We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

City of London IT

Comments

-

It's also been hit by a move from a premium to a small discount to NAV.tacpot12 said:CTY is about 7% of my retirement portfolio and I am keeping it as it is one on my highest yeilding ITs. (5% pa over the last 5 years). The share price has dropped about 14% since I bought the shares, but my entire portfolio has dropped by 9% over the same period. I think CTY may have dropped a little more as it has been very popular for its dividend, and people may be worried about how much they have invested in it and want to diversify, or just need the money. There has been a lot of outflow from pensions over the last 18 months as people try to cope with inflation.0 -

Its recent dividend increases have been pretty low as it tries to cling onto its dividend hero status. The UK stock market dividends look like they have flattened and may be on the way down. CTY only has a small revenue reserve.

With cash in savings accounts paying around the same yield and no sign that CTY will increase its dividend by much if at all, maybe people have begun to jump ship and the discount is beginning to grow.0 -

Total return is from dividends and capital growth. Total return pays the bills, whether you get it from dividends or capital growth. We’ll be able to pay fewer bills if we choose an investment for dividends which also has less total return than another with more total return but less in dividends.

‘It's not a suitable investment for total return, that's not its objective’Is that statement really what was intended, or that it’s not suitable for capital growth? I feel confused.

1 -

tacpot12 said:CTY is about 7% of my retirement portfolio and I am keeping it as it is one on my highest yeilding ITs. (5% pa over the last 5 years). The share price has dropped about 14% since I bought the shares, but my entire portfolio has dropped by 9% over the same period. I think CTY may have dropped a little more as it has been very popular for its dividend, and people may be worried about how much they have invested in it and want to diversify, or just need the money. There has been a lot of outflow from pensions over the last 18 months as people try to cope with inflation.CTY has been on my radar for an income portfolio for a number of years, however I am just wondering about peoples' thoughts on this...These days why invest in CTY (or other 5% yielding trusts), when Money Market Funds are yielding the SONIA rate (~5.18%) with very small risk of capital loss?If you want to be rich, live like you're poor; if you want to be poor, live like you're rich.0

-

Nobody knows really where base rates and inflation are heading. In the last few months UK inflation is easing but still above the base rate. Historically the BOE and FED etc have attempted to maintain rates above inflation despite 2008 crisis onwards. There's hints rises are coming to an end ?Bravepants said:tacpot12 said:CTY is about 7% of my retirement portfolio and I am keeping it as it is one on my highest yeilding ITs. (5% pa over the last 5 years). The share price has dropped about 14% since I bought the shares, but my entire portfolio has dropped by 9% over the same period. I think CTY may have dropped a little more as it has been very popular for its dividend, and people may be worried about how much they have invested in it and want to diversify, or just need the money. There has been a lot of outflow from pensions over the last 18 months as people try to cope with inflation.CTY has been on my radar for an income portfolio for a number of years, however I am just wondering about peoples' thoughts on this...These days why invest in CTY (or other 5% yielding trusts), when Money Market Funds are yielding the SONIA rate (~5.18%) with very small risk of capital loss?

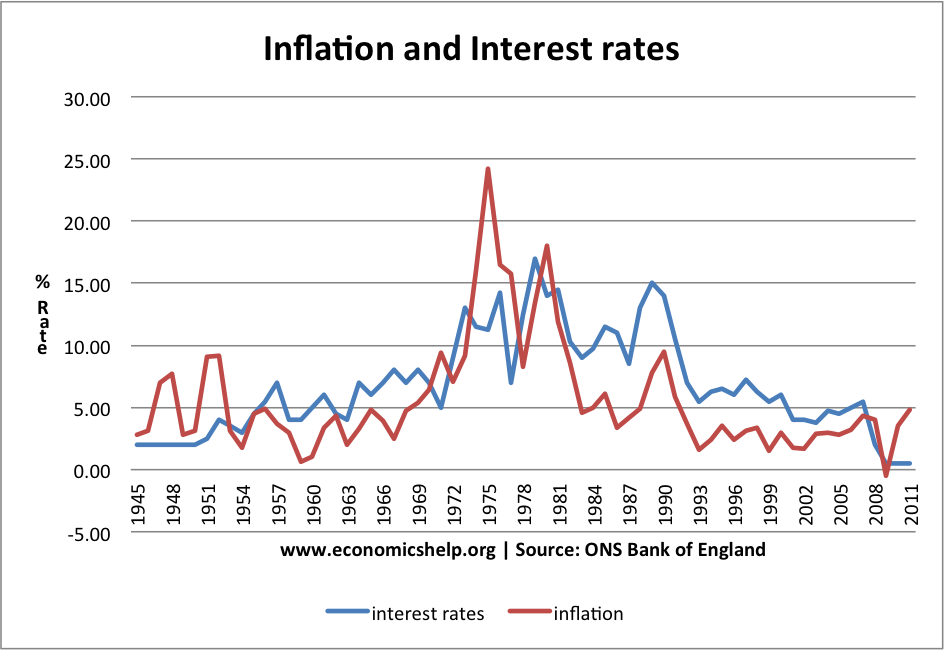

inflation-interest-rates-1945-2011.png (944×650) (economicshelp.org)

Maybe not short term but long term share price growth plus the dividends have outperformed cash investment. Depends on the level of risk you want to take and cash itself can be risky.

EuQplORWYAAGRtk (634×451) (twimg.com)

Just to back up an earlier post the FTSE is undervalued against other markets.

F5bldxga4AAZKqV (900×512) (twimg.com)

1 -

-

It hasn't cut them but the increases haven't been good either, not even close to matching inflation. Its hands are tied as it generates dividends only from incoming dividends not capital. Some other trusts with lower starting yields have done better. So over the short/medium term the income has not been great and neither has the capital gain.Linton said:

Keeping up with inflation in the medium to short term seems elusive. Maybe only certain infrastructure trusts will manage it, but they don't need to distribute their income if they don't want to.0 -

You should not expect dividends to suddenly increase with a step change in inflation. It has to work its way through the companies business and finances to appear in the profits and hence eventually in dividends which will take some years.Prism said:

It hasn't cut them but the increases haven't been good either, not even close to matching inflation. Its hands are tied as it generates dividends only from incoming dividends not capital. Some other trusts with lower starting yields have done better. So over the short/medium term the income has not been great and neither has the capital gain.Linton said:

Keeping up with inflation in the medium to short term seems elusive. Maybe only certain infrastructure trusts will manage it, but they don't need to distribute their income if they don't want to.

I see no way to get income matching inflation in the short/medium term other than with an annuity.0 -

I wouldn't expect the dividends to increase with inflation but that is one of the current issues that people are trying to solve over the short/medium term. So what is the point of holding a trust that pays a dividend but doesn't come close to meeting those goals? Maybe that is why the trust has moved to a discount. It doesn't seem to be helpful in solving the problem of providing a reliable current income, unless willing to accept a significant drop in real terms.Linton said:

You should not expect dividends to suddenly increase with a step change in inflation. It has to work its way through the companies business and finances to appear in the profits and hence eventually in dividends which will take some years.Prism said:

It hasn't cut them but the increases haven't been good either, not even close to matching inflation. Its hands are tied as it generates dividends only from incoming dividends not capital. Some other trusts with lower starting yields have done better. So over the short/medium term the income has not been great and neither has the capital gain.Linton said:

Keeping up with inflation in the medium to short term seems elusive. Maybe only certain infrastructure trusts will manage it, but they don't need to distribute their income if they don't want to.

I see no way to get income matching inflation in the short/medium term other than with an annuity.

Maybe better to look elsewhere.0 -

Asd far as I know there is no way to provide income with short term inflation protection other than through an inflation linked annuity. One would expect dividends to increase with inflation over the long term as companies in the future will presumably be as profitable in real terms as they are now.Prism said:

I wouldn't expect the dividends to increase with inflation but that is one of the current issues that people are trying to solve over the short/medium term. So what is the point of holding a trust that pays a dividend but doesn't come close to meeting those goals? Maybe that is why the trust has moved to a discount. It doesn't seem to be helpful in solving the problem of providing a reliable current income, unless willing to accept a significant drop in real terms.Linton said:

You should not expect dividends to suddenly increase with a step change in inflation. It has to work its way through the companies business and finances to appear in the profits and hence eventually in dividends which will take some years.Prism said:

It hasn't cut them but the increases haven't been good either, not even close to matching inflation. Its hands are tied as it generates dividends only from incoming dividends not capital. Some other trusts with lower starting yields have done better. So over the short/medium term the income has not been great and neither has the capital gain.Linton said:

Keeping up with inflation in the medium to short term seems elusive. Maybe only certain infrastructure trusts will manage it, but they don't need to distribute their income if they don't want to.

I see no way to get income matching inflation in the short/medium term other than with an annuity.

Maybe better to look elsewhere.

I personally do not hold City of London because its yield is rather low compared with other options.

It is unreasonable to rule out an option because it does not solve all retirement problems - nothing does. A key advantage of using income funds is that it reduces the ongoing load on the growth funds thus reducing the effect of SOR.

On the question of how to handle short term inflation when needing income ...

- barring hyper-inflation one can absorb it for some years within one's current income stream and by taking a relatively small amount of money from cash/cautious investment buffers.

- over the medium to long term, if necessary one can assign more money to income funds as part of strategic asset allocation.1

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards