We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Tempted by an annuity - comments please

Comments

-

MK62 said:Well, strictly speaking, risk is the combination of the probability of something happening and the consequences of it, but I'm not going to argue this......whether it's a risk or a consequence, loss of legacy is a consideration, and for many, a major one.You're confusing risk and risk management. Risk is the possibilty of something bad happening. If something is certain, that's not a risk, it's a known outcome.Of course it's a consideration. If you want to leave a legacy, you don't spend that money, whether on an annuity or a world cruise.0

-

zagfles said:MK62 said:Well, strictly speaking, risk is the combination of the probability of something happening and the consequences of it, but I'm not going to argue this......whether it's a risk or a consequence, loss of legacy is a consideration, and for many, a major one.You're confusing risk and risk management. Risk is the possibilty of something bad happening. If something is certain, that's not a risk, it's a known outcome.You're confusing probability (possibility) and risk.Risk is more than just the possibility of something bad happening........the consequence of that something is equally a factor. A low possibility of something bad happening does not necessarily mean that whatever you are doing is then low risk......(how bad is bad?).....and two "somethings" of equal possibility, doesn't necessarily mean the risk itself is then the same.0

-

MK62 said:zagfles said:MK62 said:Well, strictly speaking, risk is the combination of the probability of something happening and the consequences of it, but I'm not going to argue this......whether it's a risk or a consequence, loss of legacy is a consideration, and for many, a major one.You're confusing risk and risk management. Risk is the possibilty of something bad happening. If something is certain, that's not a risk, it's a known outcome.You're confusing probability (possibility) and risk.Risk is more than just the possibility of something bad happening........the consequence of that something is equally a factor. A low possibility of something bad happening does not necessarily mean that whatever you are doing is then low risk......(how bad is bad?).....and two "somethings" of equal possibility, doesn't necessarily mean the risk itself is then the same.You're confusing arguing and not arguing "I'm not going to argue this"

But you're not even arguing the real point. Something that is certain is not a risk. That's where all this started. Are you now not going to argue that a certainty is a risk

But you're not even arguing the real point. Something that is certain is not a risk. That's where all this started. Are you now not going to argue that a certainty is a risk") But back to the irrelavent side discussion off the main point.In common usage, risk is only possibility of something bad happening, not consequences, which is usually defined later.Putting £1 on number 17 on a roulette table is high risk of losing £1Taking a flight is low risk of dying in a plane crash.The level of the risk is the chance, the consequences are separately stated.In technical areas like insurance and risk management, they'll obviously include consequences in risk management analysis.In normal discussion the risk is the probability and the consequences are separately stated.

But back to the irrelavent side discussion off the main point.In common usage, risk is only possibility of something bad happening, not consequences, which is usually defined later.Putting £1 on number 17 on a roulette table is high risk of losing £1Taking a flight is low risk of dying in a plane crash.The level of the risk is the chance, the consequences are separately stated.In technical areas like insurance and risk management, they'll obviously include consequences in risk management analysis.In normal discussion the risk is the probability and the consequences are separately stated.

0 -

Nope.......putting £1 on number 17 on a roulette table has a high probability of losing £1.Putting £100,000 on number 17 has exactly the same probability of losing as putting £1 on, but few people would equate the risk as being the same, as the impact/consequence of losing are not the same.Taking a flight is low risk of dying in a plane crash.........Well, yes and no - there is a high probability of dying in a plane crash, but a very very low probability that you'll be in one. It's the low probability that makes the risk acceptable, for most anyway......some won't fly at all though, as for them the consequence outweighs the probability. This is why "risk" never comes down to just possibility or probability....the consequence/impact (call it what you will) has to considered as well.Consider two revolvers, one has a single bullet in it, the other has a single paintball.........you might allow the revolver with the paintball in it to be fired at you.......but I'd wager that you wouldn't allow someone holding the revolver with the bullet in it to do the same.......the probabilities are the same in each case, but the consequences are not........hence the risk is different.1

-

As others have said, the cap on the DB pension does make planning a bit less certain (I'm in the same position).Mutton_Geoff said:I'm fortunate to have just retired at 65 with a DB pension, SP about to be paid next month and a crystallised SIPP worth £1m. I've extracted all my TFC and leveraged that on property developments meaning I now live in a house with no mortgage.

My SIPP is self invested with medium to high risk tolerance since I have the stability of index linked DB (RPI capped 5%) and SP pensions as a backdrop. My intention was to drawdown the SIPP at a higher rate in the early years and slow down later in life and then exhaust the pot by a 1/n drawdown where n is 20 years 65-85 years old.

The DB & SP take me into the higher rate tax bracket so all SIPP drawdown is taxed at 40% or higher. My plan next year onwards is to cap regular income at £100k to avoid loss of personal tax code (ie 60%) then 45% tax.

As I'm eligible for an enhanced annuity, I have a range of quotes and am tempted by the level rate offer since this will fit my plan of higher income in the early years rather than everything escalating into the twilight of my life. Inflation can then deplete it's value for me.

Although I'm happy watching my SIPP, I am very tempted to derisk 60% of my SIPP investment by buying an annuity. Since tax rates are not scheduled to change until at least 2028, working forward inflation on my DB & SP, I could buy an level annuity at 7.5% paying £44k which means a gross guaranteed income of £90k now, £100k in 2028 and leaving £400k in my SIPP to be used as and when albeit with a high rate of income tax on any drawdown.

The question is whether to buy that annuity and lock in 7.5% and guaranteed income up to the loss of tax code/additional rate bands. The only downside I can see is massive growth in the SIPP (which would then lose almost 50% to tax in any case). I don't have any need to leave a legacy.

Plan A £100k income - keep SIPP & assume 5% inflation

DB £35k (2028 = £42k)

SP £11k (2028 = £14k)

SIPP £54k (5.4%) (2028 = £44k - unknown %)

Plan B £100k income - via £600k annuity

DB £35k (2028 = £42k)

SP £11k (2028 = £14k)

ANNUITY £44k (2028 = £44k)

SIPP £10k (2.5% drawdown) (2028 = £0k - unknown SIPP value)

I'm sorely tempted by buying some stability since any downside on a SIPP cost me money, the upside is skewed (ie taxed) by around 50%.

By comparison, the annuity quote offered 4.8% RPI linked but for reasons above, tempted by high ("jam today") level rate.

I really appreciate thoughts from the experts here.

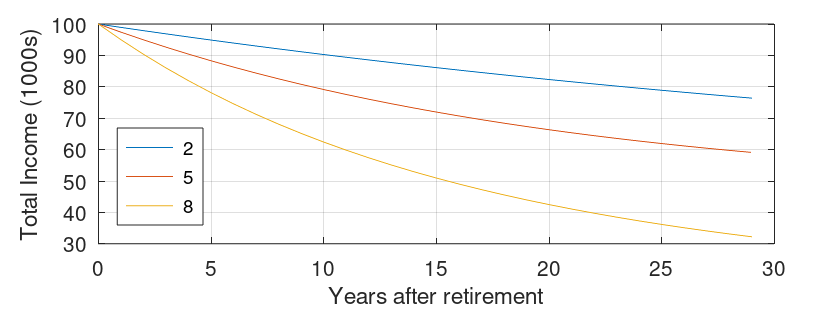

Assuming £720k spent on a level annuity (to take the initial income to £100k) and three different values for inflation (2, 5, and 8% - of course inflation is not smooth), the total income in real terms (i.e., in today's money) from the guaranteed income parts of your plan (i.e., SP, DB pension, and annuity) might look something like

For 2% and 5% only the income from the level annuity is affected by inflation, while at 8% the DB pension income also declines with time. The £280k remaining in the SIPP could be used to offset the decline in guaranteed income. The 30 year 'safe' withdrawal rate (i.e, assuming constant inflation adjusted income) is something of the order of 3.0 to 3.5%, so might give an additional 8-10k per year in real terms which would offset the declines for 10, 4, and 2 years depending on the inflation. Accepting a planned decline in portfolio income, in real terms, of 3% gives an initial withdrawal rate of 4.5% (i.e., about £12.6k). In any case, depending on inflation, income from the portfolio might not be needed early on.

If an RPI annuity is bought with the £720k instead, then the real total income from the SP, DB, and annuity components looks something like

For inflation of 2% and 5%, the income is a constant £80k, while for 8% inflation there is a decline in the DB income. The shortfall is about 20k, i.e., about 7% of the remaining portfolio. In the worst historical case this was just about sustainable for a 10 year period.If a 3% decline (in real terms) is acceptable, then it was sustainable for about 12 years (i.e., not a lot longer).

Of course, using the 1/n approach you've suggested, means that the income from the portfolio will, in real terms, be variable from year to year.

Which of these looks like a preferred outcome is a rather personal preference.

4 -

MK62 said:Nope.......putting £1 on number 17 on a roulette table has a high probability of losing £1.Putting £100,000 on number 17 has exactly the same probability of losing as putting £1 on, but few people would equate the risk as being the same, as the impact/consequence of losing are not the same.And putting your £1 on black, rather than 1, has a much lower probability of losing but the same consequence if you do. So it's lower risk.I hop that helps with the discussion, but it might not

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 37 MWh generated, long-term average 2.6 Os.0 -

QrizB said:MK62 said:Nope.......putting £1 on number 17 on a roulette table has a high probability of losing £1.Putting £100,000 on number 17 has exactly the same probability of losing as putting £1 on, but few people would equate the risk as being the same, as the impact/consequence of losing are not the same.And putting your £1 on black, rather than 1, has a much lower probability of losing but the same consequence if you do. So it's lower risk.I hop that helps with the discussion, but it might not ...haha

1 -

QrizB said:MK62 said:Nope.......putting £1 on number 17 on a roulette table has a high probability of losing £1.Putting £100,000 on number 17 has exactly the same probability of losing as putting £1 on, but few people would equate the risk as being the same, as the impact/consequence of losing are not the same.And putting your £1 on black, rather than 1, has a much lower probability of losing but the same consequence if you do. So it's lower risk.I hop that helps with the discussion, but it might notAnd if you spend the £1 on a coffee then you risk not having that £1 to leave as a legacy. Apparently

0 -

OldScientist said:

As others have said, the cap on the DB pension does make planning a bit less certain (I'm in the same position).Mutton_Geoff said:I'm fortunate to have just retired at 65 with a DB pension, SP about to be paid next month and a crystallised SIPP worth £1m. I've extracted all my TFC and leveraged that on property developments meaning I now live in a house with no mortgage.

My SIPP is self invested with medium to high risk tolerance since I have the stability of index linked DB (RPI capped 5%) and SP pensions as a backdrop. My intention was to drawdown the SIPP at a higher rate in the early years and slow down later in life and then exhaust the pot by a 1/n drawdown where n is 20 years 65-85 years old.

The DB & SP take me into the higher rate tax bracket so all SIPP drawdown is taxed at 40% or higher. My plan next year onwards is to cap regular income at £100k to avoid loss of personal tax code (ie 60%) then 45% tax.

As I'm eligible for an enhanced annuity, I have a range of quotes and am tempted by the level rate offer since this will fit my plan of higher income in the early years rather than everything escalating into the twilight of my life. Inflation can then deplete it's value for me.

Although I'm happy watching my SIPP, I am very tempted to derisk 60% of my SIPP investment by buying an annuity. Since tax rates are not scheduled to change until at least 2028, working forward inflation on my DB & SP, I could buy an level annuity at 7.5% paying £44k which means a gross guaranteed income of £90k now, £100k in 2028 and leaving £400k in my SIPP to be used as and when albeit with a high rate of income tax on any drawdown.

The question is whether to buy that annuity and lock in 7.5% and guaranteed income up to the loss of tax code/additional rate bands. The only downside I can see is massive growth in the SIPP (which would then lose almost 50% to tax in any case). I don't have any need to leave a legacy.

Plan A £100k income - keep SIPP & assume 5% inflation

DB £35k (2028 = £42k)

SP £11k (2028 = £14k)

SIPP £54k (5.4%) (2028 = £44k - unknown %)

Plan B £100k income - via £600k annuity

DB £35k (2028 = £42k)

SP £11k (2028 = £14k)

ANNUITY £44k (2028 = £44k)

SIPP £10k (2.5% drawdown) (2028 = £0k - unknown SIPP value)

I'm sorely tempted by buying some stability since any downside on a SIPP cost me money, the upside is skewed (ie taxed) by around 50%.

By comparison, the annuity quote offered 4.8% RPI linked but for reasons above, tempted by high ("jam today") level rate.

I really appreciate thoughts from the experts here.

Assuming £720k spent on a level annuity (to take the initial income to £100k) and three different values for inflation (2, 5, and 8% - of course inflation is not smooth), the total income in real terms (i.e., in today's money) from the guaranteed income parts of your plan (i.e., SP, DB pension, and annuity) might look something like

For 2% and 5% only the income from the level annuity is affected by inflation, while at 8% the DB pension income also declines with time. The £280k remaining in the SIPP could be used to offset the decline in guaranteed income. The 30 year 'safe' withdrawal rate (i.e, assuming constant inflation adjusted income) is something of the order of 3.0 to 3.5%, so might give an additional 8-10k per year in real terms which would offset the declines for 10, 4, and 2 years depending on the inflation. Accepting a planned decline in portfolio income, in real terms, of 3% gives an initial withdrawal rate of 4.5% (i.e., about £12.6k). In any case, depending on inflation, income from the portfolio might not be needed early on.

If an RPI annuity is bought with the £720k instead, then the real total income from the SP, DB, and annuity components looks something like

For inflation of 2% and 5%, the income is a constant £80k, while for 8% inflation there is a decline in the DB income. The shortfall is about 20k, i.e., about 7% of the remaining portfolio. In the worst historical case this was just about sustainable for a 10 year period.If a 3% decline (in real terms) is acceptable, then it was sustainable for about 12 years (i.e., not a lot longer).

Of course, using the 1/n approach you've suggested, means that the income from the portfolio will, in real terms, be variable from year to year.

Which of these looks like a preferred outcome is a rather personal preference.Good analysis, although another thing to account for is sequence of inflation risk. Just like SORR with an equity based drawdown, with a fixed/capped income stream like DB pension or level annuities, high inflation towards the start of retirement will have a far bigger impact than high inflation towards the end. So modelling assuming a constant inflation rate, whatever that rate is, could be misleading. If inflation is 10% for the first 3 years of retirement then that's a permanent 25% reduction in the value of a level annuity, or a 13% reduction in a 5% capped DB

1 -

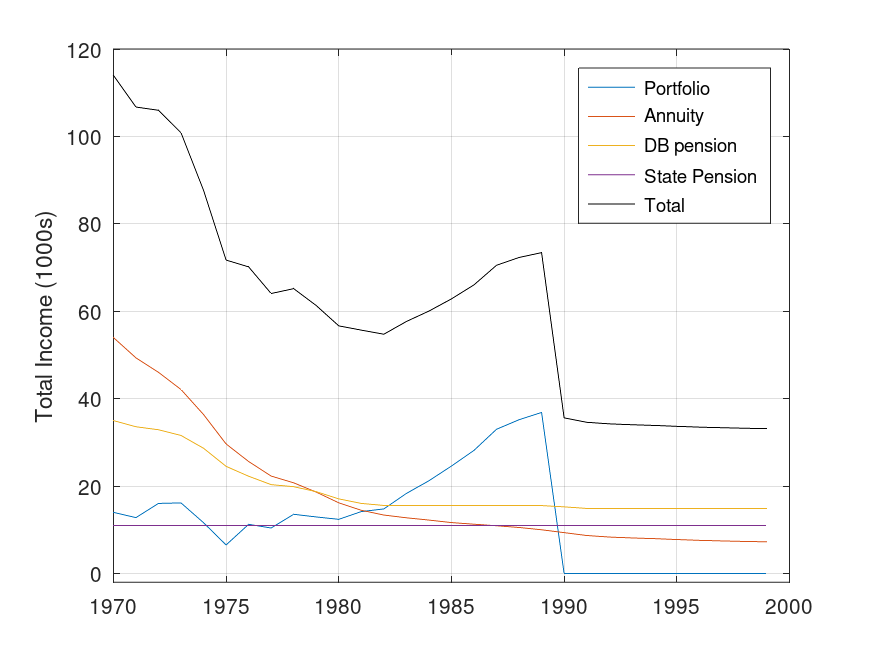

You are correct - sequence of inflation is important. So, let's have a look at an example where we use the inflation (and asset returns) for 30 years starting in 1970.zagfles said:OldScientist said:Mutton_Geoff said:I'm fortunate to have just retired at 65 with a DB pension, SP about to be paid next month and a crystallised SIPP worth £1m. I've extracted all my TFC and leveraged that on property developments meaning I now live in a house with no mortgage.

My SIPP is self invested with medium to high risk tolerance since I have the stability of index linked DB (RPI capped 5%) and SP pensions as a backdrop. My intention was to drawdown the SIPP at a higher rate in the early years and slow down later in life and then exhaust the pot by a 1/n drawdown where n is 20 years 65-85 years old.

The DB & SP take me into the higher rate tax bracket so all SIPP drawdown is taxed at 40% or higher. My plan next year onwards is to cap regular income at £100k to avoid loss of personal tax code (ie 60%) then 45% tax.

As I'm eligible for an enhanced annuity, I have a range of quotes and am tempted by the level rate offer since this will fit my plan of higher income in the early years rather than everything escalating into the twilight of my life. Inflation can then deplete it's value for me.

Although I'm happy watching my SIPP, I am very tempted to derisk 60% of my SIPP investment by buying an annuity. Since tax rates are not scheduled to change until at least 2028, working forward inflation on my DB & SP, I could buy an level annuity at 7.5% paying £44k which means a gross guaranteed income of £90k now, £100k in 2028 and leaving £400k in my SIPP to be used as and when albeit with a high rate of income tax on any drawdown.

The question is whether to buy that annuity and lock in 7.5% and guaranteed income up to the loss of tax code/additional rate bands. The only downside I can see is massive growth in the SIPP (which would then lose almost 50% to tax in any case). I don't have any need to leave a legacy.

Plan A £100k income - keep SIPP & assume 5% inflation

DB £35k (2028 = £42k)

SP £11k (2028 = £14k)

SIPP £54k (5.4%) (2028 = £44k - unknown %)

Plan B £100k income - via £600k annuity

DB £35k (2028 = £42k)

SP £11k (2028 = £14k)

ANNUITY £44k (2028 = £44k)

SIPP £10k (2.5% drawdown) (2028 = £0k - unknown SIPP value)

I'm sorely tempted by buying some stability since any downside on a SIPP cost me money, the upside is skewed (ie taxed) by around 50%.

By comparison, the annuity quote offered 4.8% RPI linked but for reasons above, tempted by high ("jam today") level rate.

I really appreciate thoughts from the experts here.Good analysis, although another thing to account for is sequence of inflation risk. Just like SORR with an equity based drawdown, with a fixed/capped income stream like DB pension or level annuities, high inflation towards the start of retirement will have a far bigger impact than high inflation towards the end. So modelling assuming a constant inflation rate, whatever that rate is, could be misleading. If inflation is 10% for the first 3 years of retirement then that's a permanent 25% reduction in the value of a level annuity, or a 13% reduction in a 5% capped DB

I've assumed

A portfolio with 60% UK stocks and 40% UK intermediate gilts with a withdrawal of 1/n over 20 years (i.e., the first withdrawal is 5% of the portfolio, the last 100%).

A level annuity bought with £720k a 7.5% payout rate

DB and state pensions as per original post.

The plot shows the contributions of the various sources of income, as well as the total income, plotted in real (i.e., inflation adjusted) terms as a function of time for this one historical example (one of the worst periods for UK inflation).

A few things to note:

1) High inflation meant that the real purchasing power of the annuity and DB pension both decline with time. By the late 70s, the complete lack of inflation protection for the level annuity meant that the real income fell below that of the DB pension and was less than half of its original value. By the mid, 1980s, the purchasing power of the annuity had even fallen below that of the state pension.

2) The income from the portfolio was highly variable (e.g., falling by nearly half after the stock market crash in the early 70s), but gradually increases as 1/n becomes larger (e.g., in the last two years, 50% and then 100% of the portfolio are taken as income) before falling to zero after 20 years. If a max income of £100k is required, then portfolio withdrawals could be delayed for a couple of years and the fall to zero delayed (the 1/n can also be capped at, say 20% of the portfolio value rather than being allowed to go to 100%).

3) The overall income is certainly front loaded with a strong decline over the first 10 years. If the retiree survived the first 20 years, then purchasing power of the remaining income was about a third of that of the original income.

To reiterate, this was a nasty historical period for retirees with non inflation protected income (i.e., it is about as bad as it has got for UK retirees). I've assumed the state pension was index linked throughout (i.e., the other two parts of the triple lock were not triggered), but for those wanting to know how the state pension was actually uprated during this period, there an interesting (at least to me) history at https://ifs.org.uk/sites/default/files/output_url_files/bn105.pdf

4

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards