We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Considering a pension move due to charges

Comments

-

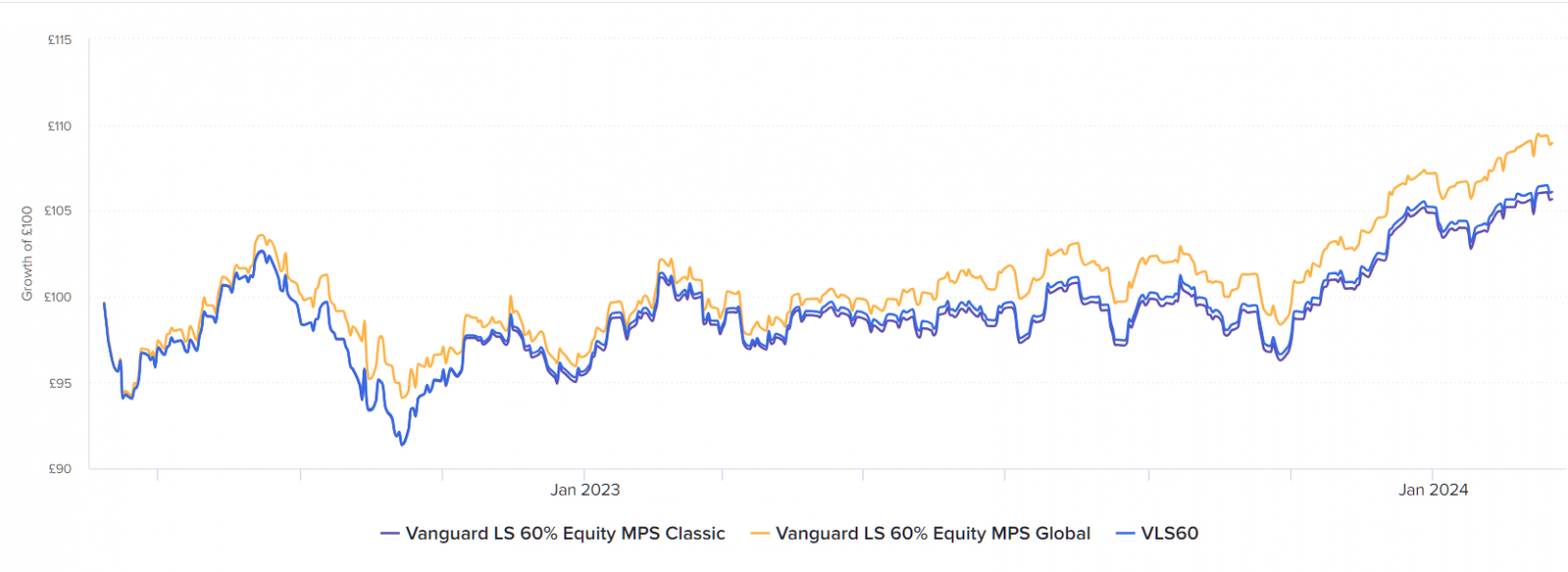

Here is the performance of the VLS60 vs Tatton core active.

If the OP had decided to switch to VLS60 and get lower charges in the past, they would have a lower fund value. There isn't a lot in it until Vanguard's fund management decisions on VLS hurt its performance from late 2021 onwards.

We don't know what the future holds. However, if the OP had made the decision back in 2012 and was investing £100,000 back then and was comparing the two now, would they be happier to have got £211,610 from VLS60 and having paid lower charges or £231,220 from Tatton but having paid higher charges. At the moment, the op is focusing on lower costs but in that period, it would have produced a worse outcome.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

VLS60 is a frequently used comparator on here. I don’t believe JohnWinder intended it as a recommendation, just as an example of a passive fund that doesn’t use tactical allocation.engagedandopen said:Do you work for Vanguard, JohnWinder?1 -

Thanks for the growth chart. You can't invest in Tatton without an advisor, and Tatton charges DFM fees as well as OCF of the fund. So any comparison of Tatton and VLS returns needs to include those, not just the fund fee as I imagine the chart does. Is it so?

Secondly, there's not much difference between 60% equity with VLS60, and 75% equity with Tatton active core, but fair go when making such comparisons. Of course we'd expect more equities to give better returns over longer periods.

I compared VLS60 with Tatton balanced because I couldn't find on their website the composition of the active core fund. I'm dull, accepted, or their website isn't as clear as Vanguard's, but then it doesn't have to be when you're paying two sets of fees for someone else to know what's in the fund.

Thirdly, one example of a fund outperforming another should not be a temptation to put it ahead of all the research suggesting Tatton-type funds with more than a sniff of active management and higher fees are less likely to be the better long term choice. Back to the SPIVA reports.

1 -

Thanks for the growth chart. You can't invest in Tatton without an advisor, and Tatton charges DFM fees as well as OCF of the fund. So any comparison of Tatton and VLS returns needs to include those, not just the fund fee as I imagine the chart does. Is it so?DFM fees are included in the chart. Hubwise is the same charge as Vanguard. So, the only difference missing is the adviser charge.Secondly, there's not much difference between 60% equity with VLS60, and 75% equity with Tatton active core, but fair go when making such comparisons. Of course we'd expect more equities to give better returns over longer periods.I also compared it against a 70% and 60% alternative DFM that uses underlying passives with an OCF and DFM charge that is less than the OCF of VLS (0.18% vs 0.22%) and the alternative had returned significantly higher than VLS and Tatton.I compared VLS60 with Tatton balanced because I couldn't find on their website the composition of the active core fund. I'm dull, accepted, or their website isn't as clear as Vanguard's, but then it doesn't have to be when you're paying two sets of fees for someone else to know what's in the fund.

DFMs come in different forms.

Full DFM (waste of money IMO - aimed at those that like to brag they speak to their investment manager who makes all the changes on the fly)

DFM using fund structure - a viable option. AJ Bell operates one like this which all funds under the OCF. It's 0.29% (IIRC) but it has outperformed VLS. VLS funds are a DFM using the fund structure. As are pretty much much most fund of funds.

DFM using MPS - this uses the actual underlying funds, often the institutional share classes rather than retail but uses platform software to set the weightings. This is my preference.

Vanguard have three versions of Lifestrategy.

Vanguard LifeStrategy Funds (uses fund structure - the one usually referred to on this site)

Vanguard LifeStrategy MPS Classic (uses MPS structure)

Vanguard LifeStrategy MPS Global (uses MPS structure)

All are 0.22%. That makes sense as VLS fund OCF is inclusive of the DFM charge whereas MPS has a lower OCF but with DFM shown explicitly.

VLS fund has home bias and is rebalanced daily

VLS MPS classic has home bias and rebalanced quarterly

VLS MPS global removes home bias and rebalanced quarterly

In time, I would expect the MPS classic to outperform the fund version as quarterly rebalancing should allow greater drift than daily rebalancing. As the MPS hasn't been running long and that period has been mostly flat, we cannot see that yet but quarterly rebalancing is better than daily rebalancing in most periods (although I believe VLS fund uses inflows and outflows in its rebalancing)

In that short period, if you had an IFA that recommended VLS 60% MPS global and that IFA charged 0.50% p.a. (the most dominant of the IFA charges), then the return on the MPS would have covered it and still been better than the VLS60 fund. Nothing to do with the IFA but the removal of home bias. Except a consumer cannot access VLS60 MPS Global directly.

As an IFA, I wouldn't use the fund version of VLS60. I would use the MPS version and I am not a fan of home bias, so I would pick the global. However, I don't use the VLS range (in any form) as Vanguard doesn't use the institutional share classes but the retail share classes. I have access to the institutional share classes of Vanguard, Blackrock, HSBC, L&G etc which lowers the DFM and OCF total to 0.18%. The performance is virtually identical but that is logical given the asset mix and weightings but on a £100k investment from launch of the VLS MPS, the 60% equity versions have turned that into £106,100 on VLS60, £108,900 on VLS 60 MPS, and £109,200 on the one we use. IFA charge would be approx £750 over that period. So, take off £750 from both VLS MPS and the one I use and both are higher than the VLS fund version which has no adviser charge. I would happily use the VLS global MPS if it were not for that (plus, the one we use does 10% equity segments rather than 20% and doesn't rebalance until there is a 10% drift, which should help improve longer-term returns).

None of this is down to the IFA other than facilitating and being aware of what is available and how to access it cost-effectively.Thirdly, one example of a fund outperforming another should not be a temptation to put it ahead of all the research suggesting Tatton-type funds with more than a sniff of active management and higher fees are less likely to be the better long term choice. Back to the SPIVA reports.Hybrid investing (mix of active and passive) is popular and Vanguard believes Hybrid to be a viable option. in the case of the Tatton MPS, most of it is passive. They also use passives to alter focus (e.g. they split the UK allocation so its not pure all share) but 25% of the portfolio is active.

SPIVA is not a bible to be followed religiously. Small amounts of active can make sense when it is used to adjust weightings or focus in small areas rather than chase fund managers that have got lucky for a period.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

ii are offering up to £5,000 cashback on SIPP transfers (£2000 on a £525k transfer) and platform fees would be just £156pa for funds:

http://www.ii.co.uk/acq/open-sipp-account

Scrounger

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards