We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Dynamic spending rules for retirement drawdown pros/cons and alternatives?

Comments

-

Thanks. That makes sense. 30% of our planned annual spend will be discretionary so there is some flex if things go sideways early on.Linton said:

Furthermore whatever you decide is not cast in stone. Keep track of your expenditure and the value of your pension pot and you will see if you are off course well before it is too late to do anything about it. Unless you blindly follow some simplistic drawdown strategy you will never actually run out of money.NoMore said:Do you drive/travel by car ? There's a risk that every time you do you could be in a serious accident, but you do it anyway.

You just need to get into the same mindset with your retirement, yes you could run out of money but you should do it anyway as the risk with your current plan is small.

If you have planned prudently and get through the first few years without a serious crash you will probably be well ahead of plan and die wealthy.

There is also a considerable chance that my employer will want me to continue supporting them on an ad hoc basis via an agency, certainly in the first year, we already have 2 recent retirees back on agency books working a day or 2 a week here and there. That would probably cover the majority if not all of our day to day spend.

No income from that is factored in my plan so, as with war, at the first contact with the enemy the plan often goes out the window.

It's time...2 -

I think you said you also have a DB pension? When are you planning to put it into payment? One of the things I realised when doing these software simulations, is that putting your DB pension into payment early, gives you the best probability of overall success because the DB pension cushions the effects of SORR. Some people don’t like this because they want their guaranteed income in the last years to be as high as possible, but it’s then at the cost of having to work on for another 2 or more years to get the same overall success probability.GazzaBloom said:

Thanks. That makes sense. 30% of our planned annual spend will be discretionary so there is some flex if things go sideways early on.Linton said:

Furthermore whatever you decide is not cast in stone. Keep track of your expenditure and the value of your pension pot and you will see if you are off course well before it is too late to do anything about it. Unless you blindly follow some simplistic drawdown strategy you will never actually run out of money.NoMore said:Do you drive/travel by car ? There's a risk that every time you do you could be in a serious accident, but you do it anyway.

You just need to get into the same mindset with your retirement, yes you could run out of money but you should do it anyway as the risk with your current plan is small.

If you have planned prudently and get through the first few years without a serious crash you will probably be well ahead of plan and die wealthy.

There is also a considerable chance that my employer will want me to continue supporting them on an ad hoc basis via an agency, certainly in the first year, we already have 2 recent retirees back on agency books working a day or 2 a week here and there. That would probably cover the majority if not all of our day to day spend.

No income from that is factored in my plan so, as with war, at the first contact with the enemy the plan often goes out the window.

It's time...

I am even toying with the idea of putting my DB into payment at 55 in order to allow me to go down to 4 days a week working, whilst still contributing to my DC pension. In the past, I probably would have said - that’s crazy you will be paying 40% tax on your DB pension income. However, it’s also a relatively risk free approach that can be prolonged if needed without impacting on my investment balances. Most of my retirement scenarios call for putting DB into payment early anyway for the reason described above, so in some ways I have nothing to lose there.2 -

yep, I took a lump sum and early DB last year. This is in the Timeline plan and covers around 19% of required annual expenditure.Pat38493 said:

I think you said you also have a DB pension? When are you planning to put it into payment? One of the things I realised when doing these software simulations, is that putting your DB pension into payment early, gives you the best probability of overall success because the DB pension cushions the effects of SORR. Some people don’t like this because they want their guaranteed income in the last years to be as high as possible, but it’s then at the cost of having to work on for another 2 or more years to get the same overall success probability.GazzaBloom said:

Thanks. That makes sense. 30% of our planned annual spend will be discretionary so there is some flex if things go sideways early on.Linton said:

Furthermore whatever you decide is not cast in stone. Keep track of your expenditure and the value of your pension pot and you will see if you are off course well before it is too late to do anything about it. Unless you blindly follow some simplistic drawdown strategy you will never actually run out of money.NoMore said:Do you drive/travel by car ? There's a risk that every time you do you could be in a serious accident, but you do it anyway.

You just need to get into the same mindset with your retirement, yes you could run out of money but you should do it anyway as the risk with your current plan is small.

If you have planned prudently and get through the first few years without a serious crash you will probably be well ahead of plan and die wealthy.

There is also a considerable chance that my employer will want me to continue supporting them on an ad hoc basis via an agency, certainly in the first year, we already have 2 recent retirees back on agency books working a day or 2 a week here and there. That would probably cover the majority if not all of our day to day spend.

No income from that is factored in my plan so, as with war, at the first contact with the enemy the plan often goes out the window.

It's time...

I am even toying with the idea of putting my DB into payment at 55 in order to allow me to go down to 4 days a week working, whilst still contributing to my DC pension. In the past, I probably would have said - that’s crazy you will be paying 40% tax on your DB pension income. However, it’s also a relatively risk free approach that can be prolonged if needed without impacting on my investment balances. Most of my retirement scenarios call for putting DB into payment early anyway for the reason described above, so in some ways I have nothing to lose there.0 -

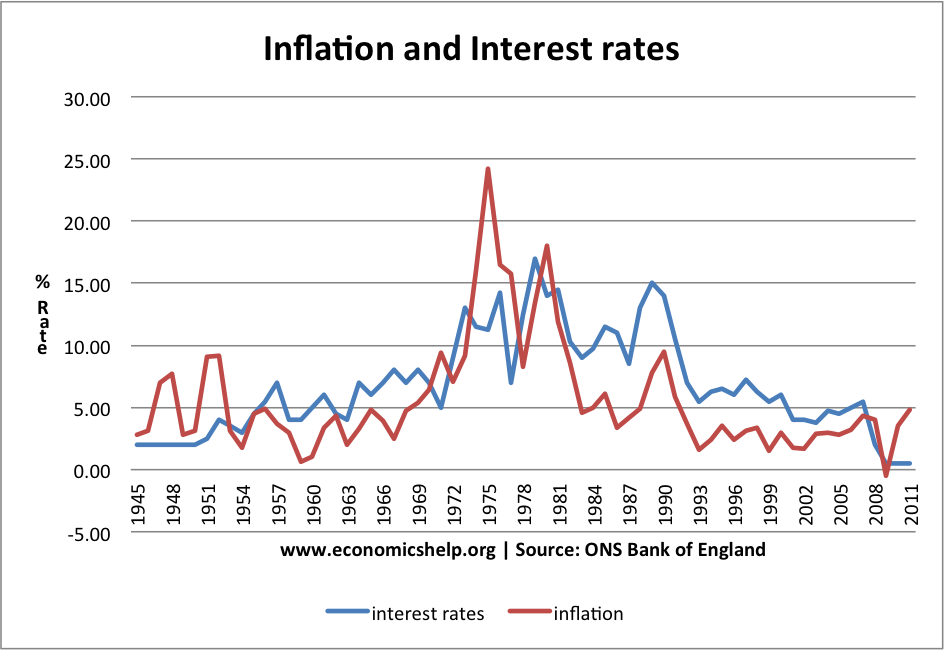

You could always increase the cash buffer from 3 years to give you peace of mind. Idea from central banks is to get rates above inflation so holding cash isn't the end of the world. US chart below shows the US are making strides towards their target. Blue is now above Red. UK as we know way behind but we shall see next year ?

F01yo-DWYAU4auL (850×595) (twimg.com)

inflation-interest-rates-1945-2011.png (944×650) (economicshelp.org)

From the Timeline link the worst case scenario was in recent decades. Although US based this link clearly shows 1972-1980 and 2000-2010 . It's set to 100% US equities ( can be adjusted for other allocations) and 4% annual withdrawal. Under the chart there's an inflation setting to add in. It's not the answer of course but the 50% drops in valuation will give many a headache. Considering markets are volatile and 10-20% isn't unusual then maybe the cash buffer could be used above 20% ?

Backtest Portfolio Asset Class Allocation (portfoliovisualizer.com)

Backtest Portfolio Asset Class Allocation (portfoliovisualizer.com)

1 -

That video and the one he linked to "how much do I need in retire with @20-£40-£60k" left me feeling a lot more positive about the futureGazzaBloom said:Coincidentally, this video just popped up in my YouTube recommendations:

Quite timely with my current musings: https://youtu.be/OuDCDp9Z9Y4

https://youtu.be/OuDCDp9Z9Y4") "All lies and jest, still a man hears what he wants to hear and disregards the rest”3

"All lies and jest, still a man hears what he wants to hear and disregards the rest”3 -

Gazzabloom must be a sports fan and have heard too often “he/she gave a 110%”.

You will keep an eye on your progress - if your plan failures so will mine and many others (more able than me).

Having read a recent link to variable withdrawals a failure rate of 90-95% is good enough as we do not blindly proceed …

Both my mother and grandmother downsized closer to some of their children (allowing visitors to stay with siblings!) which eased perceived financial squeezes. There are ways to tweak plans especially if they assume the same expenditure year in year out1 -

Was pointed at this informative thread...

I have an out-of-date Voyant report run by an FA, but without any tax optimisations (e.g. partial drawdown to use up personal allowance etc.). Before taking up the Voyant free trial offer, does it actually support such tax finessing?

The cash modelling side I can code anyway, once I have something reasonable to compare to, esp to see what dimensions make the most difference when twiddled.

But seems like folks here are able to use Timeline, which seems especially prudent for backtesting and providing some confidence intervals? I've seen mention of a free trial - but cannot see that on their site - has it been removed?

1 -

It looks like there is no free trial of Timeline anymore, I can see a link to get started first month for £1 only now, that would be worth it if there is the option to cancel after 1 month. When I signed up it was (and continues to be) a free fully working system for up to 3 clients.sofm said:Was pointed at this informative thread...

I have an out-of-date Voyant report run by an FA, but without any tax optimisations (e.g. partial drawdown to use up personal allowance etc.). Before taking up the Voyant free trial offer, does it actually support such tax finessing?

The cash modelling side I can code anyway, once I have something reasonable to compare to, esp to see what dimensions make the most difference when twiddled.

But seems like folks here are able to use Timeline, which seems especially prudent for backtesting and providing some confidence intervals? I've seen mention of a free trial - but cannot see that on their site - has it been removed?

I frequently download my full personal retirement plan report just in case it gets withdrawn at any time.0 -

Ah - it accepts a blank FCA number and then... GBP115 per month after the first month. I'll get my data in order before using the one month offer...It looks like there is no free trial of Timeline anymore, I can see a link to get started first month for £1 only now, that would be worth it if there is the option to cancel after 1 month. When I signed up it was (and continues to be) a free fully working system for up to 3 clients.0 -

If that's the case, they must have changed it recently because until recently, you could sign up with a fake FCA number and you could use it for free indefinitely but you could only have up to 3 clients set up.sofm said:

Ah - it accepts a blank FCA number and then... GBP115 per month after the first month. I'll get my data in order before using the one month offer...It looks like there is no free trial of Timeline anymore, I can see a link to get started first month for £1 only now, that would be worth it if there is the option to cancel after 1 month. When I signed up it was (and continues to be) a free fully working system for up to 3 clients.0

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards