We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

We're aware that some users are currently experiencing errors on the Forum. Our tech team is working to resolve the issue. Thanks for your patience.

To transfer or not to transfer , IFA’s differ in opinion.

GoldenOldy

Posts: 245 Forumite

Good Morning.

I am seeking advice and opinion on behalf on my nephews wife if thats possible. The issue is puzzling both him and her.

She is now 60 and is unsure when she will retire, as she has a nice part time job and quite a bit of savings , which help pay the bills etc

There is no saying how long the job will last however, and although they could just manage without her part time earnings while these savings rates are high.

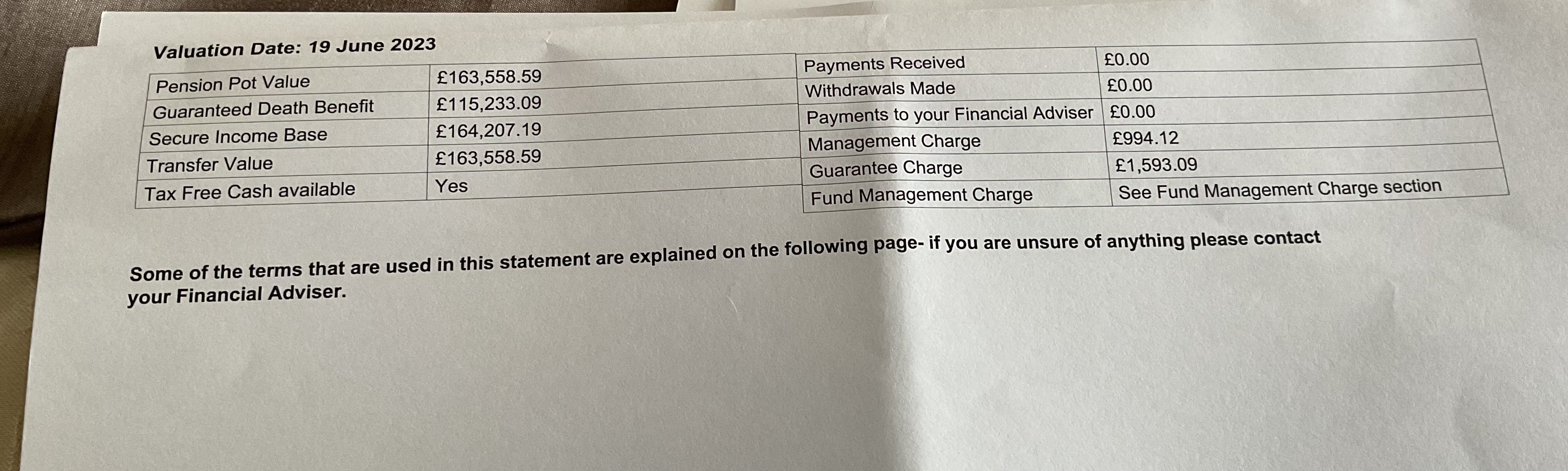

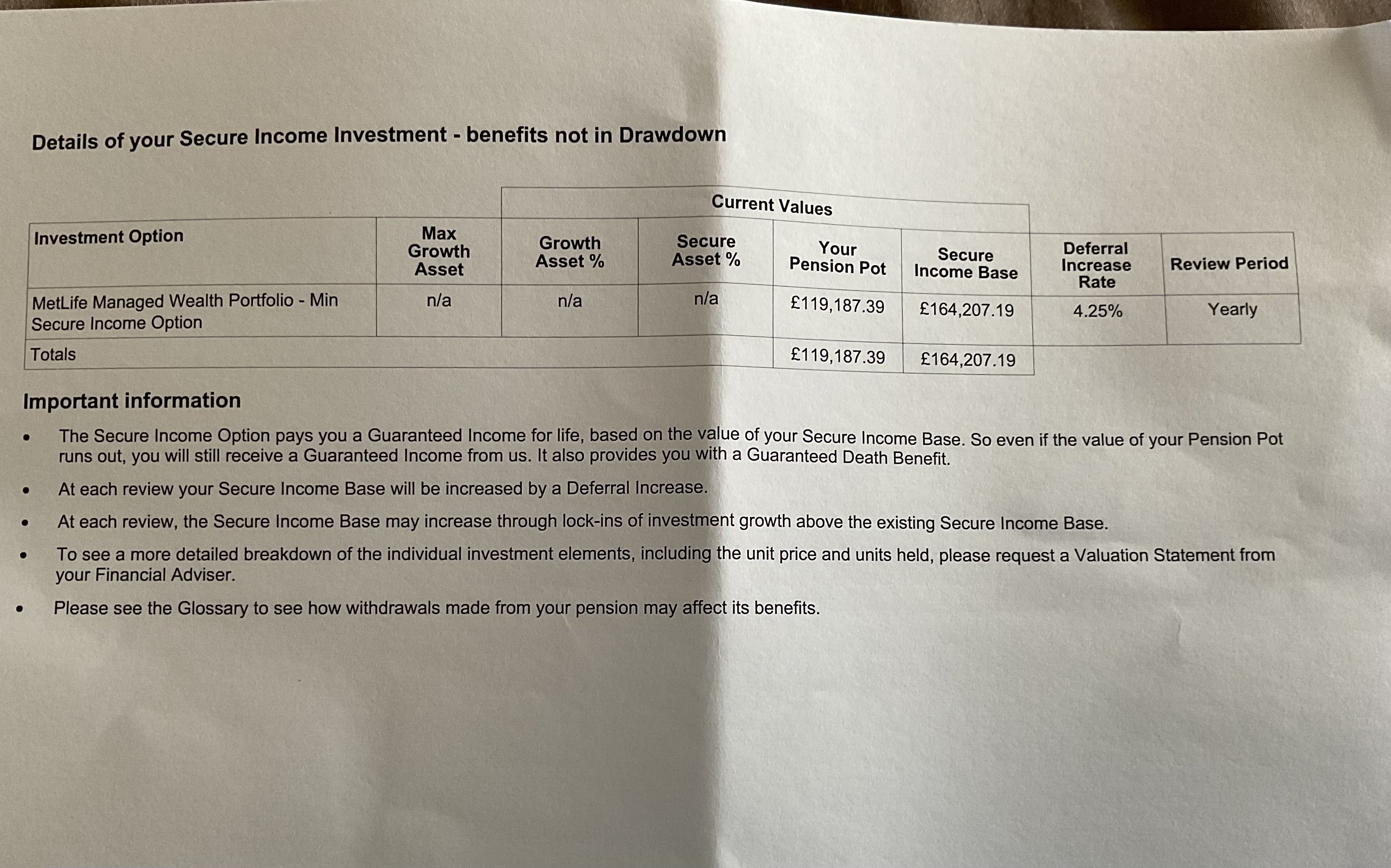

We looked at her pension statement with Metlife , and it has a pension pot of 163,000, which is also referred to as a ‘secure income base’.

It has all sorts of bells n whistles on it, which she doesnt need …it was set up before pension freedoms etc

Anyway ,its made a measly 3.8 per cent before charges £1593 guarantee charge, and 994 management charge.

I am seeking advice and opinion on behalf on my nephews wife if thats possible. The issue is puzzling both him and her.

She is now 60 and is unsure when she will retire, as she has a nice part time job and quite a bit of savings , which help pay the bills etc

There is no saying how long the job will last however, and although they could just manage without her part time earnings while these savings rates are high.

We looked at her pension statement with Metlife , and it has a pension pot of 163,000, which is also referred to as a ‘secure income base’.

It has all sorts of bells n whistles on it, which she doesnt need …it was set up before pension freedoms etc

Anyway ,its made a measly 3.8 per cent before charges £1593 guarantee charge, and 994 management charge.

She is pretty risk averse, and quite anxious about money, having experienced real poverty growing up which she has never quite overcome.

She has seen 2 ifa’s , one who said leave it where it is (although she really hates it,) and one who said put it into a low risk fund for a few years.

As she is getting now 5 pc on her savings , she is wondering whether it would be better just to put this is a sipp in a cash deposit or something as at least then she has the control.

Any thoughts?

As she is getting now 5 pc on her savings , she is wondering whether it would be better just to put this is a sipp in a cash deposit or something as at least then she has the control.

Any thoughts?

0

Comments

-

"Secure income base" sounds like a defined benefit pension - if that's the case then she'll probably struggle to move it. Does it say anything about the annual/monthly pension pay out & index linking? Cash deposits/savings feel secure / more certain... but their value gets eroded by inflation.

Is she continuing to contribute to it? does it get employer contributions?

It would probably be best if you got your nephew / his wife to post on here for advice though.2 -

Can you clarify what you mean by "bells and whistles" - do you mean that it has guaranteed or protected benefits in it?1

-

Hates what, exactly? Without knowing that, it's rather hard to understand what she's got that she doesn't like and what she thinks might be something she would like.GoldenOldy said:She has seen 2 ifa’s , one who said leave it where it is (although she really hates it,) and one who said put it into a low risk fund for a few years.

Why pay for advice from 2 IFAs? The likelihood of getting identical answers to all questions is pretty slim, so all she's doing is laying out cash to confuse herself!

Asking for opinions here probably won't help her either, given we have virtually no information on which to base those opinions. Both IFAs should have given her reasons for their recommendations, so perhaps going back and looking at those, then deciding what she herself wants to do on an informed basis, might be the most sensible way to proceed.Googling on your question might have been both quicker and easier, if you're only after simple facts rather than opinions!2 -

Thankyou for your answers so far.

Just to clarify, she doesnt pay in or get employers contributions.

She is thinking of retiring at age 65 latest although senses her job could finish any moment now, but they could manage until 65 anyway on her savings just, if thats what is required.

She hates the pension due to ‘lack of control’ and the ‘surprise factor ‘ every year , and due to her ‘condition’ . I believe its regarded as ‘neuro diverse’ hence seeking help from different sources.

She asked me to post on her behalf, as I mentioned this site and how useful its been in the past.

I shall send some pictures of the info she left with me yesterday which may or may not help, I have just called for her consent.

0 -

I can't see the "surprise factor" she's worried about.GoldenOldy said:Thankyou for your answers so far.

Just to clarify, she doesnt pay in or get employers contributions.

She is thinking of retiring at age 65 latest although senses her job could finish any moment now, but they could manage until 65 anyway on her savings just, if thats what is required.

She hates the pension due to ‘lack of control’ and the ‘surprise factor ‘ every year , and due to her ‘condition’ . I believe its regarded as ‘neuro diverse’ hence seeking help from different sources.

She asked me to post on her behalf, as I mentioned this site and how useful its been in the past.

I shall send some pictures of the info she left with me yesterday which may or may not help, I have just called for her consent.

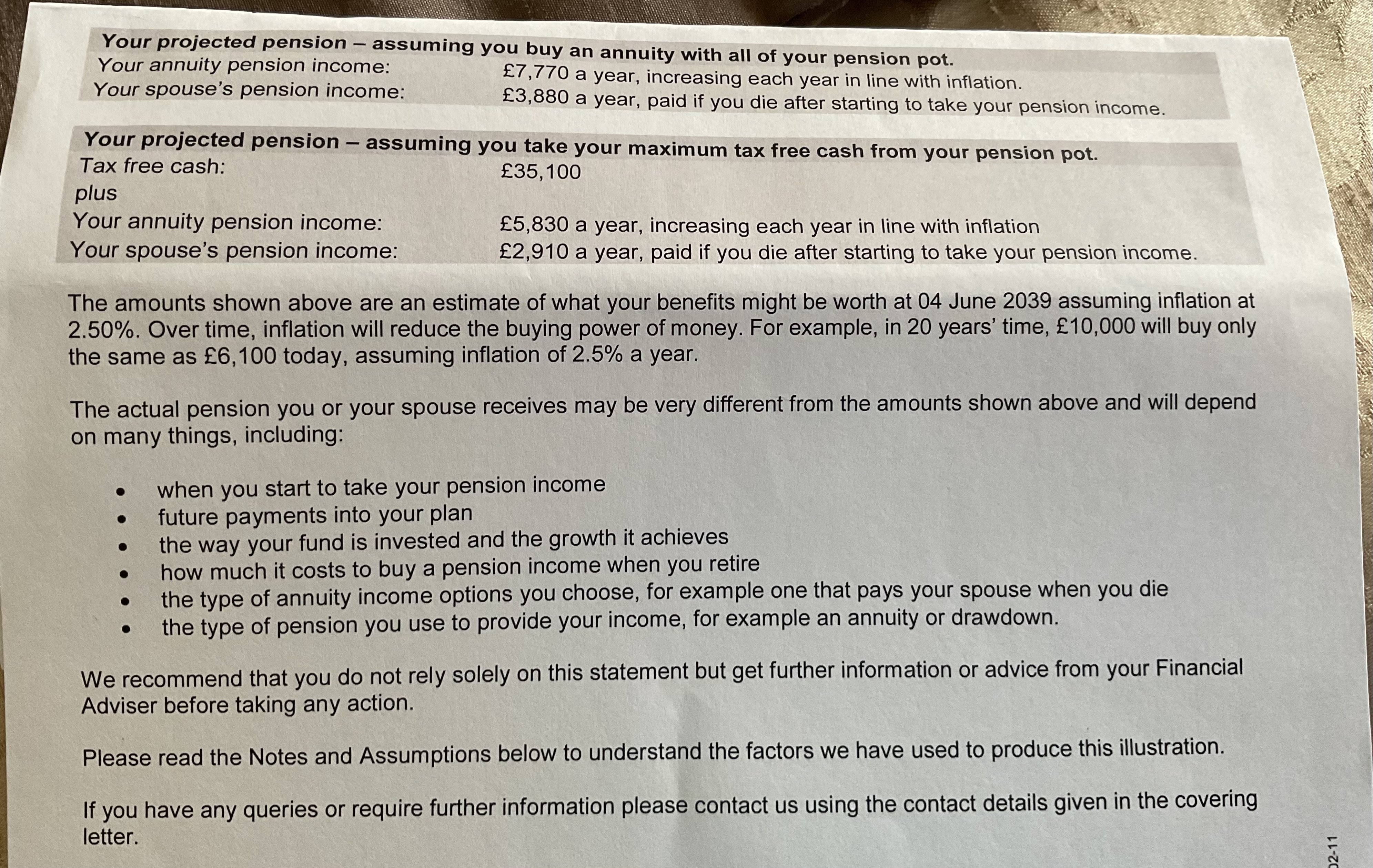

The pension pays a fixed amount each year (presumably in equal monthly payments) and the amount paid, rises with inflation so the payments maintain their buying power.

The only difference is if she takes a lump sum, or not.

0 -

I'm afraid I'm not familiar with this "secure income option is" but I am sure there are others on this forum who know about this who will reply in due course. From the terms used on those documents I would suspect that this pension has some kind of guaranteed benefits in it, which means that she would be obliged to take financial advice (at her cost) before being able to transfer it out to another provider. If that is the advice she has already received, and it was proper paid advice on that basis to transfer out, she may already have what she needs. Needs some others who are more expert in this area to comment further...1

-

Thanks both. The surprise factor id unlike her savings this fund increases and decreases each year which bothers her when its so low risk.0

-

She also thinks she is paying rather a lot for a guarantee.0

-

We looked at her pension statement with Metlife , and it has a pension pot of 163,000, which is also referred to as a ‘secure income base’.Its a horrible product. (in my opinion). It does have some downside protection but is invested in a way that leaves it less likely to grow and has a drag of high charges on it.She has seen 2 ifa’s , one who said leave it where it is (although she really hates it,) and one who said put it into a low risk fund for a few years.Investing is largely about opinion. With over 30,000 different options and an infinite combination available, you will get varying opinions.As she is getting now 5 pc on her savings , she is wondering whether it would be better just to put this is a sipp in a cash deposit or something as at least then she has the control.Insufficient information to go on. It will largely depend on the options selected on the metlife plan, which version it was (as it was tweaked over the years), the charges and any contractual benefits and the costs of getting out. i.e. it needs a proper analysis and not a quick and dirty opinion based on little or no facts.

Have both of these IFAs given paid advice or just quick and dirty responses?

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

Hello Dunstonh. Thankyou. She has received free introductory advice from both. I believe there are no costs for getting out as the transfer value is the same amount as the fund value. It was taken out just before pension freedoms happened, think 2015.dunstonh said:We looked at her pension statement with Metlife , and it has a pension pot of 163,000, which is also referred to as a ‘secure income base’.Its a horrible product. (in my opinion). It does have some downside protection but is invested in a way that leaves it less likely to grow and has a drag of high charges on it.She has seen 2 ifa’s , one who said leave it where it is (although she really hates it,) and one who said put it into a low risk fund for a few years.Investing is largely about opinion. With over 30,000 different options and an infinite combination available, you will get varying opinions.As she is getting now 5 pc on her savings , she is wondering whether it would be better just to put this is a sipp in a cash deposit or something as at least then she has the control.Insufficient information to go on. It will largely depend on the options selected on the metlife plan, which version it was (as it was tweaked over the years), the charges and any contractual benefits and the costs of getting out. i.e. it needs a proper analysis and not a quick and dirty opinion based on little or no facts.

Have both of these IFAs given paid advice or just quick and dirty responses?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards