We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Trend from Passive funds to Bank accounts

Comments

-

Something has been broken, near 0% interest rates throughout the western world for 15 years.Malthusian said:

If people who take risk are getting lower returns than people who don't take risk, something is broken in the world economy. Investors need returns above the risk-free rate to persuade them to risk their capital.Sg28 said:Up to now anything that was merely above 0 growth would have beaten cash, the question is will they continue to beat it now interest rates are more normal and investors/savers dont need to look to higher risk to get returns.

If cash truly did pay more than investments over the long term, people would sell risky assets and stick their money under the mattress, which would cause the price of assets to fall, which would increase the potential returns for the investors who bought at lower prices, which would restore normality. We aren't even seeing that happen to any great extent, otherwise stockmarkets would be falling more than they have.

When prices are rising, businesses' profits rise, asset prices rise and returns rise. Investment in real assets should therefore roughly follow inflation - not consistently, but as a general rule and in the long term. Cash returns less than inflation.

Savers didn't need to look to higher risk to get returns before 2022 either. They could get a return of 1%pa on easy access. In real terms that was a better return than they are getting now. In the zero interest rate era they were making a real return of about minus 1% - 2%, now they are getting minus 6%.

I wasn't talking long term. It just seems to me that the people who were pushed into higher risk investments to chase gains will now start to back to lower risk cash.Ex Sg27 (long forgotten log in details)Massive thank you to those on the long since defunct Matched Betting board.2 -

Indeed.Malthusian said:

If people who take risk are getting lower returns than people who don't take risk, something is broken in the world economy. Investors need returns above the risk-free rate to persuade them to risk their capital.Sg28 said:Up to now anything that was merely above 0 growth would have beaten cash, the question is will they continue to beat it now interest rates are more normal and investors/savers dont need to look to higher risk to get returns.

If cash truly did pay more than investments over the long term, people would sell risky assets and stick their money under the mattress, which would cause the price of assets to fall, which would increase the potential returns for the investors who bought at lower prices, which would restore normality. We aren't even seeing that happen to any great extent, otherwise stockmarkets would be falling more than they have.

When prices are rising, businesses' profits rise, asset prices rise and returns rise. Investment in real assets should therefore roughly follow inflation - not consistently, but as a general rule and in the long term. Cash returns less than inflation.

Savers didn't need to look to higher risk to get returns before 2022 either. They could get a return of 1%pa on easy access. In real terms that was a better return than they are getting now. In the zero interest rate era they were making a real return of about minus 1% - 2%, now they are getting minus 6%.

Unilever seeing increased profits from lower sales volumes, how can that happen?

Businesses may increase things by percentages, so as cost go up the selling price doesn't just go up by the increased production costs they are seeing, the total pricing including the profit margin goes up by a percentage, so the profit margin increases as well. Profits rise then share prices rise.

Magnum-maker Unilever's profits higher after it raises prices - BBC News

2 -

Years ago the board was dominated by savings accounts and in recent years products such as VLS. Easy to see why as interest rates plummeted. Think savers have always been there it's just that rates weren't worth talking about. Since 2/3% gained ground so have the posts for best returns. Could say back to normal and next stop looks like 5/6%?Sg28 said:

Something has been broken, near 0% interest rates throughout the western world for 15 years.Malthusian said:

If people who take risk are getting lower returns than people who don't take risk, something is broken in the world economy. Investors need returns above the risk-free rate to persuade them to risk their capital.Sg28 said:Up to now anything that was merely above 0 growth would have beaten cash, the question is will they continue to beat it now interest rates are more normal and investors/savers dont need to look to higher risk to get returns.

If cash truly did pay more than investments over the long term, people would sell risky assets and stick their money under the mattress, which would cause the price of assets to fall, which would increase the potential returns for the investors who bought at lower prices, which would restore normality. We aren't even seeing that happen to any great extent, otherwise stockmarkets would be falling more than they have.

When prices are rising, businesses' profits rise, asset prices rise and returns rise. Investment in real assets should therefore roughly follow inflation - not consistently, but as a general rule and in the long term. Cash returns less than inflation.

Savers didn't need to look to higher risk to get returns before 2022 either. They could get a return of 1%pa on easy access. In real terms that was a better return than they are getting now. In the zero interest rate era they were making a real return of about minus 1% - 2%, now they are getting minus 6%.

I wasn't talking long term. It just seems to me that the people who were pushed into higher risk investments to chase gains will now start to back to lower risk cash.

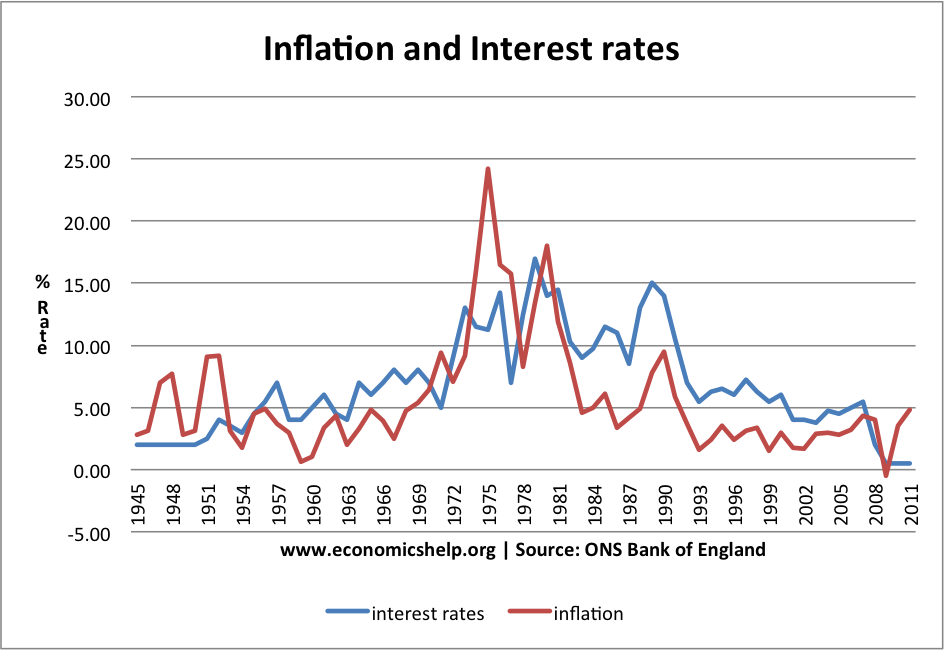

The idea that inflation outpaces interest rates isn't strictly true. The chart below ( source BOE ) shows 50 years out of 70 to 2010 interest rates above inflation . Is the chart wrong ? Remember you can usually get better than the base rate shopping around. Latest inflation figure was 7.9% , maybe rates will be above inflation by next year ? I'm sure that's the BOE aim.

inflation-interest-rates-1945-2011.png (944×650) (economicshelp.org)

Investing is a different game and data shows it outperforms cash saving longer term . Recent posts on here and pensions board have seen posters questioning returns . Equities and bonds have fallen. Bonds have had one of the worst periods in history. Look at VGOV in three years fallen from 2600 to 1600. Will hardly recover until rates are cut again.

Vanguard UK Gilt UCITS ETF, UK:VGOV Advanced Chart - (LON) UK:VGOV, Vanguard UK Gilt UCITS ETF Stock Price - BigCharts.com (marketwatch.com)

3 -

By price gouging:GazzaBloom said:

Indeed.Malthusian said:

If people who take risk are getting lower returns than people who don't take risk, something is broken in the world economy. Investors need returns above the risk-free rate to persuade them to risk their capital.Sg28 said:Up to now anything that was merely above 0 growth would have beaten cash, the question is will they continue to beat it now interest rates are more normal and investors/savers dont need to look to higher risk to get returns.

If cash truly did pay more than investments over the long term, people would sell risky assets and stick their money under the mattress, which would cause the price of assets to fall, which would increase the potential returns for the investors who bought at lower prices, which would restore normality. We aren't even seeing that happen to any great extent, otherwise stockmarkets would be falling more than they have.

When prices are rising, businesses' profits rise, asset prices rise and returns rise. Investment in real assets should therefore roughly follow inflation - not consistently, but as a general rule and in the long term. Cash returns less than inflation.

Savers didn't need to look to higher risk to get returns before 2022 either. They could get a return of 1%pa on easy access. In real terms that was a better return than they are getting now. In the zero interest rate era they were making a real return of about minus 1% - 2%, now they are getting minus 6%.

Unilever seeing increased profits from lower sales volumes, how can that happen?

Businesses may increase things by percentages, so as cost go up the selling price doesn't just go up by the increased production costs they are seeing, the total pricing including the profit margin goes up by a percentage, so the profit margin increases as well. Profits rise then share prices rise.

Magnum-maker Unilever's profits higher after it raises prices - BBC News

https://en.wikipedia.org/wiki/Price_gouging

0 -

But that's the fundamental issue here - decisions regarding saving v investing should be driven by timescales not short-term rates, i.e. invest long-term money and save short-term money....Sg28 said:

I wasn't talking long term. It just seems to me that the people who were pushed into higher risk investments to chase gains will now start to back to lower risk cash.5 -

Yes, simple as that, the ugly face of capitalism than can often benefit us shareholders so lucratively.bundoran said:

By price gouging:GazzaBloom said:

Indeed.Malthusian said:

If people who take risk are getting lower returns than people who don't take risk, something is broken in the world economy. Investors need returns above the risk-free rate to persuade them to risk their capital.Sg28 said:Up to now anything that was merely above 0 growth would have beaten cash, the question is will they continue to beat it now interest rates are more normal and investors/savers dont need to look to higher risk to get returns.

If cash truly did pay more than investments over the long term, people would sell risky assets and stick their money under the mattress, which would cause the price of assets to fall, which would increase the potential returns for the investors who bought at lower prices, which would restore normality. We aren't even seeing that happen to any great extent, otherwise stockmarkets would be falling more than they have.

When prices are rising, businesses' profits rise, asset prices rise and returns rise. Investment in real assets should therefore roughly follow inflation - not consistently, but as a general rule and in the long term. Cash returns less than inflation.

Savers didn't need to look to higher risk to get returns before 2022 either. They could get a return of 1%pa on easy access. In real terms that was a better return than they are getting now. In the zero interest rate era they were making a real return of about minus 1% - 2%, now they are getting minus 6%.

Unilever seeing increased profits from lower sales volumes, how can that happen?

Businesses may increase things by percentages, so as cost go up the selling price doesn't just go up by the increased production costs they are seeing, the total pricing including the profit margin goes up by a percentage, so the profit margin increases as well. Profits rise then share prices rise.

Magnum-maker Unilever's profits higher after it raises prices - BBC News

https://en.wikipedia.org/wiki/Price_gouging0 -

Getting less free money for putting your cash in an FSCS-protected saving account and doing nothing doesn't make the economy broken.Sg28 said:Something has been broken, near 0% interest rates throughout the western world for 15 years.

Investors getting lower long-term returns than cash savers would, because everyone would stop investing. Productive businesses would have to be wound up so investors could get their cash out, because nobody would be buying shares when they can get better returns in a bank account. For the reasons described previously, it is economically impossible.

Investors doing worse than savers over a 3 year period is just normal. You get higher returns in the long term as your reward for accepting lower returns in some random short term periods, like this one. Business as usual.I wasn't talking long term. It just seems to me that the people who were pushed into higher risk investments to chase gains will now start to back to lower risk cash.Probably, but only those who invested above their risk profile and are regretting it.

The fact that returns on cash have fallen off a cliff from minus ~1%pa to minus ~6%pa illustrates that for those who are prepared to accept risk, the impetus to do so is higher than it has been for two decades.1 -

Malthusian said:

Getting less free money for putting your cash in an FSCS-protected saving account and doing nothing doesn't make the economy broken.Sg28 said:Something has been broken, near 0% interest rates throughout the western world for 15 years.

Investors getting lower long-term returns than cash savers would, because everyone would stop investing. Productive businesses would have to be wound up so investors could get their cash out, because nobody would be buying shares when they can get better returns in a bank account. For the reasons described previously, it is economically impossible.

Investors doing worse than savers over a 3 year period is just normal. You get higher returns in the long term as your reward for accepting lower returns in some random short term periods, like this one. Business as usual.I wasn't talking long term. It just seems to me that the people who were pushed into higher risk investments to chase gains will now start to back to lower risk cash.Probably, but only those who invested above their risk profile and are regretting it.

The fact that returns on cash have fallen off a cliff from minus ~1%pa to minus ~6%pa illustrates that for those who are prepared to accept risk, the impetus to do so is higher than it has been for two decades.

My point is for someone looking at buying (or holding) vls60 for example with 10 year annualised performance of 6.11% and 5 years at 3.7% those 6%+ 1 year fixes are going to seem very attractive.Malthusian said:

Getting less free money for putting your cash in an FSCS-protected saving account and doing nothing doesn't make the economy broken.Sg28 said:Something has been broken, near 0% interest rates throughout the western world for 15 years.

Investors getting lower long-term returns than cash savers would, because everyone would stop investing. Productive businesses would have to be wound up so investors could get their cash out, because nobody would be buying shares when they can get better returns in a bank account. For the reasons described previously, it is economically impossible.

Investors doing worse than savers over a 3 year period is just normal. You get higher returns in the long term as your reward for accepting lower returns in some random short term periods, like this one. Business as usual.I wasn't talking long term. It just seems to me that the people who were pushed into higher risk investments to chase gains will now start to back to lower risk cash.Probably, but only those who invested above their risk profile and are regretting it.

The fact that returns on cash have fallen off a cliff from minus ~1%pa to minus ~6%pa illustrates that for those who are prepared to accept risk, the impetus to do so is higher than it has been for two decades.

By the way, Im not personally moving to cash and im still adding the same monthly amount to my investments, although it does seem tempting temporarily.

Ex Sg27 (long forgotten log in details)Massive thank you to those on the long since defunct Matched Betting board.2 -

What's the scenario where it would be valid to compare apples and oranges in that way?Sg28 said:My point is for someone looking at buying (or holding) vls60 for example with 10 year annualised performance of 6.11% and 5 years at 3.7% those 6%+ 1 year fixes are going to seem very attractive.3 -

I must admit I am concerned by my passive investments (Vanguard). However I am loathed to sell as that would just crystalise my losses. I am hoping for at least a modest return before I cash in. There are some good fixed rates around and I have just opened a Nat West 2 year ISA at 5.9% with the thoughts that rates might decrease in the next year.

I suppose it could be the time to purchase more from the likes of Vanguard but I can't quite bring myself to do that.0

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards