We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

City of london IT

Comments

-

I had it a few years ago for part of the UK portfolio but did not particularly need the income and total return was poor so dumped. The argument for it is whether you want dividends and are not too worried about growth.1

-

A bit of reading..

Fundswire article | Trustnet

Two of the quarterly dividends in 2023 are up so far on 2022 payments. Selecting ANNUAL DIVIDENDS tab shows the percentage changes since 2006.

City of London Investment Trust (CTY) Dividends (dividendmax.com)

Maybe it is similar to a FTSE tracker but as part of an income portfolio it's not bad. I've posted some information about the FTSE in this thread and dividends have well outperformed inflation.

If I don't buy annuity, give me the name of 3 funds to do the same in a SIPP drawdown scenario — MoneySavingExpert Forum

This chart will go to JAN 1995 showing CTY and inflation.

Chart Tool | Trustnet

3 -

At what point does any investment become an issue if it doesn't come close to inflation increases though?Prism said:

Is that not going to cause a bit of a problem though over time? The dividends are unaffected but the increase this year has been tiny - 1% I think. At what point does an income focused trust become an issue if it doesn't come close to inflation increases.ColdIron said:I use it for income and the dividends are unaffected. I'll worry about the eventual share price when I come to sell it whenever that may be. It's not an investment I would have for growth

0 -

None I suppose but I am interested how people use these types of trusts during retirement, as it will become a consideration for me in a few years. The idea of natural yield directly from company dividends or a smoothing of it using ITs is interesting but only if it works over time and especially during difficult economic times. The dividends ideally would need to cover a core level of income, which may be increasing due to inflation. As there are no guarantees that will happen I do wonder what people do to top that up if needed. It doesn't seem to create the simple strategy that I might hope for. I assume most people need to use a combination of drawdown and income in those cases but it seems more complicated than just drawdown.MK62 said:

At what point does any investment become an issue if it doesn't come close to inflation increases though?Prism said:

Is that not going to cause a bit of a problem though over time? The dividends are unaffected but the increase this year has been tiny - 1% I think. At what point does an income focused trust become an issue if it doesn't come close to inflation increases.ColdIron said:I use it for income and the dividends are unaffected. I'll worry about the eventual share price when I come to sell it whenever that may be. It's not an investment I would have for growth

I also question the relevance of long histories of increasing dividends, when those increases are not that much when someone really needs it. I am experimenting with index linked infrastructure and property trusts in the run up to my own retirement - these have never been properly tested in inflationary times due to short history. So far the results are not great to be honest.0 -

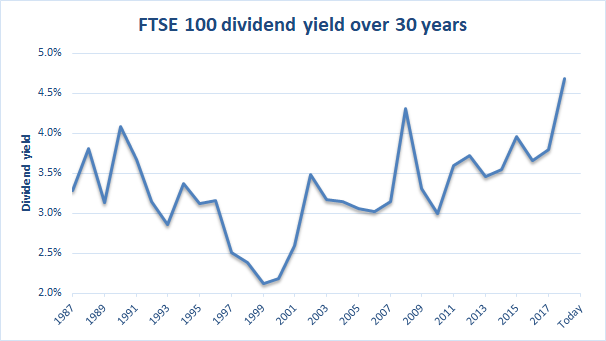

Timing really is key regarding stock market valuations and dividend yields when expressed as a percentage of index or fund. Look no further than1999 dotcom boom ,high valuations and the FTSE yield was only 2%. Easy to say with hindsight it was better to top slice the fund than take the income. When you buy today the FTSE would be yielding nearly 4% and valuations very realistic so a potential to lock in at a good starting level. As my link shows above dividends have outpaced inflation from decent levels.Prism said:

None I suppose but I am interested how people use these types of trusts during retirement, as it will become a consideration for me in a few years. The idea of natural yield directly from company dividends or a smoothing of it using ITs is interesting but only if it works over time and especially during difficult economic times. The dividends ideally would need to cover a core level of income, which may be increasing due to inflation. As there are no guarantees that will happen I do wonder what people do to top that up if needed. It doesn't seem to create the simple strategy that I might hope for. I assume most people need to use a combination of drawdown and income in those cases but it seems more complicated than just drawdown.MK62 said:

At what point does any investment become an issue if it doesn't come close to inflation increases though?Prism said:

Is that not going to cause a bit of a problem though over time? The dividends are unaffected but the increase this year has been tiny - 1% I think. At what point does an income focused trust become an issue if it doesn't come close to inflation increases.ColdIron said:I use it for income and the dividends are unaffected. I'll worry about the eventual share price when I come to sell it whenever that may be. It's not an investment I would have for growth

I also question the relevance of long histories of increasing dividends, when those increases are not that much when someone really needs it. I am experimenting with index linked infrastructure and property trusts in the run up to my own retirement - these have never been properly tested in inflationary times due to short history. So far the results are not great to be honest.

saupload_FTSE-100-dividend-yield.png (606×341) (seekingalpha.com)

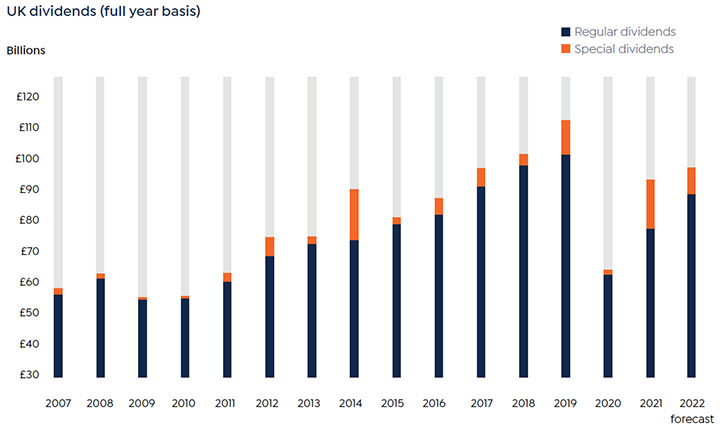

Like everything there's always a catch , do I go growth and top slice or use income funds? We can only use history to suggest what might happen in downturns ? This one shows actual pay outs during 2008 GFC. Just like the market itself down and a recovery in a few years. If your dividends are already outperforming inflation then it's no big issue. Well unless you need more and more so a lump sum in cash might come in handy.?

LinkQ22022dividends.jpg (725×430) (morningstar.co.uk)

This one shows the payments motoring from 2010 until the pandemic. A one off event but still recovering again.

FTSE100-Dividend-chart-1.png (482×296) (dzexi57u5vx1h.cloudfront.net)

At the end of the day there's no doubt many income funds fail to outperform a simple global tracker.

Chart Tool | Trustnet

This on ain't bad

JPMorgan Global Growth & Income plc Ord Fund factsheet | Trustnet

0 -

coastline said:

Timing really is key regarding stock market valuations and dividend yields when expressed as a percentage of index or fund. Look no further than1999 dotcom boom ,high valuations and the FTSE yield was only 2%. Easy to say with hindsight it was better to top slice the fund than take the income. When you buy today the FTSE would be yielding nearly 4% and valuations very realistic so a potential to lock in at a good starting level. As my link shows above dividends have outpaced inflation from decent levels.Prism said:

None I suppose but I am interested how people use these types of trusts during retirement, as it will become a consideration for me in a few years. The idea of natural yield directly from company dividends or a smoothing of it using ITs is interesting but only if it works over time and especially during difficult economic times. The dividends ideally would need to cover a core level of income, which may be increasing due to inflation. As there are no guarantees that will happen I do wonder what people do to top that up if needed. It doesn't seem to create the simple strategy that I might hope for. I assume most people need to use a combination of drawdown and income in those cases but it seems more complicated than just drawdown.MK62 said:

At what point does any investment become an issue if it doesn't come close to inflation increases though?Prism said:

Is that not going to cause a bit of a problem though over time? The dividends are unaffected but the increase this year has been tiny - 1% I think. At what point does an income focused trust become an issue if it doesn't come close to inflation increases.ColdIron said:I use it for income and the dividends are unaffected. I'll worry about the eventual share price when I come to sell it whenever that may be. It's not an investment I would have for growth

I also question the relevance of long histories of increasing dividends, when those increases are not that much when someone really needs it. I am experimenting with index linked infrastructure and property trusts in the run up to my own retirement - these have never been properly tested in inflationary times due to short history. So far the results are not great to be honest.

saupload_FTSE-100-dividend-yield.png (606×341) (seekingalpha.com)

1) Like everything there's always a catch , do I go growth and top slice or use income funds? We can only use history to suggest what might happen in downturns ? This one shows actual pay outs during 2008 GFC. Just like the market itself down and a recovery in a few years. If your dividends are already outperforming inflation then it's no big issue. Well unless you need more and more so a lump sum in cash might come in handy.?

LinkQ22022dividends.jpg (725×430) (morningstar.co.uk)

This one shows the payments motoring from 2010 until the pandemic. A one off event but still recovering again.

FTSE100-Dividend-chart-1.png (482×296) (dzexi57u5vx1h.cloudfront.net)

2) At the end of the day there's no doubt many income funds fail to outperform a simple global tracker.

Chart Tool | Trustnet

This on ain't bad

JPMorgan Global Growth & Income plc Ord Fund factsheet | Trustnet

1) Why not do both? Let income funds produce income and hold growth funds for growth

2)

Whether income funds generally fail to outperform a global tracker rather depends on the time frame

1

{kind=link}

{kind=link}

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 352.2K Banking & Borrowing

- 253.6K Reduce Debt & Boost Income

- 454.3K Spending & Discounts

- 245.3K Work, Benefits & Business

- 601K Mortgages, Homes & Bills

- 177.5K Life & Family

- 259.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards