We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Private Pension Lifestyling investments - the next scandal?

Comments

-

I suppose the big risk with that strategy is if there is a big market crash wiping out massive percentages off your fund and if there is still sufficient remaining plus any cash savings whilst you wait for the markets to recover which could take a few years.Pat38493 said:

I’m still researching all this but from my opinion so far, the two big problems that can arise with these lifestyle or target retirement funds is that they start to move you more into bonds too early, sometimes 10 years before retirement which is way to early if you are planning drawdown, and secondly they even carry on increasing your bond share after you have retired.Rich1976 said:

Well the provider is Standard Life and upon checking earlier there are over 300 funds I could choose from . Only about a dozen have charges below 1% which are mostly variations of the Multi Asset Lifestyle funds.Pat38493 said:

It may be that your employer is with a provider who only offers a small choice of funds. You can certainly get tracker funds for a lot less than 1% - for example Vanguard has them at 0.22% and HSBS at 0.19% and you can get lesser than that as well.Rich1976 said:

i started off being in tracker funds which are mainly ones by Blackrock rather than standard life’s own ones. They were all 0.98% plus transactional charges of about 0.05% on top.dunstonh said:so really Lifestyling can’t be that bad surely. The fees tend to be reasonable ( and certainly with my work pension are cheaper than tracker funds which are all about 1% compared to 0.65 for the lifestyle fund )Are you sure about the cost? Normally, the internal/in-house funds are within the auto-enrolment 0.75% cap.

so then I changed to the Lifestyle fund.

but even looking on my online account this morning , the lifestyle funds are still the cheapest, there is nothing available for lower or the same charges.

However if your employer has locked you into a small range of choices, your only other option is to see if your employer provider allows partial transfers out - you could then transfer the money to a SIPP with a much larger choice.

The other option you have is to be in the lifestyle fund but change your retirement date to 75 or whatever so that the lifestyling does not kick in. As discussed above lifestyling is not necessarily bad, but it’s quite often a bit over conservative to deliver the best long term results for clued up investors.Thankfully I have had a Sipp running for years which has over 25 years of contributions from previous employers as well as my own contributions .

standard life do not allow partial transfers as I phoned and asked last year.

in itself the multi asset fund does seem quite good having grown over 8% in the last 12 months and the derisking isn’t as as dramatic as some others I have seen from other providers.

From the research I’ve read, you are arguably better off moving into a bigger share of bonds only a few years before retirement or even at retirement, and then over the 10 years after retirement slowly raise your equities back up again to 90 or 100%.

Therefore even if you don’t have much ability to control it before retirement, you can certainly transfer out as soon as you are no longer an employee and take control of your situation (and also take advantage of much lower DIY platform and fund charges if you are willing to do a bit of research and reading up on it).0 -

That’s the reason why you would reduce your risk around retirement and for about 10 years after that. A crash in the first 5-10 years is your worst risk.Rich1976 said:

I suppose the big risk with that strategy is if there is a big market crash wiping out massive percentages off your fund and if there is still sufficient remaining plus any cash savings whilst you wait for the markets to recover which could take a few years.Pat38493 said:

I’m still researching all this but from my opinion so far, the two big problems that can arise with these lifestyle or target retirement funds is that they start to move you more into bonds too early, sometimes 10 years before retirement which is way to early if you are planning drawdown, and secondly they even carry on increasing your bond share after you have retired.Rich1976 said:

Well the provider is Standard Life and upon checking earlier there are over 300 funds I could choose from . Only about a dozen have charges below 1% which are mostly variations of the Multi Asset Lifestyle funds.Pat38493 said:

It may be that your employer is with a provider who only offers a small choice of funds. You can certainly get tracker funds for a lot less than 1% - for example Vanguard has them at 0.22% and HSBS at 0.19% and you can get lesser than that as well.Rich1976 said:

i started off being in tracker funds which are mainly ones by Blackrock rather than standard life’s own ones. They were all 0.98% plus transactional charges of about 0.05% on top.dunstonh said:so really Lifestyling can’t be that bad surely. The fees tend to be reasonable ( and certainly with my work pension are cheaper than tracker funds which are all about 1% compared to 0.65 for the lifestyle fund )Are you sure about the cost? Normally, the internal/in-house funds are within the auto-enrolment 0.75% cap.

so then I changed to the Lifestyle fund.

but even looking on my online account this morning , the lifestyle funds are still the cheapest, there is nothing available for lower or the same charges.

However if your employer has locked you into a small range of choices, your only other option is to see if your employer provider allows partial transfers out - you could then transfer the money to a SIPP with a much larger choice.

The other option you have is to be in the lifestyle fund but change your retirement date to 75 or whatever so that the lifestyling does not kick in. As discussed above lifestyling is not necessarily bad, but it’s quite often a bit over conservative to deliver the best long term results for clued up investors.Thankfully I have had a Sipp running for years which has over 25 years of contributions from previous employers as well as my own contributions .

standard life do not allow partial transfers as I phoned and asked last year.

in itself the multi asset fund does seem quite good having grown over 8% in the last 12 months and the derisking isn’t as as dramatic as some others I have seen from other providers.

From the research I’ve read, you are arguably better off moving into a bigger share of bonds only a few years before retirement or even at retirement, and then over the 10 years after retirement slowly raise your equities back up again to 90 or 100%.

Therefore even if you don’t have much ability to control it before retirement, you can certainly transfer out as soon as you are no longer an employee and take control of your situation (and also take advantage of much lower DIY platform and fund charges if you are willing to do a bit of research and reading up on it).

You need to do some research around safe withdrawal rates and all the work that’s been done around it.

These kind of strategies would have worked even if you retired at the worst point of the 1920s or 1970s so in the end it depends whether you think we will see worse than that going forward.

0 -

Another big risk is that you need the nerve/stomach to follow it through. Most 70/75 year old people would not be sleeping very well during a market crash if they were that heavily invested in equities.Rich1976 said:

I suppose the big risk with that strategy is if there is a big market crash wiping out massive percentages off your fund and if there is still sufficient remaining plus any cash savings whilst you wait for the markets to recover which could take a few years.Pat38493 said:

I’m still researching all this but from my opinion so far, the two big problems that can arise with these lifestyle or target retirement funds is that they start to move you more into bonds too early, sometimes 10 years before retirement which is way to early if you are planning drawdown, and secondly they even carry on increasing your bond share after you have retired.Rich1976 said:

Well the provider is Standard Life and upon checking earlier there are over 300 funds I could choose from . Only about a dozen have charges below 1% which are mostly variations of the Multi Asset Lifestyle funds.Pat38493 said:

It may be that your employer is with a provider who only offers a small choice of funds. You can certainly get tracker funds for a lot less than 1% - for example Vanguard has them at 0.22% and HSBS at 0.19% and you can get lesser than that as well.Rich1976 said:

i started off being in tracker funds which are mainly ones by Blackrock rather than standard life’s own ones. They were all 0.98% plus transactional charges of about 0.05% on top.dunstonh said:so really Lifestyling can’t be that bad surely. The fees tend to be reasonable ( and certainly with my work pension are cheaper than tracker funds which are all about 1% compared to 0.65 for the lifestyle fund )Are you sure about the cost? Normally, the internal/in-house funds are within the auto-enrolment 0.75% cap.

so then I changed to the Lifestyle fund.

but even looking on my online account this morning , the lifestyle funds are still the cheapest, there is nothing available for lower or the same charges.

However if your employer has locked you into a small range of choices, your only other option is to see if your employer provider allows partial transfers out - you could then transfer the money to a SIPP with a much larger choice.

The other option you have is to be in the lifestyle fund but change your retirement date to 75 or whatever so that the lifestyling does not kick in. As discussed above lifestyling is not necessarily bad, but it’s quite often a bit over conservative to deliver the best long term results for clued up investors.Thankfully I have had a Sipp running for years which has over 25 years of contributions from previous employers as well as my own contributions .

standard life do not allow partial transfers as I phoned and asked last year.

in itself the multi asset fund does seem quite good having grown over 8% in the last 12 months and the derisking isn’t as as dramatic as some others I have seen from other providers.

From the research I’ve read, you are arguably better off moving into a bigger share of bonds only a few years before retirement or even at retirement, and then over the 10 years after retirement slowly raise your equities back up again to 90 or 100%.

Therefore even if you don’t have much ability to control it before retirement, you can certainly transfer out as soon as you are no longer an employee and take control of your situation (and also take advantage of much lower DIY platform and fund charges if you are willing to do a bit of research and reading up on it).0 -

Just for fun, here are the first twenty years of a UK retirement starting in 1973 with an allocation of 90% to UK stocks and 10% to cash with an inflation adjusted withdrawal of 4% (data from macrohistory.net). Top panel is portfolio value (expressed in real terms as a percentage of the initial portfolio value), the rather dull bottom panel is real withdrawal.Albermarle said:

Another big risk is that you need the nerve/stomach to follow it through. Most 70/75 year old people would not be sleeping very well during a market crash if they were that heavily invested in equities.Rich1976 said:

I suppose the big risk with that strategy is if there is a big market crash wiping out massive percentages off your fund and if there is still sufficient remaining plus any cash savings whilst you wait for the markets to recover which could take a few years.Pat38493 said:

I’m still researching all this but from my opinion so far, the two big problems that can arise with these lifestyle or target retirement funds is that they start to move you more into bonds too early, sometimes 10 years before retirement which is way to early if you are planning drawdown, and secondly they even carry on increasing your bond share after you have retired.Rich1976 said:

Well the provider is Standard Life and upon checking earlier there are over 300 funds I could choose from . Only about a dozen have charges below 1% which are mostly variations of the Multi Asset Lifestyle funds.Pat38493 said:

It may be that your employer is with a provider who only offers a small choice of funds. You can certainly get tracker funds for a lot less than 1% - for example Vanguard has them at 0.22% and HSBS at 0.19% and you can get lesser than that as well.Rich1976 said:

i started off being in tracker funds which are mainly ones by Blackrock rather than standard life’s own ones. They were all 0.98% plus transactional charges of about 0.05% on top.dunstonh said:so really Lifestyling can’t be that bad surely. The fees tend to be reasonable ( and certainly with my work pension are cheaper than tracker funds which are all about 1% compared to 0.65 for the lifestyle fund )Are you sure about the cost? Normally, the internal/in-house funds are within the auto-enrolment 0.75% cap.

so then I changed to the Lifestyle fund.

but even looking on my online account this morning , the lifestyle funds are still the cheapest, there is nothing available for lower or the same charges.

However if your employer has locked you into a small range of choices, your only other option is to see if your employer provider allows partial transfers out - you could then transfer the money to a SIPP with a much larger choice.

The other option you have is to be in the lifestyle fund but change your retirement date to 75 or whatever so that the lifestyling does not kick in. As discussed above lifestyling is not necessarily bad, but it’s quite often a bit over conservative to deliver the best long term results for clued up investors.Thankfully I have had a Sipp running for years which has over 25 years of contributions from previous employers as well as my own contributions .

standard life do not allow partial transfers as I phoned and asked last year.

in itself the multi asset fund does seem quite good having grown over 8% in the last 12 months and the derisking isn’t as as dramatic as some others I have seen from other providers.

From the research I’ve read, you are arguably better off moving into a bigger share of bonds only a few years before retirement or even at retirement, and then over the 10 years after retirement slowly raise your equities back up again to 90 or 100%.

Therefore even if you don’t have much ability to control it before retirement, you can certainly transfer out as soon as you are no longer an employee and take control of your situation (and also take advantage of much lower DIY platform and fund charges if you are willing to do a bit of research and reading up on it).

I don't know about anyone else, but I would have been fairly perturbed after the first two years and not much happier at the end of the 70s (the 1990s were better - the portfolio recovered to 80% of the initial value by 2000 and the portfolio didn't run out of money even after 45 years).

3 -

mind you, the first few years are still quite scary even with 50% stocks and 50% cash.

1 -

Two posts before are very helpful and easy to understand.OldScientist said:mind you, the first few years are still quite scary even with 50% stocks and 50% cash.

Just wondering if poss OldScientist could do two more posts years 1975 till 1995 would be so interesting to see please?

0 -

This is another problem I have with swr - a lot of the scenarios that turn out to be safe see withdrawals reaching >20% of the portfolio (portfolio only covers 5 years of withdrawals) within the first decade. Who on earth is going to hold their nerve in such a scenario?OldScientist said:

Just for fun, here are the first twenty years of a UK retirement starting in 1973 with an allocation of 90% to UK stocks and 10% to cash with an inflation adjusted withdrawal of 4% (data from macrohistory.net). Top panel is portfolio value (expressed in real terms as a percentage of the initial portfolio value), the rather dull bottom panel is real withdrawal.Albermarle said:

Another big risk is that you need the nerve/stomach to follow it through. Most 70/75 year old people would not be sleeping very well during a market crash if they were that heavily invested in equities.Rich1976 said:

I suppose the big risk with that strategy is if there is a big market crash wiping out massive percentages off your fund and if there is still sufficient remaining plus any cash savings whilst you wait for the markets to recover which could take a few years.Pat38493 said:

I’m still researching all this but from my opinion so far, the two big problems that can arise with these lifestyle or target retirement funds is that they start to move you more into bonds too early, sometimes 10 years before retirement which is way to early if you are planning drawdown, and secondly they even carry on increasing your bond share after you have retired.Rich1976 said:

Well the provider is Standard Life and upon checking earlier there are over 300 funds I could choose from . Only about a dozen have charges below 1% which are mostly variations of the Multi Asset Lifestyle funds.Pat38493 said:

It may be that your employer is with a provider who only offers a small choice of funds. You can certainly get tracker funds for a lot less than 1% - for example Vanguard has them at 0.22% and HSBS at 0.19% and you can get lesser than that as well.Rich1976 said:

i started off being in tracker funds which are mainly ones by Blackrock rather than standard life’s own ones. They were all 0.98% plus transactional charges of about 0.05% on top.dunstonh said:so really Lifestyling can’t be that bad surely. The fees tend to be reasonable ( and certainly with my work pension are cheaper than tracker funds which are all about 1% compared to 0.65 for the lifestyle fund )Are you sure about the cost? Normally, the internal/in-house funds are within the auto-enrolment 0.75% cap.

so then I changed to the Lifestyle fund.

but even looking on my online account this morning , the lifestyle funds are still the cheapest, there is nothing available for lower or the same charges.

However if your employer has locked you into a small range of choices, your only other option is to see if your employer provider allows partial transfers out - you could then transfer the money to a SIPP with a much larger choice.

The other option you have is to be in the lifestyle fund but change your retirement date to 75 or whatever so that the lifestyling does not kick in. As discussed above lifestyling is not necessarily bad, but it’s quite often a bit over conservative to deliver the best long term results for clued up investors.Thankfully I have had a Sipp running for years which has over 25 years of contributions from previous employers as well as my own contributions .

standard life do not allow partial transfers as I phoned and asked last year.

in itself the multi asset fund does seem quite good having grown over 8% in the last 12 months and the derisking isn’t as as dramatic as some others I have seen from other providers.

From the research I’ve read, you are arguably better off moving into a bigger share of bonds only a few years before retirement or even at retirement, and then over the 10 years after retirement slowly raise your equities back up again to 90 or 100%.

Therefore even if you don’t have much ability to control it before retirement, you can certainly transfer out as soon as you are no longer an employee and take control of your situation (and also take advantage of much lower DIY platform and fund charges if you are willing to do a bit of research and reading up on it).

I don't know about anyone else, but I would have been fairly perturbed after the first two years and not much happier at the end of the 70s (the 1990s were better - the portfolio recovered to 80% of the initial value by 2000 and the portfolio didn't run out of money even after 45 years).I think....2 -

No problem... here's 50% stocks and 50% cash for a 1975 start - illustrating the difference between starting at the bottom of a decline or (as previously) starting at the top. Of course, the 1973 retiree who had delayed their retirement for 2 years until 1975 would have seen their portfolio fall in value (so the '4%' would have been a much smaller number of £).RogerPensionGuy said:

Two posts before are very helpful and easy to understand.OldScientist said:mind you, the first few years are still quite scary even with 50% stocks and 50% cash.

Just wondering if poss OldScientist could do two more posts years 1975 till 1995 would be so interesting to see please?

The following plot of the historical 30 year safe withdrawal rates (i.e. the minimum inflation adjusted withdrawal rate that led to no failures during 30 years) for the UK for different retirement start years at different stock levels (0, 25, 50, 75, and 100%) may be of interest. UK based assets and inflation, fixed income is allocated half to 15-20 year bonds and half to 3 month bills (i.e., a cash proxy). My own calculations with asset returns drawn from Revision 6 of the database at macrohistory.net and no fees or taxes.

Poor performance in the early 20th century was down to high inflation towards the end of WWI (20% or so), while poor performance in 1930s caused by WWII, a stock market crash in 1937, and, for bonds, dreadful real performance post-WWII.

A few other things to note:

1) The SWR could be highly variable from year-to-year

2) Higher stock allocations tended to result in higher SWR (mainly down to poor bond performance)

3) SWR for a given retirement was only known at the end of the 30 year period (in other words, at the start of retirement the retiree would have no real idea).

Apologies to the OP - while this is not lifestyling, it probably does illustrate that the timing of retirement (luck/fate or whatever you want to call it) has often been more important than the precise asset allocation (although using stock allocations of 0% and 25% generally gave poor results). There are two good references on stock allocation glide paths that actually come to opposite conclusions:

Pfau, W. D., and Kitces M. E. (2014). “Reducing Retirement Risk with a Rising Equity Glide Path.” Journal of Financial Planning, 27, 38-48 who used Monte Carlo approximation to US asset returns and concluded that a rising stock allocation in retirement produced better results.Estrada, J. (2016). “The Retirement Glidepath: An International Perspective.” The Journal of Investing, 25 (2) 28-54; DOI: https://doi.org/10.3905/joi.2016.25.2.028 who looked at international historical data and concluded that declining glidepaths during retirement gave better outcomes (their final conclusion was actually that a fixed allocation was simple and probably good enough).

2 -

I think in reality it depends what you mean by holding nerve. In that scenario which seems to be a known outlier if you plot lots of years on the same chart, I would most likely reduce spending but I would not change my investment mix and sell at the bottom.michaels said:

This is another problem I have with swr - a lot of the scenarios that turn out to be safe see withdrawals reaching >20% of the portfolio (portfolio only covers 5 years of withdrawals) within the first decade. Who on earth is going to hold their nerve in such a scenario?OldScientist said:

Just for fun, here are the first twenty years of a UK retirement starting in 1973 with an allocation of 90% to UK stocks and 10% to cash with an inflation adjusted withdrawal of 4% (data from macrohistory.net). Top panel is portfolio value (expressed in real terms as a percentage of the initial portfolio value), the rather dull bottom panel is real withdrawal.Albermarle said:

Another big risk is that you need the nerve/stomach to follow it through. Most 70/75 year old people would not be sleeping very well during a market crash if they were that heavily invested in equities.Rich1976 said:

I suppose the big risk with that strategy is if there is a big market crash wiping out massive percentages off your fund and if there is still sufficient remaining plus any cash savings whilst you wait for the markets to recover which could take a few years.Pat38493 said:

I’m still researching all this but from my opinion so far, the two big problems that can arise with these lifestyle or target retirement funds is that they start to move you more into bonds too early, sometimes 10 years before retirement which is way to early if you are planning drawdown, and secondly they even carry on increasing your bond share after you have retired.Rich1976 said:

Well the provider is Standard Life and upon checking earlier there are over 300 funds I could choose from . Only about a dozen have charges below 1% which are mostly variations of the Multi Asset Lifestyle funds.Pat38493 said:

It may be that your employer is with a provider who only offers a small choice of funds. You can certainly get tracker funds for a lot less than 1% - for example Vanguard has them at 0.22% and HSBS at 0.19% and you can get lesser than that as well.Rich1976 said:

i started off being in tracker funds which are mainly ones by Blackrock rather than standard life’s own ones. They were all 0.98% plus transactional charges of about 0.05% on top.dunstonh said:so really Lifestyling can’t be that bad surely. The fees tend to be reasonable ( and certainly with my work pension are cheaper than tracker funds which are all about 1% compared to 0.65 for the lifestyle fund )Are you sure about the cost? Normally, the internal/in-house funds are within the auto-enrolment 0.75% cap.

so then I changed to the Lifestyle fund.

but even looking on my online account this morning , the lifestyle funds are still the cheapest, there is nothing available for lower or the same charges.

However if your employer has locked you into a small range of choices, your only other option is to see if your employer provider allows partial transfers out - you could then transfer the money to a SIPP with a much larger choice.

The other option you have is to be in the lifestyle fund but change your retirement date to 75 or whatever so that the lifestyling does not kick in. As discussed above lifestyling is not necessarily bad, but it’s quite often a bit over conservative to deliver the best long term results for clued up investors.Thankfully I have had a Sipp running for years which has over 25 years of contributions from previous employers as well as my own contributions .

standard life do not allow partial transfers as I phoned and asked last year.

in itself the multi asset fund does seem quite good having grown over 8% in the last 12 months and the derisking isn’t as as dramatic as some others I have seen from other providers.

From the research I’ve read, you are arguably better off moving into a bigger share of bonds only a few years before retirement or even at retirement, and then over the 10 years after retirement slowly raise your equities back up again to 90 or 100%.

Therefore even if you don’t have much ability to control it before retirement, you can certainly transfer out as soon as you are no longer an employee and take control of your situation (and also take advantage of much lower DIY platform and fund charges if you are willing to do a bit of research and reading up on it).

I don't know about anyone else, but I would have been fairly perturbed after the first two years and not much happier at the end of the 70s (the 1990s were better - the portfolio recovered to 80% of the initial value by 2000 and the portfolio didn't run out of money even after 45 years).

I suspect if you plot the same graphs over 40 or 45 years for an early retiree the equity one will catch up and overtake the 50/50 chart which might fail with much longer horizon.

In any case even if you foresaw 1973 and moved into cash at the top, you would then have got walloped by inflation later in the 1970s.

The prior proposal was to use a glide path increasing from 60% equity to 100% during approximately the first decade. You can’t really avoid seeing a terrifying early drop in some of those outlier scenarios. The simulations showed that this provided a slightly better outcome in most situations than any of the fixed balanced allocations.

In a way that’s the easy one. More worrying is the ones like I think around 1963 or so where it looks like you are doing great for 7-8 years and then…..

However I take the point that in the real world there are certainly situations when most of us would reduce spending to be on the safe side even if the data says it should be ok.1 -

The questions are thenPat38493 said:

I think in reality it depends what you mean by holding nerve. In that scenario which seems to be a known outlier if you plot lots of years on the same chart, I would most likely reduce spending but I would not change my investment mix and sell at the bottom.michaels said:

This is another problem I have with swr - a lot of the scenarios that turn out to be safe see withdrawals reaching >20% of the portfolio (portfolio only covers 5 years of withdrawals) within the first decade. Who on earth is going to hold their nerve in such a scenario?

I suspect if you plot the same graphs over 40 or 45 years for an early retiree the equity one will catch up and overtake the 50/50 chart which might fail with much longer horizon.

In any case even if you foresaw 1973 and moved into cash at the top, you would then have got walloped by inflation later in the 1970s.

The prior proposal was to use a glide path increasing from 60% equity to 100% during approximately the first decade. You can’t really avoid seeing a terrifying early drop in some of those outlier scenarios. The simulations showed that this provided a slightly better outcome in most situations than any of the fixed balanced allocations.

In a way that’s the easy one. More worrying is the ones like I think around 1963 or so where it looks like you are doing great for 7-8 years and then…..

However I take the point that in the real world there are certainly situations when most of us would reduce spending to be on the safe side even if the data says it should be ok.

a) When would you reduce spending?

b) By how much?

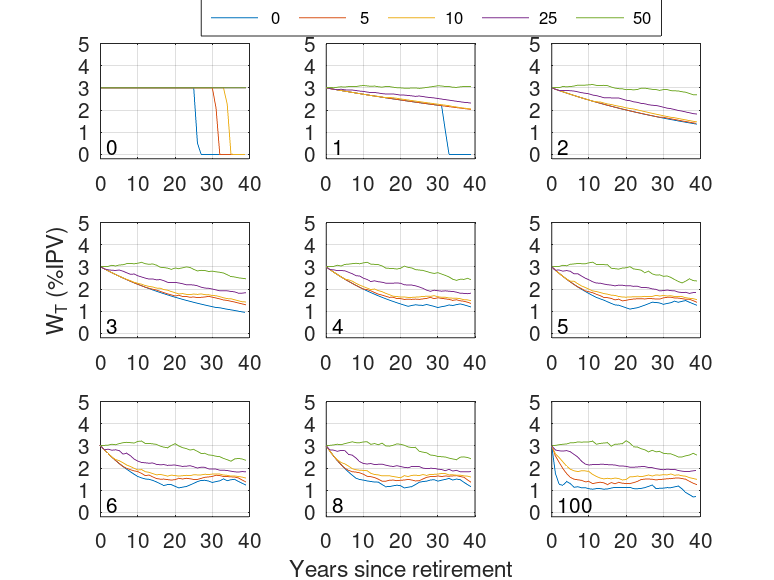

The following graphs are the real withdrawal as a function of time since retirement for various percentiles (0th is worst case, 50% is median) for a UK 50/25/25 allocation (stocks/bonds/cash). The different panels are how much year-to-year flexibility in the real withdrawal is allowed using the Vanguard Dynamic approach (e.g., see https://www.vanguard.ca/documents/literature/dynamic-ret-spending-paper.pdf for details). For example, in the panel marked '2' this means that the real withdrawal is allowed to vary by up 2% per year.

The top left panel (marked 0) is the constant pound (i.e., SWR) approach - the income fell to zero in just under 5% of historical retirements after 30 years, and somewhere between 10% and 25% after 40 years. The bottom right panel (marked '100') is withdrawals using a constant percentage of portfolio (i.e., in this case, 3% of whatever the portfolio value is at the time) - while the income never fell to zero, it did become very small after 40 years (1% in worst case and about 2.7% in the median case). The other panels represent cases between these two extremes.

The two extremes have opposite advantages and disadvantages:

1) For SWR approach, the income is constant in real terms (advantage) until it fails (disadvantage).

2) For percentage portfolio, the income never fell to zero (advantage) but it did fall to less than 1% in the worst cases after 40 years (disadvantage).

Which is best for a given retiree is dependent on their circumstances. For example,

1) A retiree whose expenditure is largely covered by sources of guaranteed income (state pension, DB pension, annuities, inflation linked ladders) may be be happier with more income variation (so could choose a higher flexibility number)

2) A retiree whose sources of guarantee income fall well below their required expenditure, might be happier with a lower flexibility number.

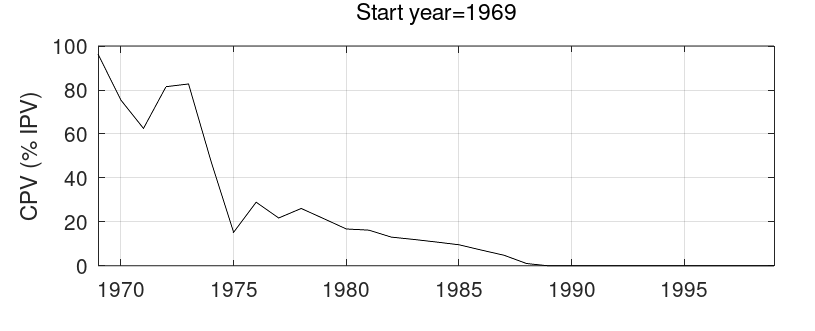

1969 is a problematic retirement (see the plot of SWR vs time in earlier post) - using 4% withdrawals (to save space, I've cut the lower panel off).

Here is 100% stocks

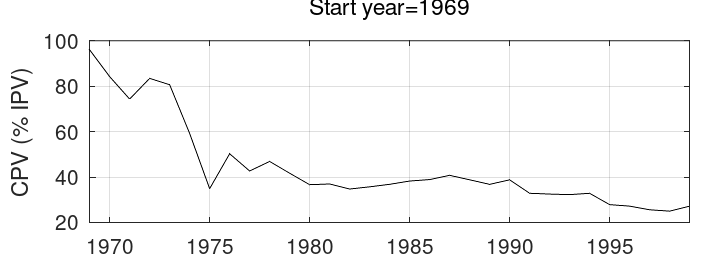

And the following is for 50% stocks (and 50% cash - note that with 100% bonds, the portfolio falls to zero in 1994).

You're right - the first 5 years are plain sailing, but at some point during 1973 (and certainly by the beginning of 1974), worry would be setting in (in either case to be honest).

3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards