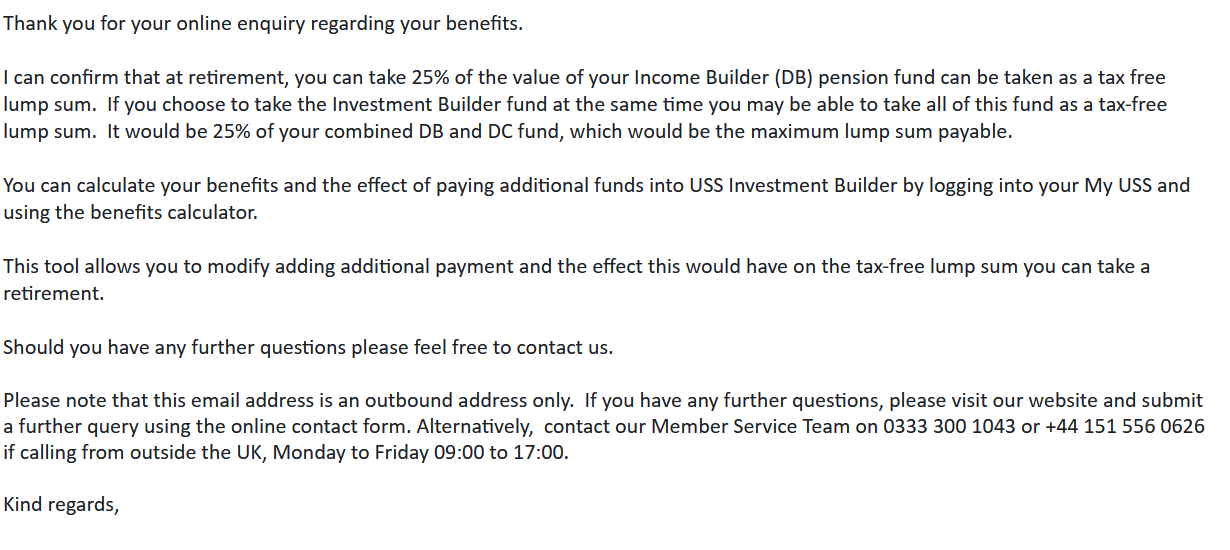

LL_USS said:NickBFS said:It does not work like that. the maximum PCLS that you can take when you start your DB is 25% of the value of your DB. The value of your DB itself is 20xDB, to which we need to add the default lump sum of 3xDB. So, the maximum PCLS is (23xDB)/4. This is so, regardless of the size of your DC pot.I understand now. The USS website says "25% of the overall benefits at retirement" - that is the "benefits" the employer promises you for the rest of your life, hence, based on the DB (20*DB/year + 3 times of DB lumpsum), independent of your DC - I see I see I see....Oh no I have emailed USS and this is what they have just told me. It means the TFLS is calculated as 25% of the combined DB and DC fund. Can we trust USS helpline??????????????????????

EDIT - Please ignore this. I have got the answers from others after this post. Thanks !!!!!!!!!!!

0 -

Their statement does not refute the information you've been given re calculating the maximum TFLS.LL_USS said:LL_USS said:NickBFS said:It does not work like that. the maximum PCLS that you can take when you start your DB is 25% of the value of your DB. The value of your DB itself is 20xDB, to which we need to add the default lump sum of 3xDB. So, the maximum PCLS is (23xDB)/4. This is so, regardless of the size of your DC pot.I understand now. The USS website says "25% of the overall benefits at retirement" - that is the "benefits" the employer promises you for the rest of your life, hence, based on the DB (20*DB/year + 3 times of DB lumpsum), independent of your DC - I see I see I see....Oh no I have emailed USS and this is what they have just told me. It means the TFLS is calculated as 25% of the combined DB and DC fund. Can we trust USS helpline??????????????????????

"25% of your total DB and DC fund" is a high level statement. To test this, try to work out the total TFLS with this information alone (you can't).

The formula provided by MPLMPL is correct.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards