We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Buy to Let - has the time passed?

Comments

-

Any idea what this property would be worth now?[Deleted User] said:

A property we rented in 2018 for 650 is now 950. Paying someone else's mortgage or paying interest on your own. No choice is a big winner really in our locality.TerryTeacake said:

I don't disagree that those LL who have been in the game a long time and who are not overleveraged will be in a better position than those who are overleveraged. For most cases, I have been crunching the numbers and it is definitely cheaper to rent at the moment than to buy especially where the interest rates are along with these high house prices. Surely something has to give!Mstty said:

I think you will find teacake I never said things were Rosey. I merely highlighted from a posted article that supply reducing (so yes LL exiting the market could well add to that especially those leveraged in the last few years with no reserves) means more demand on the properties left and higher rents.TerryTeacake said:

I wouldn't say things are as rosy as you make out. The chart shows a major increase in landlords defaulting on their mortgages. Also in the last quarter, there has been a massive increase in mortgage holders falling behind on their mortgage payments.Mstty said:From that article linked aboveThere are still 43 per cent fewer rental homes on the market than there were in 2019, with every region of the country recording a fall of at least 25 per cent, and Scotland leading the way with a 65 per cent drop.

That only means one thing. Demand grossly outstripping supply and higher rents.Apologies if the image is not very clear but you can click on the above link to see better.

Demand outsripping supply grossly.

Put another way those LL that have been in the game a long time with no to little BTL mortgage debt will be making as much money in the next few years as they did when the tax breaks were at there optimum.0 -

Why not ask Tony? A very knowledgable chap I seem to rememberTerryTeacake said:

Any idea what this property would be worth now?[Deleted User] said:

A property we rented in 2018 for 650 is now 950. Paying someone else's mortgage or paying interest on your own. No choice is a big winner really in our locality.TerryTeacake said:

I don't disagree that those LL who have been in the game a long time and who are not overleveraged will be in a better position than those who are overleveraged. For most cases, I have been crunching the numbers and it is definitely cheaper to rent at the moment than to buy especially where the interest rates are along with these high house prices. Surely something has to give!Mstty said:

I think you will find teacake I never said things were Rosey. I merely highlighted from a posted article that supply reducing (so yes LL exiting the market could well add to that especially those leveraged in the last few years with no reserves) means more demand on the properties left and higher rents.TerryTeacake said:

I wouldn't say things are as rosy as you make out. The chart shows a major increase in landlords defaulting on their mortgages. Also in the last quarter, there has been a massive increase in mortgage holders falling behind on their mortgage payments.Mstty said:From that article linked aboveThere are still 43 per cent fewer rental homes on the market than there were in 2019, with every region of the country recording a fall of at least 25 per cent, and Scotland leading the way with a 65 per cent drop.

That only means one thing. Demand grossly outstripping supply and higher rents.Apologies if the image is not very clear but you can click on the above link to see better.

Demand outsripping supply grossly.

Put another way those LL that have been in the game a long time with no to little BTL mortgage debt will be making as much money in the next few years as they did when the tax breaks were at there optimum.

3 -

I remember thinking around the time that I would never pay 160k for a 2 up 2 down, as several years previously I am sure the going rate was 120k for the same, but many have sold for 200ish. The price is the price I suppose but clearly there are parts of the country where 200k goes much further.TerryTeacake said:

Any idea what this property would be worth now?[Deleted User] said:

A property we rented in 2018 for 650 is now 950. Paying someone else's mortgage or paying interest on your own. No choice is a big winner really in our localityTerryTeacake said:

I don't disagree that those LL who have been in the game a long time and who are not overleveraged will be in a better position than those who are overleveraged. For most cases, I have been crunching the numbers and it is definitely cheaper to rent at the moment than to buy especially where the interest rates are along with these high house prices. Surely something has to give!Mstty said:

I think you will find teacake I never said things were Rosey. I merely highlighted from a posted article that supply reducing (so yes LL exiting the market could well add to that especially those leveraged in the last few years with no reserves) means more demand on the properties left and higher rents.TerryTeacake said:

I wouldn't say things are as rosy as you make out. The chart shows a major increase in landlords defaulting on their mortgages. Also in the last quarter, there has been a massive increase in mortgage holders falling behind on their mortgage payments.Mstty said:From that article linked aboveThere are still 43 per cent fewer rental homes on the market than there were in 2019, with every region of the country recording a fall of at least 25 per cent, and Scotland leading the way with a 65 per cent drop.

That only means one thing. Demand grossly outstripping supply and higher rents.Apologies if the image is not very clear but you can click on the above link to see better.

Demand outsripping supply grossly.

Put another way those LL that have been in the game a long time with no to little BTL mortgage debt will be making as much money in the next few years as they did when the tax breaks were at there optimum.0 -

I thought I would crunch the numbers for you so we can see what the true costs are.[Deleted User] said:

I remember thinking around the time that I would never pay 160k for a 2 up 2 down, as several years previously I am sure the going rate was 120k for the same, but many have sold for 200ish. The price is the price I suppose but clearly there are parts of the country where 200k goes much further.TerryTeacake said:

Any idea what this property would be worth now?[Deleted User] said:

A property we rented in 2018 for 650 is now 950. Paying someone else's mortgage or paying interest on your own. No choice is a big winner really in our localityTerryTeacake said:

I don't disagree that those LL who have been in the game a long time and who are not overleveraged will be in a better position than those who are overleveraged. For most cases, I have been crunching the numbers and it is definitely cheaper to rent at the moment than to buy especially where the interest rates are along with these high house prices. Surely something has to give!Mstty said:

I think you will find teacake I never said things were Rosey. I merely highlighted from a posted article that supply reducing (so yes LL exiting the market could well add to that especially those leveraged in the last few years with no reserves) means more demand on the properties left and higher rents.TerryTeacake said:

I wouldn't say things are as rosy as you make out. The chart shows a major increase in landlords defaulting on their mortgages. Also in the last quarter, there has been a massive increase in mortgage holders falling behind on their mortgage payments.Mstty said:From that article linked aboveThere are still 43 per cent fewer rental homes on the market than there were in 2019, with every region of the country recording a fall of at least 25 per cent, and Scotland leading the way with a 65 per cent drop.

That only means one thing. Demand grossly outstripping supply and higher rents.Apologies if the image is not very clear but you can click on the above link to see better.

Demand outsripping supply grossly.

Put another way those LL that have been in the game a long time with no to little BTL mortgage debt will be making as much money in the next few years as they did when the tax breaks were at there optimum.

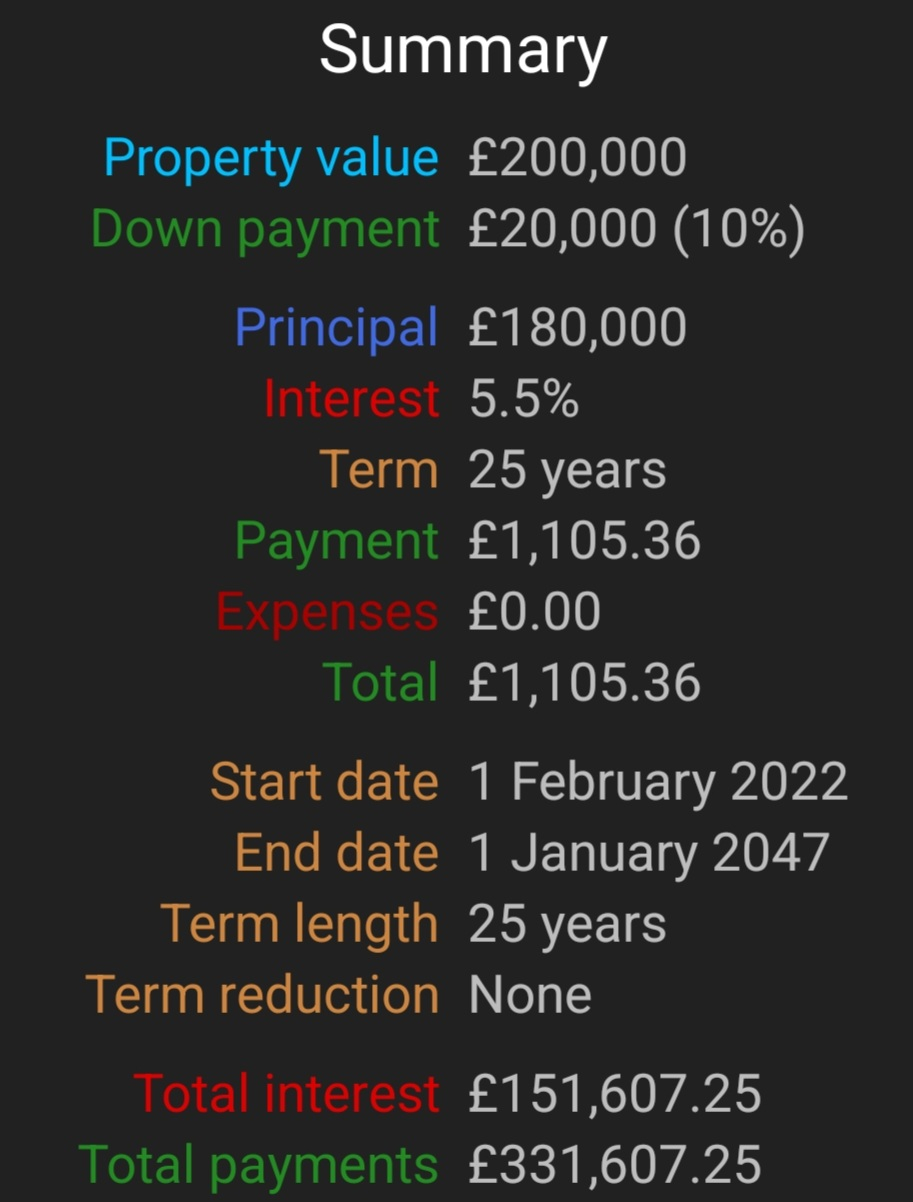

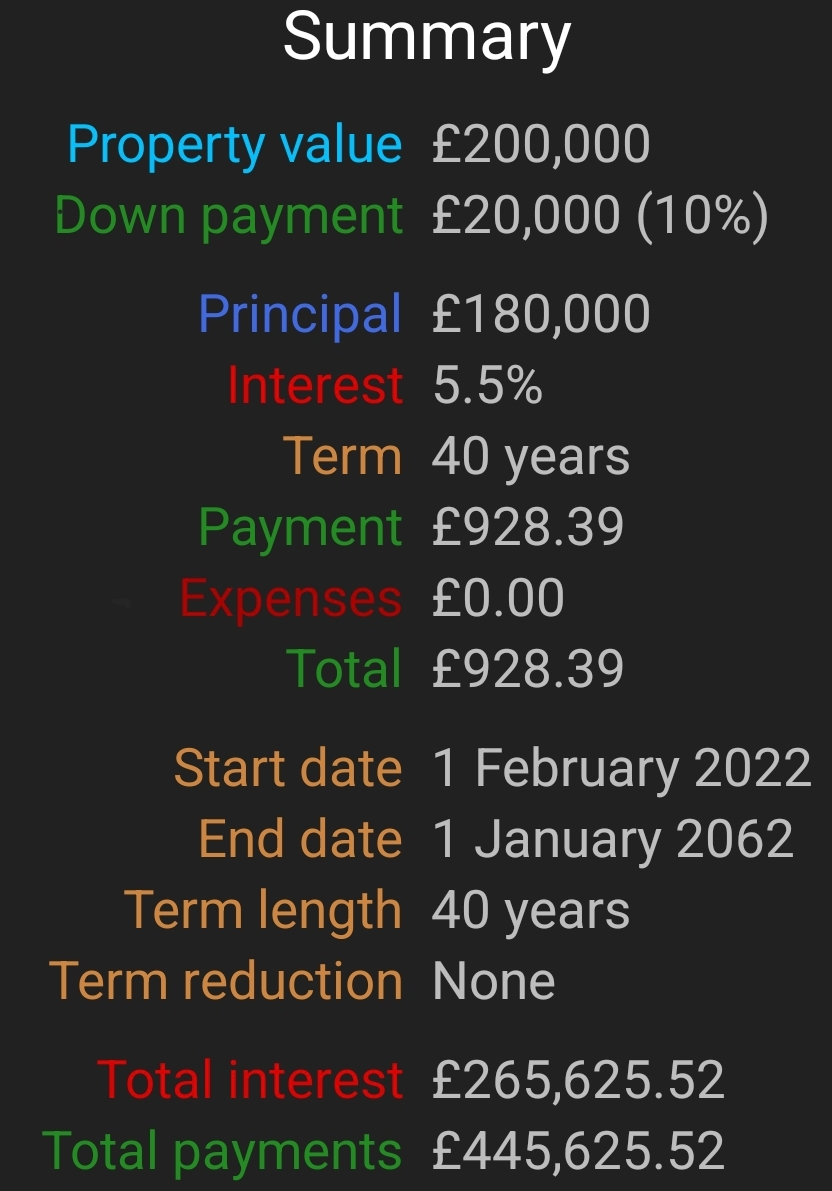

Based on a 25 year mortgage with a 10% deposit your monthly payments would be £1,105 plus other charges like ground rent with it been a flat.

Plenty of stories out there of people taking longer term mortgages so I thought I would show you an example.

As you can see in the first 5 years you would have been paying a hell of a lot of interest and you can see you not a lot of the principle would of been paid off, just under 7k. When you view it this way renting doesn't seem that bad at all especially the direction the market is heading.Year Interest Principal Balance 2022 9,048.58 1,163.68 178,836.32 2023 9,802.60 1,338.04 177,498.29 2024 9,727.13 1,413.51 176,084.78 2025 9,647.39 1,493.24 174,591.53 2026 9,563.16 1,577.48 173,014.06

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards