We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Annuity Cost - Hargreaves Lansdown

Comments

-

The provider pays them, I get the annuity as quoted.Qyburn said:

Are the figures quoted by HL net of commission? For example say they quote £10k/year, is that after commission is taken or do you get a separate bill for the 0.8%?FIREDreamer said:I have expressed the commissions as a percentage of the purchase cost for all the quotes. Most are 0.78%, one is 0.80% and one outlier is 0.42% (the lowest quote, 5% worse than the best!) …

Not sure if I should wait until 65 before I buy an annuity though, best rates have reduced by 5% (8% by Aviva) in the last fortnight so I feel I have missed the boat somewhat.

eg Single Life (but same impact for Joint Life)

End July August 9th

August 9th 1

1 -

The provider pays them, I get the annuity as quoted.That means the annuity rate will be the lower commission rate version. Whilst the provider facilitates the commission payment, you pay for it in the lower annuity rate.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

Great post here, looking at average and grooping, it sorta looks like Aviva just wanted to grab more market share at that point in time, it certainly sticks out head and shoulders from the pack a few weeks ago.FIREDreamer said:

The provider pays them, I get the annuity as quoted.Qyburn said:

Are the figures quoted by HL net of commission? For example say they quote £10k/year, is that after commission is taken or do you get a separate bill for the 0.8%?FIREDreamer said:I have expressed the commissions as a percentage of the purchase cost for all the quotes. Most are 0.78%, one is 0.80% and one outlier is 0.42% (the lowest quote, 5% worse than the best!) …

Not sure if I should wait until 65 before I buy an annuity though, best rates have reduced by 5% (8% by Aviva) in the last fortnight so I feel I have missed the boat somewhat.

eg Single Life (but same impact for Joint Life)

End JulyAugust 9th

Looking at some others there, some companies did increase pay outs on that latest screenshot.

Maybe that Aviva figure will prove to be a high, but the future looks a bit bumpy, I definitely won't be surprised if that Aviva deal is topped, time will tell.

0 -

Are annuities a bit like car insurance or house insurance then? You might find that a particular provider decides that they need to sell some more policies at that moment to meet some kind of goal in some spreadsheet or other, and at other times that provider might be completely uncompetitive as they don't want any more business at that moment?RogerPensionGuy said:

Great post here, looking at average and grooping, it sorta looks like Aviva just wanted to grab more market share at that point in time, it certainly sticks out head and shoulders from the pack a few weeks ago.FIREDreamer said:

The provider pays them, I get the annuity as quoted.Qyburn said:

Are the figures quoted by HL net of commission? For example say they quote £10k/year, is that after commission is taken or do you get a separate bill for the 0.8%?FIREDreamer said:I have expressed the commissions as a percentage of the purchase cost for all the quotes. Most are 0.78%, one is 0.80% and one outlier is 0.42% (the lowest quote, 5% worse than the best!) …

Not sure if I should wait until 65 before I buy an annuity though, best rates have reduced by 5% (8% by Aviva) in the last fortnight so I feel I have missed the boat somewhat.

eg Single Life (but same impact for Joint Life)

End JulyAugust 9th

Looking at some others there, some companies did increase pay outs on that latest screenshot.

Maybe that Aviva figure will prove to be a high, but the future looks a bit bumpy, I definitely won't be surprised if that Aviva deal is topped, time will tell.0 -

...but why buy an annuity over holding gilts (which is esentially all the insurance company does (?) - isn't it like comparing an actively managed (expensive) fund over a cheap diy tracker ?

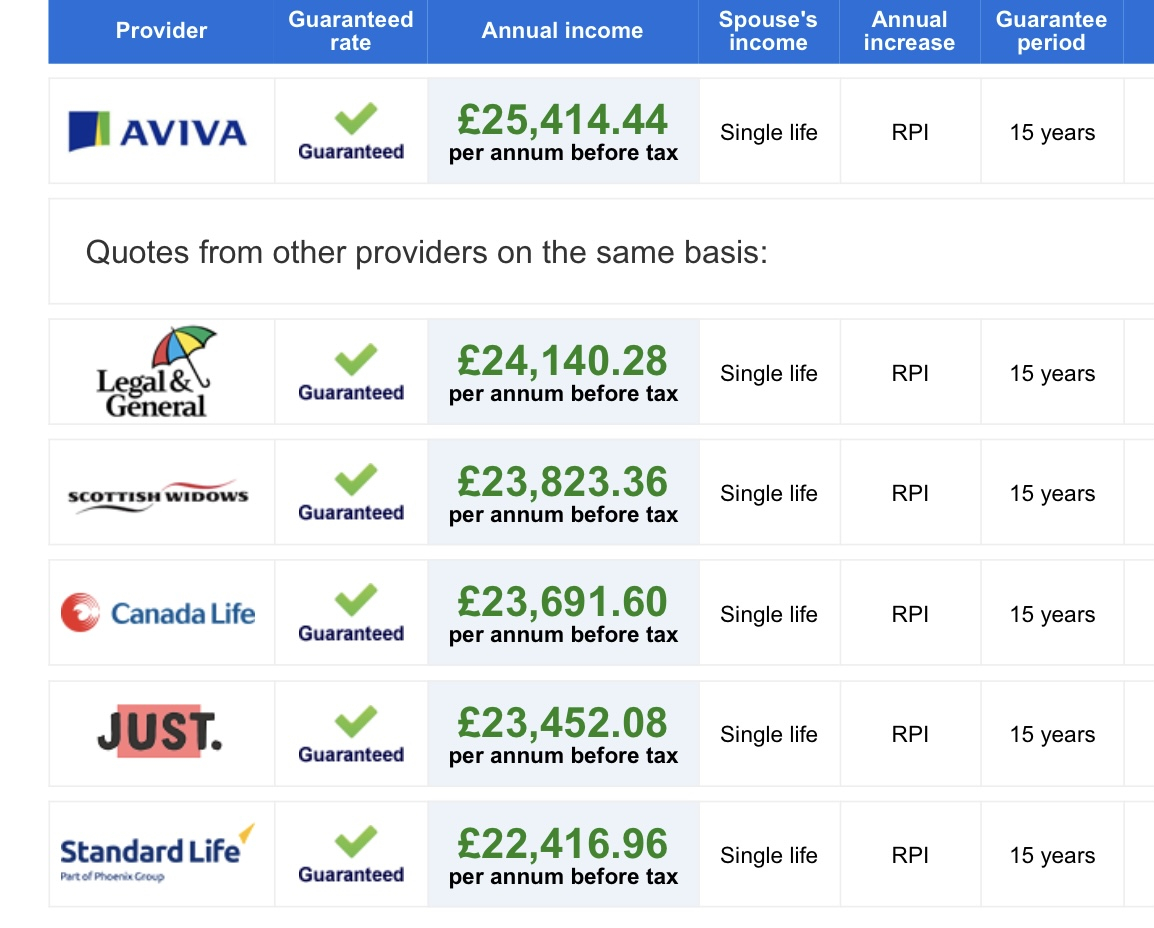

For example from HL

would provide ...So about the same % income, 100% spousal, and 10 year guarantee. OK it's not index linked, but you get all your money back at the end and can "get out" part way through if your circumstances change. Surely getting all your money back beats the "index linked" element - which is probably capped anyway...

...So about the same % income, 100% spousal, and 10 year guarantee. OK it's not index linked, but you get all your money back at the end and can "get out" part way through if your circumstances change. Surely getting all your money back beats the "index linked" element - which is probably capped anyway...

What is the USP for annuities....? What am I missing...?

0 -

The RPI quotes on the HL search aren't capped unless you specifically request capped rates.0

-

I presume that the fact of guaranteed lifeling income that you can basically ignore once set up is the main draw over having to manage Gilts in your Sipp / investment account, especially as you might lose capacity when elderly and would need someone else to manage it. A bereaved spouse might have no idea how to go about things, or even how to access the information - with an annuity, presumably the insurance company sorts everything ( for a fee?)0

-

Ciprico said:...but why buy an annuity over holding gilts (which is esentially all the insurance company does (?) - isn't it like comparing an actively managed (expensive) fund over a cheap diy tracker ?

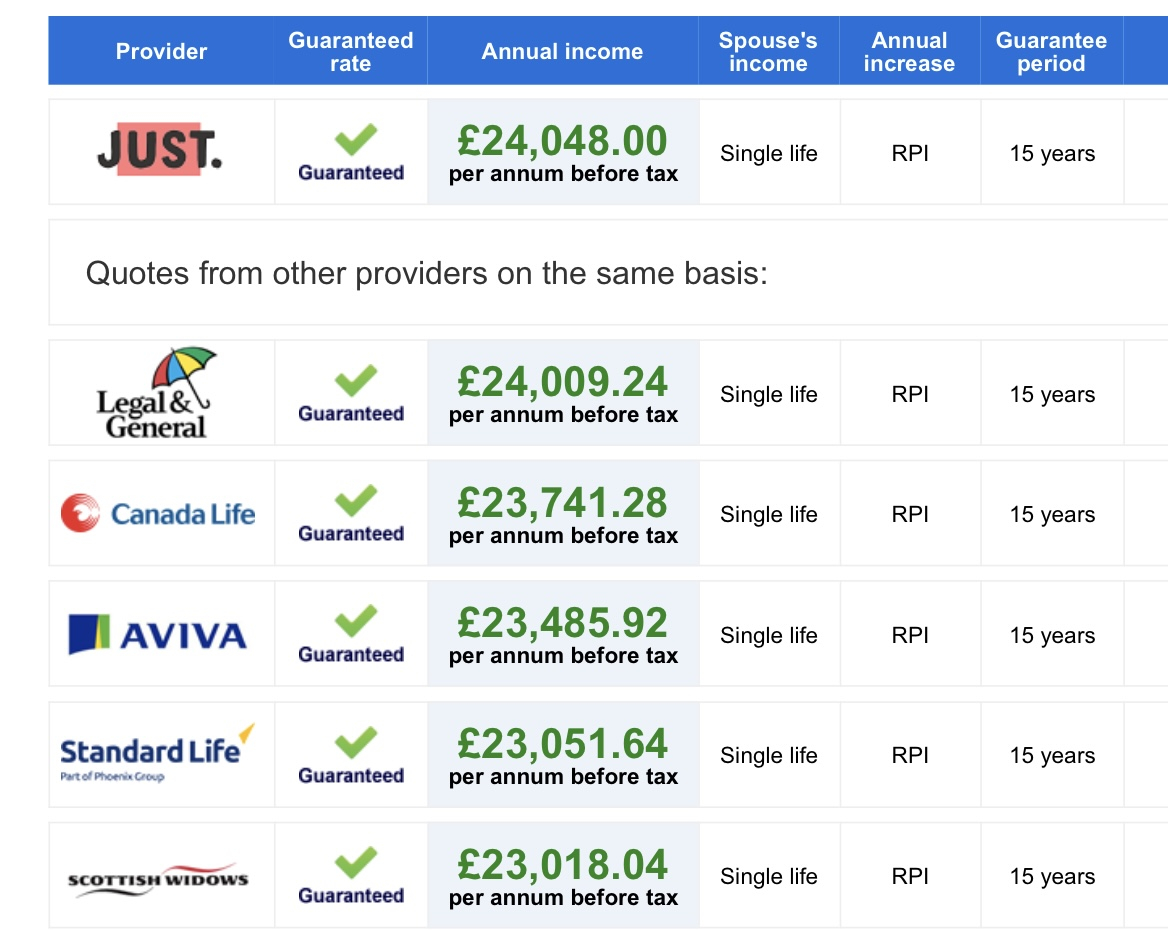

For example from HL

would provide...So about the same % income, 100% spousal, and 10 year guarantee. OK it's not index linked, but you get all your money back at the end and can "get out" part way through if your circumstances change. Surely getting all your money back beats the "index linked" element - which is probably capped anyway...

What is the USP for annuities....? What am I missing...?That you don't know how long you'll live! That's the USP of annuities over raw gilts - pooling longevity risk. Like any insurance really.I did a comparison of a gilts ladder and annuities here: https://forums.moneysavingexpert.com/discussion/6458492/if-i-dont-buy-annuity-give-me-the-name-of-3-funds-to-do-the-same-in-a-sipp-drawdown-scenario#latest

1 -

I'm not trying to be awkward, I just don't get it, if I could persuade myself it was the way to go I would, I am 60 and on the cusp of retiring - so this is not just academic

Admin easier ? A SIPP containing one gilt that pays out the same amount twice a year into your current account is not a heavy admin overhead, once set up, nothing to do for 35+ years

Rest of life ? - a 35+ year gilt still seems to beat the annuityTreasury 4% 22/01/2060

GBP | GB00B54QLM75 | B54QLM74.000% 22 January 2060 £92.120

Assuming 4% continous inflation (ouch) the original pot will have lost about 70% - but better than nothing in 30 years,

It's hard to see how an annuity can win, except if you live a long time, and then it's at the expense of someone who dies early, and all the time the annuity company taking their fees....Do the insurance companies work on the basis that maybe most people are optimistic about their life span are are not going to be the ones that die early....?

0 -

The annuities quoted have an annual RPI increase, your gilt is paying a fixed 4% (assuming you buy at par) with no annual RPI increase. The annuity not only deals with the longevity risk, it also deals with the inflation risk. It's not much consolation that you will get some money back after 35 years, if 4% is no longer enough to live on.In your example you would be on 30% of your original income after 30 years.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards