We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Difference between partially settled and fully settled?

TylerDurden36

Posts: 87 Forumite

Hi. So 2 years ago I had an account with Arrow Global and was paying £10 a month off a £1100 debt. I did this for 12 months and then the bank card I was using to pay this every month had its details stolen while I was at Alton Towers. Next thing I know arrow global had defaulted my account. I just left it which was very silly in retrospect but I felt cheated as I’d been paying it but then got a default without any warning.

Anyway so last year the debt was sold to a company called Capquest who have been chasing me for the money for months. Today they sent me a settlement offer for 50% off the £980 still owing. So I paid the £490 today hoping that this would make a positive impact on my credit file. But after doing a bit of online reading it seems that a partially settled account is actually worse than not paying at all and has a more negative effect. My question is this. Is it worth ringing Capquest and paying off the remaining £490? Would there be any difference between partially settled and fully settled? Have I just wasted £490? Starting to think I should have just left it as even paying it off doesn’t remove the default which in of itself is just crazy. How can paying a debt in full have no effect on a default? You’re basically ruined for 6 years if you get slapped with one! Thanks in advance for any replies.

Anyway so last year the debt was sold to a company called Capquest who have been chasing me for the money for months. Today they sent me a settlement offer for 50% off the £980 still owing. So I paid the £490 today hoping that this would make a positive impact on my credit file. But after doing a bit of online reading it seems that a partially settled account is actually worse than not paying at all and has a more negative effect. My question is this. Is it worth ringing Capquest and paying off the remaining £490? Would there be any difference between partially settled and fully settled? Have I just wasted £490? Starting to think I should have just left it as even paying it off doesn’t remove the default which in of itself is just crazy. How can paying a debt in full have no effect on a default? You’re basically ruined for 6 years if you get slapped with one! Thanks in advance for any replies.

0

Comments

-

Not paying at all < partial settlement < full settlement

1 -

So does that mean it’s all the same? Makes absolutely no difference whether it’s partially paid, fully paid or not paid at all? So glad I’ve just thrown away £490 then!DullGreyGuy said:Not paying at all < partial settlement < full settlement

I suppose the only good thing is that they can’t pursue me for the debt anymore so it can’t get any worse such as a CCJ or similar.Oh well!0 -

No.TylerDurden36 said:

So does that mean it’s all the same? Makes absolutely no difference whether it’s partially paid, fully paid or not paid at all? So glad I’ve just thrown away £490 then!DullGreyGuy said:Not paying at all < partial settlement < full settlement

I suppose the only good thing is that they can’t pursue me for the debt anymore so it can’t get any worse such as a CCJ or similar.Oh well!

If you read the post again, you'll see that the lesser than symbol has been used, not the equals sign.

You haven't thrown any money away. You given someone else's money back to them and improved your credit files.

Result.0 -

Oh right ok that’s good then. Wild you say it would be better to ring them back next month and pay the full amount or will it make little difference now that dent has been partially settled?MorningcoffeeIV said:

No.TylerDurden36 said:

So does that mean it’s all the same? Makes absolutely no difference whether it’s partially paid, fully paid or not paid at all? So glad I’ve just thrown away £490 then!DullGreyGuy said:Not paying at all < partial settlement < full settlement

I suppose the only good thing is that they can’t pursue me for the debt anymore so it can’t get any worse such as a CCJ or similar.Oh well!

If you read the post again, you'll see that the lesser than symbol has been used, not the equals sign.

You haven't thrown any money away. You given someone else's money back to them and improved your credit files.

Result.

I read somewhere that paying off any of it can have a detrimental effect on the credit file which made no sense to me. The debt company said it can take 6 to 8 weeks to change on my report so I guess I won’t know until then.0 -

Paying a debt does not remove a default, it will be there for 6 years regardless of what you do.

The difference to your credit file, between a settled debt, and a partially settled debt is minimal, and only of any importance if you go looking for further credit.

Pay no heed to the silly credit score, that will fluctuate with any change, good or bad, and is only ever seen by you anyway.

What you have done is got Capquest off your back, ideally you should have had the deal agreed in writing, to stop them selling on the remainder of your debt, but hopefully you received something of that nature.

Paying the remaining balance would not be an option, as they should write it off, and you would just be wasting your money anyway, as the only loser would be you.

I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

Hi thanks for the reply.sourcrates said:Paying a debt does not remove a default, it will be there for 6 years regardless of what you do.

The difference to your credit file, between a settled debt, and a partially settled debt is minimal, and only of any importance if you go looking for further credit.

Pay no heed to the silly credit score, that will fluctuate with any change, good or bad, and is only ever seen by you anyway.

What you have done is got Capquest off your back, ideally you should have had the deal agreed in writing, to stop them selling on the remainder of your debt, but hopefully you received something of that nature.

Paying the remaining balance would not be an option, as they should write it off, and you would just be wasting your money anyway, as the only loser would be you.

I was aware of the default not being lifted until after 6 years as my brother had a £2000 debt with with a bank that was in default. They never chased him for it and last year it was removed after 6 years and his credit score went through the roof. Went up something like 100 points over 3 months.

The whole default system is a bit mad to me. I only owed £1000 and was happily paying it off until my card details were stolen. A month later and I’m hit with a default that basically ruins my life for 6 years even though I’d happily pay the debt.

Why is it so tough on people? 6 years is huge. You get less time for a serious crime!

Anyway thanks again and I’ll not the pay the rest. They are sending me a letter to confirm that it has been paid. Cheers.0 -

The default is a factual record of what happened. You did not make the payments due under the agreement that you entered into with the lender. It stays on your file for six years so that other potential lenders know what happened and can take it into account when deciding whether to lend you money.TylerDurden36 said:

Hi thanks for the reply.sourcrates said:Paying a debt does not remove a default, it will be there for 6 years regardless of what you do.

The difference to your credit file, between a settled debt, and a partially settled debt is minimal, and only of any importance if you go looking for further credit.

Pay no heed to the silly credit score, that will fluctuate with any change, good or bad, and is only ever seen by you anyway.

What you have done is got Capquest off your back, ideally you should have had the deal agreed in writing, to stop them selling on the remainder of your debt, but hopefully you received something of that nature.

Paying the remaining balance would not be an option, as they should write it off, and you would just be wasting your money anyway, as the only loser would be you.

I was aware of the default not being lifted until after 6 years as my brother had a £2000 debt with with a bank that was in default. They never chased him for it and last year it was removed after 6 years and his credit score went through the roof. Went up something like 100 points over 3 months.

The whole default system is a bit mad to me. I only owed £1000 and was happily paying it off until my card details were stolen. A month later and I’m hit with a default that basically ruins my life for 6 years even though I’d happily pay the debt.

Why is it so tough on people? 6 years is huge. You get less time for a serious crime!

Anyway thanks again and I’ll not the pay the rest. They are sending me a letter to confirm that it has been paid. Cheers.

If you were happy to pay the money, then you should have done so and there would have been no need for a default to be issued.0 -

The default was issued without any notice whatsoever. I missed one payment. I had no idea this was going to happen. I thought the payment came from my bank account not my card so when the card details were stolen the payments stopped. They never sent me any letters. Just whacked me with a default.TheBanker said:

The default is a factual record of what happened. You did not make the payments due under the agreement that you entered into with the lender. It stays on your file for six years so that other potential lenders know what happened and can take it into account when deciding whether to lend you money.TylerDurden36 said:

Hi thanks for the reply.sourcrates said:Paying a debt does not remove a default, it will be there for 6 years regardless of what you do.

The difference to your credit file, between a settled debt, and a partially settled debt is minimal, and only of any importance if you go looking for further credit.

Pay no heed to the silly credit score, that will fluctuate with any change, good or bad, and is only ever seen by you anyway.

What you have done is got Capquest off your back, ideally you should have had the deal agreed in writing, to stop them selling on the remainder of your debt, but hopefully you received something of that nature.

Paying the remaining balance would not be an option, as they should write it off, and you would just be wasting your money anyway, as the only loser would be you.

I was aware of the default not being lifted until after 6 years as my brother had a £2000 debt with with a bank that was in default. They never chased him for it and last year it was removed after 6 years and his credit score went through the roof. Went up something like 100 points over 3 months.

The whole default system is a bit mad to me. I only owed £1000 and was happily paying it off until my card details were stolen. A month later and I’m hit with a default that basically ruins my life for 6 years even though I’d happily pay the debt.

Why is it so tough on people? 6 years is huge. You get less time for a serious crime!

Anyway thanks again and I’ll not the pay the rest. They are sending me a letter to confirm that it has been paid. Cheers.

If you were happy to pay the money, then you should have done so and there would have been no need for a default to be issued.

The system isn’t fair because all circumstances are different and should be treated as such. It just tars everyone with the same brush regardless of circumstance.0 -

Creditors are supposed to follow guidelines under CONC regulations, and section 87 of the consumer credit act.

However, as they are just guidelines, and not set in stone law, there is a wide interpretation of the rules displayed by different creditors, some are quick to default, others are not so quick, it really is the luck of the draw, and yes, 6 years is a long time to be penalised, especially when the circumstances were dubious, but unfortunately that is the system we are stuck with.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter0 -

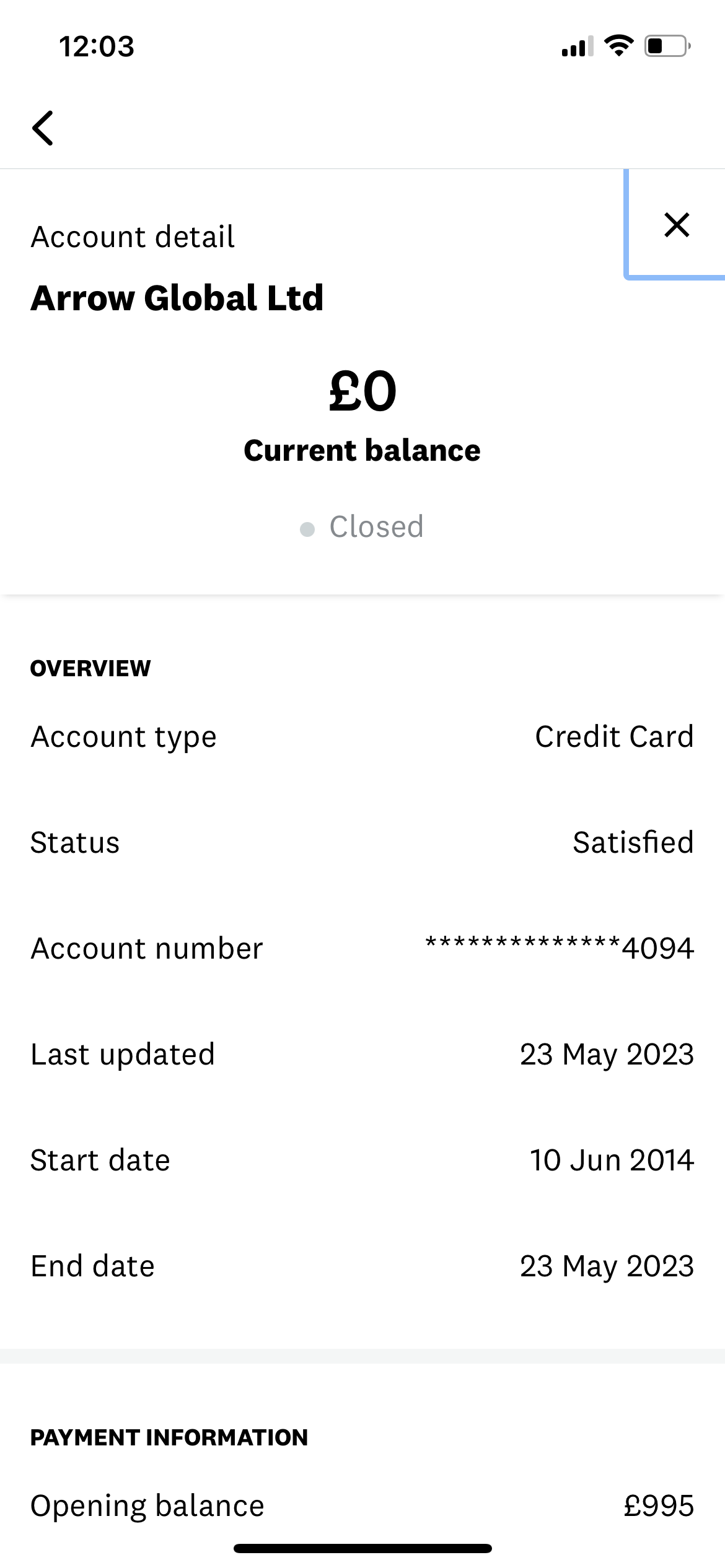

If anyone is interested the default is no longer on my credit file after todays update. Just says satisfied under closed accounts (see photo). It’s not upped my score much but hopefully that will go up more over time.

0

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.1K Reduce Debt & Boost Income

- 455K Spending & Discounts

- 246.6K Work, Benefits & Business

- 602.9K Mortgages, Homes & Bills

- 178K Life & Family

- 260.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards