We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Old loan and new loan

SwiftS

Posts: 30 Forumite

My daughter graduated in June 2022. She’s now thinking about applying for PGCE. I understand this is the only postgrad course which is funded as an undergrad course. So she would have three years of the old style 30 year repayment loan and one year of the 40 year loan. I’ve tried to look at how the repayments would be approached but I can’t find the answer. Will she be paying off both for 30 years and then pay the remainder of the ‘new’ loan for the extra years? Or is the initial loan prioritised for repayment. I’m concerned that if this was the case, then after 30 years paying the initial loan she’d have nearly all of the PGCE to pay for (at a time when she would be a potentially higher earner)

0

Comments

-

It's not the only one but that's not important. .In repayment 9% of earning above the relevant threshold is taken as repayment, even with multiple Plan Type loans. If only one threshold is reached then all repayments go towards that loan.If both thresholds are reached then any repayments for earnings above the higher threshold are shared equally between both loans..If the plan 2 loan is paid in full or cancelled after 30 years then any repayments after this time will all go towards the plan 5 loan, if they still have one, until it's paid off or 40 years pass since it's repayment start date.1

-

This bit's wrong.kaMelo said:It's not the only one but that's not important. .In repayment 9% of earning above the relevant threshold is taken as repayment, even with multiple Plan Type loans. If only one threshold is reached then all repayments go towards that loan.If both thresholds are reached then any repayments for earnings above the higher threshold are shared equally between both loans.If the plan 2 loan is paid in full or cancelled after 30 years then any repayments after this time will all go towards the plan 5 loan, if they still have one, until it's paid off or 40 years pass since it's repayment start date.

Once you reach a threshold for a particular plan type then all repayments from earnings above that threshold go to that plan type, until a higher threshold is reached for a different plan type.

Example 1

If you have a Plan 2 and a Plan 5 loan that are both in repayment (note Plan 5 can't enter repayment until April 2026 at the earliest), and you earn £30,000 then:

• 9% of income between £25,000 (Plan 5 threshold) and £27,295 (Plan 2 threshold) goes to the Plan 5 loan, and

• 9% of income over £27,295 (Plan 2 threshold) goes to the Plan 2 loan.

Example 2

If you have a Plan 1, Plan 2 and a Plan 5 loan that are all in repayment (note Plan 5 can't enter repayment until April 2026 at the earliest), and you earn £30,000 then:

• 9% of income between £22,015 (Plan 1 threshold) and £25,000 (Plan 5 threshold) goes to the Plan 1 loan,

• 9% of income between £25,000 (Plan 5 threshold) and £27,295 (Plan 2 threshold) goes to the Plan 5 loan, and

• 9% of income over £27,295 (Plan 2 threshold) goes to the Plan 2 loan.

2 -

It's going to be interesting if the thresholds are ever identical or one "overtakes" another!Ed-1 said:

This bit's wrong.kaMelo said:It's not the only one but that's not important. .In repayment 9% of earning above the relevant threshold is taken as repayment, even with multiple Plan Type loans. If only one threshold is reached then all repayments go towards that loan.If both thresholds are reached then any repayments for earnings above the higher threshold are shared equally between both loans.If the plan 2 loan is paid in full or cancelled after 30 years then any repayments after this time will all go towards the plan 5 loan, if they still have one, until it's paid off or 40 years pass since it's repayment start date.

Once you reach a threshold for a particular plan type then all repayments from earnings above that threshold go to that plan type, until a higher threshold is reached for a different plan type.

Example 1

If you have a Plan 2 and a Plan 5 loan that are both in repayment (note Plan 5 can't enter repayment until April 2026 at the earliest), and you earn £30,000 then:

• 9% of income between £25,000 (Plan 5 threshold) and £27,295 (Plan 2 threshold) goes to the Plan 5 loan, and

• 9% of income over £27,295 (Plan 2 threshold) goes to the Plan 2 loan.

Example 2

If you have a Plan 1, Plan 2 and a Plan 5 loan that are all in repayment (note Plan 5 can't enter repayment until April 2026 at the earliest), and you earn £30,000 then:

• 9% of income between £22,015 (Plan 1 threshold) and £25,000 (Plan 5 threshold) goes to the Plan 1 loan,

• 9% of income between £25,000 (Plan 5 threshold) and £27,295 (Plan 2 threshold) goes to the Plan 5 loan, and

• 9% of income over £27,295 (Plan 2 threshold) goes to the Plan 2 loan.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.1 -

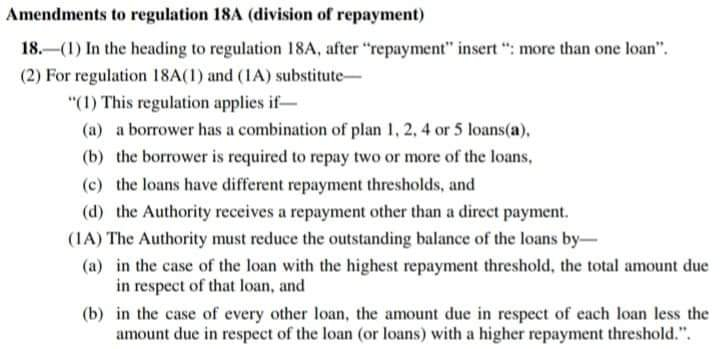

It's already happened this year when Plan 4 overtook Plan 2 and the regulations had to be amended (point 2.2(2)):silvercar said:

It's going to be interesting if the thresholds are ever identical or one "overtakes" another!Ed-1 said:

This bit's wrong.kaMelo said:It's not the only one but that's not important. .In repayment 9% of earning above the relevant threshold is taken as repayment, even with multiple Plan Type loans. If only one threshold is reached then all repayments go towards that loan.If both thresholds are reached then any repayments for earnings above the higher threshold are shared equally between both loans.If the plan 2 loan is paid in full or cancelled after 30 years then any repayments after this time will all go towards the plan 5 loan, if they still have one, until it's paid off or 40 years pass since it's repayment start date.

Once you reach a threshold for a particular plan type then all repayments from earnings above that threshold go to that plan type, until a higher threshold is reached for a different plan type.

Example 1

If you have a Plan 2 and a Plan 5 loan that are both in repayment (note Plan 5 can't enter repayment until April 2026 at the earliest), and you earn £30,000 then:

• 9% of income between £25,000 (Plan 5 threshold) and £27,295 (Plan 2 threshold) goes to the Plan 5 loan, and

• 9% of income over £27,295 (Plan 2 threshold) goes to the Plan 2 loan.

Example 2

If you have a Plan 1, Plan 2 and a Plan 5 loan that are all in repayment (note Plan 5 can't enter repayment until April 2026 at the earliest), and you earn £30,000 then:

• 9% of income between £22,015 (Plan 1 threshold) and £25,000 (Plan 5 threshold) goes to the Plan 1 loan,

• 9% of income between £25,000 (Plan 5 threshold) and £27,295 (Plan 2 threshold) goes to the Plan 5 loan, and

• 9% of income over £27,295 (Plan 2 threshold) goes to the Plan 2 loan.

3 -

I'm sure I read somewhere the payments were shared but happy to be corrected, I must be thinking of something else.1

-

I wasn't questioning, I had absolutely no doubt that you were correct and I was not.

As you say, the legislation is clear.

It has got me thinking on what it was I read and what it related to, whether I did actually read something or did I simply just imagine it.0 -

Seems unethical to me, for payments to be assigned by thresholds. You should be allowed to assign payments to the loan with the highest interest rate.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.0

-

Thanks for the responses. Really helpful. It was not easy to find the answer when I searched. Students completing their degrees on plan 2 and now having to fund pgce on plan 5 are going to be paying student loans for prettyEd-1 said:

The regulations are conclusive:kaMelo said:I'm sure I read somewhere the payments were shared but happy to be corrected, I must be thinking of something else.

much their whole career. My daughter graduated in June 2022, but wanted to get some experience in a school first before applying to do PGCE (to make sure it was the right choice for her etc). This has been a potentially costly mistake as she could have been doing PGCE this year on plan 2 🥺.

So if I have this right…

plan 2 payments 2023-2053 (not paying anything at the minute because salaries in education are so abysmal)

If she starts pgce in 2024, then plan 5 payments will start April 2026 and continue to 2066. She’ll be 65.

If she starts work as a teacher in September 2025, there will be 6 months or so of just paying plan 2.

April 2026 plan 5 kicks in as well, but she will only be making a tiny contribution to this (9% of salary between £25-£27k). Bulk of repayment goes to plan 2 (9% over £27k).This continues for 27 years (or so, my

maths is muddled now!)

By April 2053 the remainder of plan 2 is written off, but now the payments shift to plan 5 only. Despite paying both loans for 27 years she will have only made a tiny dent in the plan 5 loan.She now pays 9% of her salary over £25k for the next 13 years until the age of 65 in 2066.

I suspect students will turn to routes other than PGCE. Alternatives in our area are a bit limited though.

Depressing options for young people 🥺0 -

Your calculation looks right, other than the last sentence should be the next 33 not 13 years.SwiftS said:

Thanks for the responses. Really helpful. It was not easy to find the answer when I searched. Students completing their degrees on plan 2 and now having to fund pgce on plan 5 are going to be paying student loans for prettyEd-1 said:

The regulations are conclusive:kaMelo said:I'm sure I read somewhere the payments were shared but happy to be corrected, I must be thinking of something else.

much their whole career. My daughter graduated in June 2022, but wanted to get some experience in a school first before applying to do PGCE (to make sure it was the right choice for her etc). This has been a potentially costly mistake as she could have been doing PGCE this year on plan 2 🥺.

So if I have this right…

plan 2 payments 2023-2053 (not paying anything at the minute because salaries in education are so abysmal)

If she starts pgce in 2024, then plan 5 payments will start April 2026 and continue to 2066. She’ll be 65.

If she starts work as a teacher in September 2025, there will be 6 months or so of just paying plan 2.

April 2026 plan 5 kicks in as well, but she will only be making a tiny contribution to this (9% of salary between £25-£27k). Bulk of repayment goes to plan 2 (9% over £27k).This continues for 27 years (or so, my

maths is muddled now!)

By April 2053 the remainder of plan 2 is written off, but now the payments shift to plan 5 only. Despite paying both loans for 27 years she will have only made a tiny dent in the plan 5 loan.She now pays 9% of her salary over £25k for the next 13 years until the age of 65 in 2066.

I suspect students will turn to routes other than PGCE. Alternatives in our area are a bit limited though.

Depressing options for young people 🥺

Of course a few years of high inflation will lead to wage rises, this in turn could lead to more students paying off their loan sooner.I'm a Forum Ambassador on the housing, mortgages & student money saving boards. I volunteer to help get your forum questions answered and keep the forum running smoothly. Forum Ambassadors are not moderators and don't read every post. If you spot an illegal or inappropriate post then please report it to forumteam@moneysavingexpert.com (it's not part of my role to deal with this). Any views are mine and not the official line of MoneySavingExpert.com.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.9K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards