We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Confused about savings and tax

movingforward2010

Posts: 1,588 Forumite

I earn £24000 a year. My tax code is 1257C.

I’m 41 years old. Single

I’ve got £33500 in savings in an instant access savings account at 4.36% (saving for mortgage deposit)

Do I need to put £20000 of this in an ISA so I don’t pay tax?

I’ve just renewed my ISA with Lloyds bank. ( it only has £100 in it) can I close this and move to a better paying rate one?

I’m 41 years old. Single

I’ve got £33500 in savings in an instant access savings account at 4.36% (saving for mortgage deposit)

Do I need to put £20000 of this in an ISA so I don’t pay tax?

I’ve just renewed my ISA with Lloyds bank. ( it only has £100 in it) can I close this and move to a better paying rate one?

0

Comments

-

If it may take more than a year to use the money for a deposit, then, yes, moving some to an ISA would be a good idea.

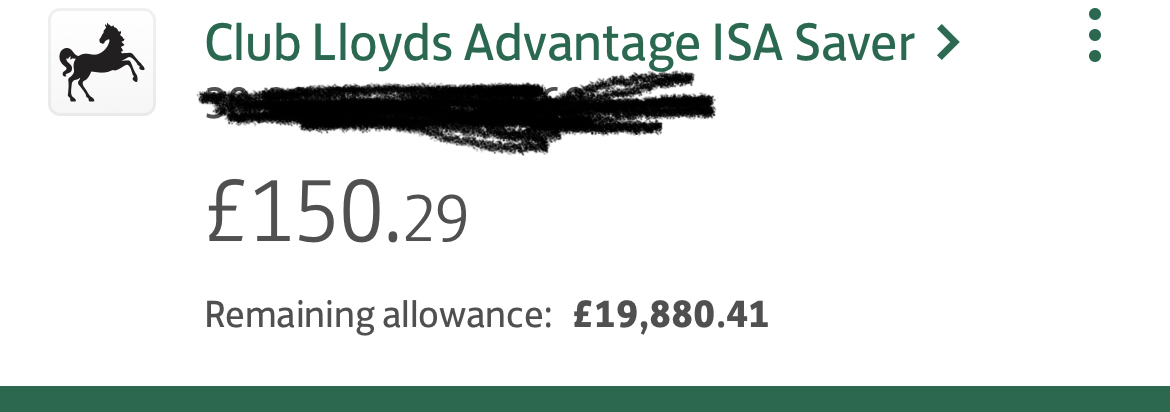

You're only allowed to pay into one cash ISA each tax year (ie April 6th to April 5th). When you say you've "renewed" the Lloyds one, do you just mean you agreed for it run for some further length of time, or did you pay any new cash into it? This could determine the order you do things next, and which other ISA to look for.1 -

You should get £1000 PSA tax free. Any more would be taxed.

I would go with Virgin money, for two reasons.

You can switch between Virgin isa’s within 14 days from your deposit and their penalty’s for leaving

are lower than other isa’s.

You could get 5.55% via Virgin 3 year isa.

120 interest penalty £364.93.

Or 2 year 5.5% 90 day penalty £271.23 or 1 year 5.45% 60 day penalty £268.76.

A cheap way to get your 20k back in a hurry.

1 -

movingforward2010 said:I earn £24000 a year. My tax code is 1257C.

I’m 41 years old. Single

I’ve got £33500 in savings in an instant access savings account at 4.36% (saving for mortgage deposit)

Do I need to put £20000 of this in an ISA so I don’t pay tax?

I’ve just renewed my ISA with Lloyds bank. ( it only has £100 in it) can I close this and move to a better paying rate one?

Presumably you mean C1257L and are Welsh resident for tax purposes.

If so then with £24k earnings you will be taxed at 0% on the first £1,000 of your interest and 20% on anything above that.

You need to decide if you can make more money overall with a normal account or an ISA.

There are some decent fixed rate ISA's at the moment which might be the best option.1 -

EthicsGradient said:If it may take more than a year to use the money for a deposit, then, yes, moving some to an ISA would be a good idea.

You're only allowed to pay into one cash ISA each tax year (ie April 6th to April 5th). When you say you've "renewed" the Lloyds one, do you just mean you agreed for it run for some further length of time, or did you pay any new cash into it? This could determine the order you do things next, and which other ISA to look for. It had £150.29 in it and then I clicked “renew savings account”.0

It had £150.29 in it and then I clicked “renew savings account”.0 -

OK, that looks like you've paid £119.59 into it in this tax year, because of "remaining allowance". That means you can either pay more money into the Lloyds one first, and then transfer the whole thing to a new ISA manager (you need one that accepts transfers-in - most do, but check), or you'll have to open the new one without immediately adding any new cash to it, get your Lloyds ISA transferred to it, and then you can add new cash to it (I've never done that myself, but it should be possible - see eg Nationwide saying "You can transfer an active cash ISA to a new manager. If you transfer your current-year ISA, we will tell your new ISA manager how much more you can pay in during the tax year").

Since your instant access account pays more than the Lloyds ISA (seems to be 3.2%), the latter would be better, I think. The new ISA manager will tell you how to get the transfer started.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards