We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Nursing home assessment fee

Comments

-

Show me where in the CCA the word beneficiary or any synonym of it is used?SiliconChip said:I doubt if a S75 claim would be successful as you are not the beneficiary of the credit.

For S75 to apply there must be a three way relationship between the debtor, the creditor and the supplier with no additional parties (other than merchant acquiring bank) involved. The OP doesn't need to be the beneficiary of the service (they are the beneficiary of the credit) but does clearly need to be the contracting party with the supplier.

Agree on the other point though, a chargeback is more likely to be quicker and simpler assuming there is no significant delay that time bars it.0 -

The whole "beneficiary" angle is an urban myth that emerged on these forums, because people mis-read a poorly written MSE page referring to a FOS decision. That page has since been re-written.

As you say, "Beneficiary" doesn't appear in the legislation - but it does appear in FOS rulings on s75 with "additional credit card holders". (So this isn't relevant to this thread.)

In simple terms, the FOS has decided that...- In general, purchases made by additional card holders aren't covered by s75 (no 'Debtor-Creditor-Supplier chain) ...

- ... unless the additional card holder's purchase is for the benefit of the main card holder. (In that case, the FOS says a Debtor-Creditor-Supplier chain exists.)

FWIW, here's an example FOS ruling:Looking first at whether section 75 applies, it’s correct that the link between debtor, creditor and supplier mustn’t be broken. The problem here is whether this is broken because the toy car was paid for on Mr S’s card rather than on Mrs S’s card, as she was the main cardholder. I accepted that the link is satisfied if the purchase made on Mr S’s card also benefited Mrs S. I find that it did, because it was a present for their son, which they told us they sat together on the sofa and chose on the laptop, and wrapped up with a label from them both. So I found it was a combined purchase and a joint decision, chosen together and given to him together. So I found that the debtor, creditor and supplier requirement of section 75 was satisfied.

Link: https://www.financial-ombudsman.org.uk/decision/DRN4115539.pdf

1 -

Without wanting to go too far down the rabbit hole which isn't relevant to this thread but do you have any other cases @eddddy ?eddddy said:In simple terms, the FOS has decided that...- In general, purchases made by additional card holders aren't covered by s75 (no 'Debtor-Creditor-Supplier chain) ...

- ... unless the additional card holder's purchase is for the benefit of the main card holder. (In that case, the FOS says a Debtor-Creditor-Supplier chain exists.)

The one thing notable thing to me in the background if I were looking over the case is the statement that they were together when they choose and bought it and it was given as a gift from the pair of them. So it is likely it was effectively a joint contract and just for some practical reason the additional cardholders card was used (if its like with my wife it'll be as my phone is in my pocket and I can get it out, activate ApplePay and tap before my wife has worked out if her phone is in her handbag or a pocket)

I appreciate the Ombudsman uses the language of beneficiary but if you look hard enough there are more than one outlier decisions in the database and hence wonder if this is a common thinking or a one off from an ombudsman having a weird moment.0 -

DullGreyGuy said:

Without wanting to go too far down the rabbit hole which isn't relevant to this thread but do you have any other cases @eddddy ?

Yep.

(But I suspect that a lot of people have lost interest by now...)

Here are some snippets from FOS decisions, but the lack of "benefit to the main cardholder" argument is generally used as a reason to reject the claims....To succeed a S 75 claim has to meet certain criteria. One of the key criteria is that there is a debtor-creditor-supplier link. Purchases made by an additional cardholder do not meet this requirement unless the goods or services are purchased for the benefit of the main cardholder.

https://www.financial-ombudsman.org.uk/decision/DRN1686735.pdfBut purchases made by an additional cardholder don’t maintain the supplier - debtor part of the chain unless the goods or services are bought for the benefit of the main cardholder.

Link: https://www.financial-ombudsman.org.uk/decision/DRN5928621.pdfAlthough I don’t doubt that Mr P has had some involvement in the process of helping with the car purchase, and while he might get some benefit from the car, I’m not satisfied that this is enough to make him a contracting party for the requirements of a Section 75 claim.

Link: https://www.financial-ombudsman.org.uk/decision/DRN-2376015.pdf

Tesco Personal Finance also appear to agree...Tesco also said that the invoices for the work were in his partner’s name. So Mr S would need to show that he jointly benefited from the car

Link: https://www.financial-ombudsman.org.uk/decision/DRN1031482.pdf

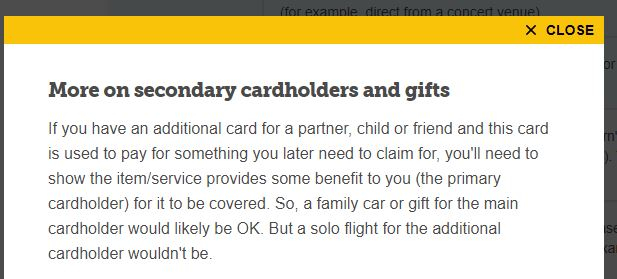

And the offending MSE webpage has now been rewritten more clearly to say:

Link: https://www.moneysavingexpert.com/reclaim/section75-protect-your-purchases/

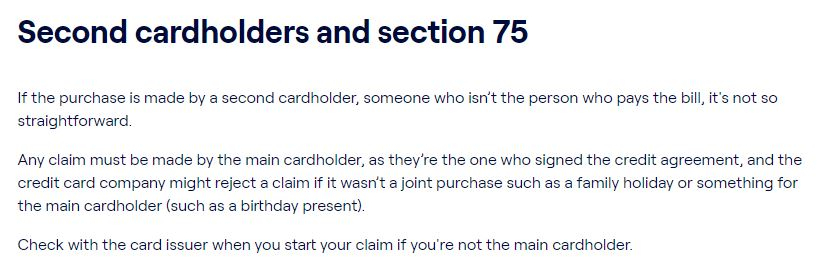

And the government-backed Money Helper website seems to be saying the same thing....

Link: https://www.moneyhelper.org.uk/en/everyday-money/credit/how-youre-protected-when-you-pay-by-card

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards