We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

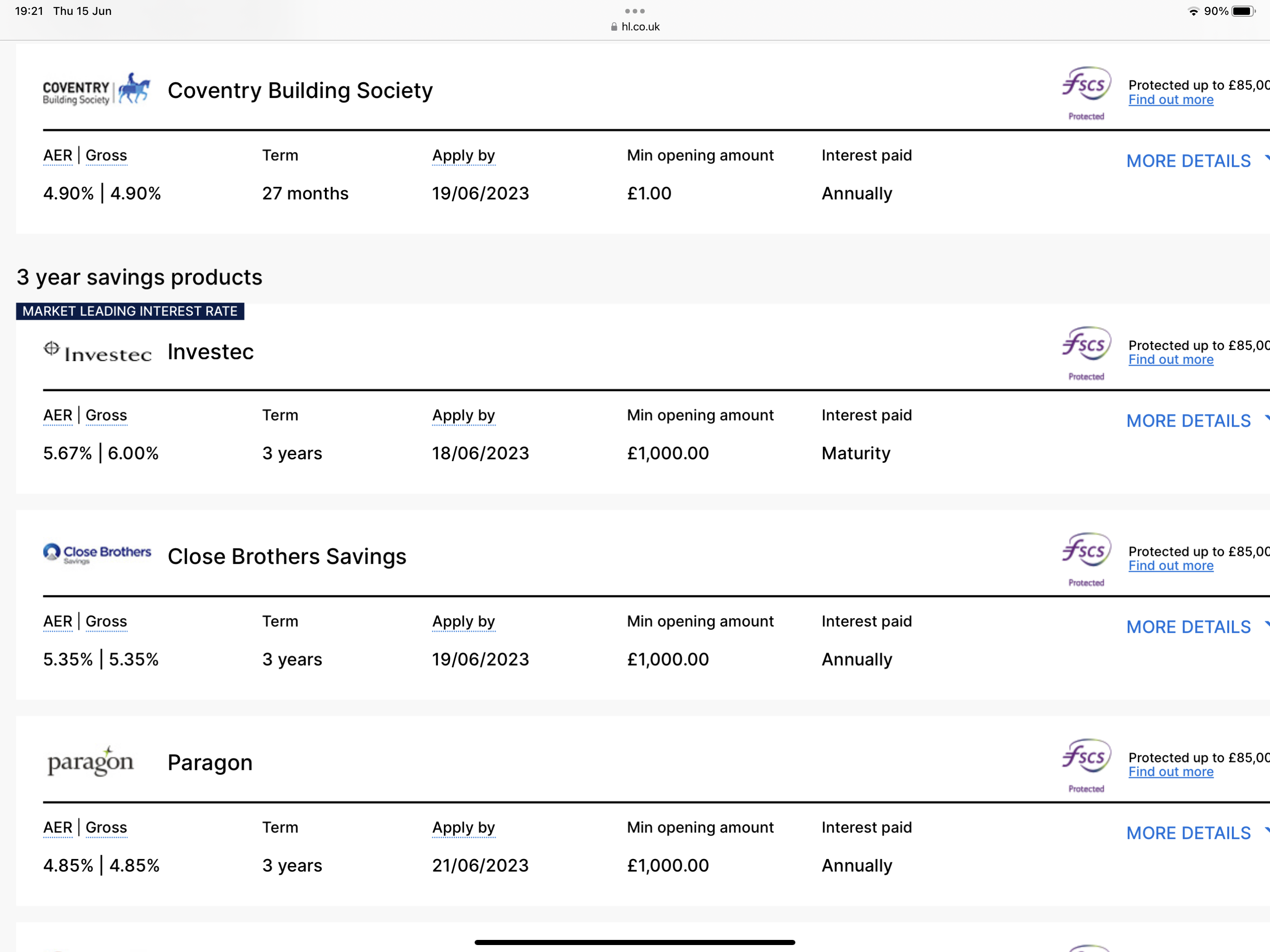

Expecting a fixed rate to be 5.50% by June 2023.

Comments

-

I wonder if Barclays will ever launch a regular saver account again - the article says they used to have one. It seems to be the only main high street player with no such account.RG2015 said:

I'm not actually waiting for anything as my comment was purely academic.VNX said:

Good luck waiting for 10%RG2015 said:What about the possibility of 10% soon?

We already have a 12 month 9% fixed rate on the Saffron Members' Monthly Loyalty Saver for a monthly £50 deposit.

It may only yield about £29 after 12 months but technically it is a fixed rate as per the thread title.

We will have 10% pretty soon but probably another building society wanting a quick influx of capital.

Just after the financial crisis of 2007/2008, there were record breaking rates of 10% and even 12% regular savers.

https://www.theguardian.com/money/2008/jun/07/banksIf you want me to definitely see your reply, please tag me @forumuser7 Thank you.

N.B. (Amended from Forum Rules): You must investigate, and check several times, before you make any decisions or take any action based on any information you glean from any of my content, as nothing I post is advice, rather it is personal opinion and is solely for discussion purposes. I research before my posts, and I never intend to share anything that is misleading, misinforming, or out of date, but don't rely on everything you read. Some of the information changes quickly, is my own opinion or may be incorrect. Verify anything you read before acting on it to protect yourself because you are responsible for any action you consequently make... DYOR, YMMV etc.2 -

Barclays have their niche market leader with their 5% Rainy Day Saver. I doubt they would have a second loss leader with an RS account.ForumUser7 said:

I wonder if Barclays will ever launch a regular saver account again - the article says they used to have one. It seems to be the only main high street player with no such account.RG2015 said:

I'm not actually waiting for anything as my comment was purely academic.VNX said:

Good luck waiting for 10%RG2015 said:What about the possibility of 10% soon?

We already have a 12 month 9% fixed rate on the Saffron Members' Monthly Loyalty Saver for a monthly £50 deposit.

It may only yield about £29 after 12 months but technically it is a fixed rate as per the thread title.

We will have 10% pretty soon but probably another building society wanting a quick influx of capital.

Just after the financial crisis of 2007/2008, there were record breaking rates of 10% and even 12% regular savers.

https://www.theguardian.com/money/2008/jun/07/banks5 -

I think the high street banks have their own 'loss leader' products, but don't want to have too many going at the same time. E.g. First Direct have their 7% RS as their loss leader, but nothing else of note. Similar with Natwest/RBS with 6%+ RS's.ForumUser7 said:

I wonder if Barclays will ever launch a regular saver account again - the article says they used to have one. It seems to be the only main high street player with no such account.RG2015 said:

I'm not actually waiting for anything as my comment was purely academic.VNX said:

Good luck waiting for 10%RG2015 said:What about the possibility of 10% soon?

We already have a 12 month 9% fixed rate on the Saffron Members' Monthly Loyalty Saver for a monthly £50 deposit.

It may only yield about £29 after 12 months but technically it is a fixed rate as per the thread title.

We will have 10% pretty soon but probably another building society wanting a quick influx of capital.

Just after the financial crisis of 2007/2008, there were record breaking rates of 10% and even 12% regular savers.

https://www.theguardian.com/money/2008/jun/07/banks

Barclays probably see their 5% Rainy Day saver as their loss leader, so don't want to offer a high interest RS at the same time. Maybe if they were to make the Rainy Day one NLA, then they may replace it with a high interest RS in the future.5 -

RG2015 said:

Barclays have their niche market leader with their 5% Rainy Day Saver. I doubt they would have a second loss leader with an RS account.ForumUser7 said:

I wonder if Barclays will ever launch a regular saver account again - the article says they used to have one. It seems to be the only main high street player with no such account.RG2015 said:

I'm not actually waiting for anything as my comment was purely academic.VNX said:

Good luck waiting for 10%RG2015 said:What about the possibility of 10% soon?

We already have a 12 month 9% fixed rate on the Saffron Members' Monthly Loyalty Saver for a monthly £50 deposit.

It may only yield about £29 after 12 months but technically it is a fixed rate as per the thread title.

We will have 10% pretty soon but probably another building society wanting a quick influx of capital.

Just after the financial crisis of 2007/2008, there were record breaking rates of 10% and even 12% regular savers.

https://www.theguardian.com/money/2008/jun/07/banks

I suppose, but Santander has their edge saver and RS at the same time - albeit it the edge saver is a lower rate and lower max deposit, and not so competitive anymoret1redmonkey said:

I think the high street banks have their own 'loss leader' products, but don't want to have too many going at the same time. E.g. First Direct have their 7% RS as their loss leader, but nothing else of note. Similar with Natwest/RBS with 6%+ RS's.ForumUser7 said:

I wonder if Barclays will ever launch a regular saver account again - the article says they used to have one. It seems to be the only main high street player with no such account.RG2015 said:

I'm not actually waiting for anything as my comment was purely academic.VNX said:

Good luck waiting for 10%RG2015 said:What about the possibility of 10% soon?

We already have a 12 month 9% fixed rate on the Saffron Members' Monthly Loyalty Saver for a monthly £50 deposit.

It may only yield about £29 after 12 months but technically it is a fixed rate as per the thread title.

We will have 10% pretty soon but probably another building society wanting a quick influx of capital.

Just after the financial crisis of 2007/2008, there were record breaking rates of 10% and even 12% regular savers.

https://www.theguardian.com/money/2008/jun/07/banks

Barclays probably see their 5% Rainy Day saver as their loss leader, so don't want to offer a high interest RS at the same time. Maybe if they were to make the Rainy Day one NLA, then they may replace it with a high interest RS in the future.If you want me to definitely see your reply, please tag me @forumuser7 Thank you.

N.B. (Amended from Forum Rules): You must investigate, and check several times, before you make any decisions or take any action based on any information you glean from any of my content, as nothing I post is advice, rather it is personal opinion and is solely for discussion purposes. I research before my posts, and I never intend to share anything that is misleading, misinforming, or out of date, but don't rely on everything you read. Some of the information changes quickly, is my own opinion or may be incorrect. Verify anything you read before acting on it to protect yourself because you are responsible for any action you consequently make... DYOR, YMMV etc.1 -

Though many of the other banks offer a cash switching incentive and/or decent reward account as well as a high paying regular.t1redmonkey said:

I think the high street banks have their own 'loss leader' products, but don't want to have too many going at the same time. E.g. First Direct have their 7% RS as their loss leader, but nothing else of note. Similar with Natwest/RBS with 6%+ RS's.ForumUser7 said:

I wonder if Barclays will ever launch a regular saver account again - the article says they used to have one. It seems to be the only main high street player with no such account.RG2015 said:

I'm not actually waiting for anything as my comment was purely academic.VNX said:

Good luck waiting for 10%RG2015 said:What about the possibility of 10% soon?

We already have a 12 month 9% fixed rate on the Saffron Members' Monthly Loyalty Saver for a monthly £50 deposit.

It may only yield about £29 after 12 months but technically it is a fixed rate as per the thread title.

We will have 10% pretty soon but probably another building society wanting a quick influx of capital.

Just after the financial crisis of 2007/2008, there were record breaking rates of 10% and even 12% regular savers.

https://www.theguardian.com/money/2008/jun/07/banks

Barclays probably see their 5% Rainy Day saver as their loss leader, so don't want to offer a high interest RS at the same time. Maybe if they were to make the Rainy Day one NLA, then they may replace it with a high interest RS in the future.

With first direct new customers get £175, interest free OD and the 7% regular saver. Natwest/RBS offer a £200 switching incentive, £3/mth back in rewards and the 6% regular saver. Lloyds offer a CL lifestyle benefit, 2 regular savers and a switching incentive etc.

Barclays offer just the 5% rainy day saver and a reward account whose rewards are cancelled out by the £5 monthly fee.

1 -

BoE hikes that are expected are already "priced in" and therefore reflected (in theory) by current fixed rates available. The best thing to watch are Gilt yields or Swap rates - you can look at charts somewhere like https://www.investing.com/rates-bonds/uk-1-year-bond-yield to see how things are moving. Currently a hike on the next BoE meeting (22nd June) is fully expected and a 5% bank rate (=0.5% more than now) is about 80%+ expected later this year, probably by the 3Aug BoE meeting. Many more hikes than that aren't really priced in, but it's about how long they keep the Bank rate high and the timing of any subsequent rate cuts that will affect the 1yr average rate just as much as how high it goes.boingy said:I think we've got at least two more BoE hikes to come so I'd expect 5.5% fixed to be exceeded. However, I don't have a crystal ball and I have been known to be wrong.

I'm assuming rates will peak sometime this year. What I don't know is what happens after that. Do they stay level-ish for an extended period or do they slowly start coming down? The BoE is independent but I imagine it will come under some significant pressure from a Govt with one eye on a probable General Election next year. Bribing the electorate is as common as kissing babies in the build-up to a GE so tax rates and interest rates will not necessarily be dictated by pure economics.

Fix rates tend to lag the Gilt/Swap market by a days or weeks, there was a big spike (0.4-0.5%) after the last set on inflation data on 24th May and it took a week for fixes to reflect some of this and arguably they still haven't priced all of this move. The next inflation data is on 21st June - if that is higher than expected then Gilt yields will go up again and fix rates will also move up again and we could see 5.5% for 1yr around the end of June/start of July. Note that 1yr Gilt yields should always be lower than 1yr fix rates offered by banks as lending to the govt is in theory much safer, and also banks are often able to use deposits to allow them to lend at higher interest rates.

It's worth pointing out that the market is pricing in a 70% chance of a rate hike in the US in either June or July but *also* less than a 70% chance that it is lower by December, so the expected outcome is another hike soon, followed by rate cuts within 5 months of this hike. The UK current expectation is more like 2 hikes soon and cuts in the first half of 2024, higher inflation means the timing of any cuts can get pushed back which would raise fix rates simply because the expected average of the bank rate over the coming year would be higher.3 -

I think this thread needs a gentle bump.

0 -

Gilt moves suggest we should hit 5.5% or so. Whether that's brief or persistent depends on the data (e.g. next week's inflation numbers).2

-

3

-

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards