We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

HMRC Poor Wording

RG2015

Posts: 6,229 Forumite

in Cutting tax

Over the years I have been confused by numerous examples of poor wording from HMRC. If it wasn’t bad enough that tax rules are incredibly confusing, we have to put up with ambiguous, misleading and often illogical wording.

The purpose here is to highlight these with a view to providing a level of clarity, preferably without having to wade through pages of HMRC descriptions. There may be good reasons for some of these such as HMRC having to implement politically driven edicts, but that doesn’t really help the poor punters.

I have picked out a few examples for starters.

The purpose here is to highlight these with a view to providing a level of clarity, preferably without having to wade through pages of HMRC descriptions. There may be good reasons for some of these such as HMRC having to implement politically driven edicts, but that doesn’t really help the poor punters.

I have picked out a few examples for starters.

- The personal savings allowance is not an allowance but a nil rate tax band. It also does not relate to savings but rather to interest on savings.

- Investment income includes interest received on savings accounts. This despite saving (in savings accounts) and investing being quite different from each other.

- Per HMRC. You need to register for Self Assessment if your income from savings and investments is over £10,000. This does not include interest received on ISAs or dividends received on investments which are not applicable for this £10k threshold.

- The tax year for interest received is based on the date it is available not for the year when it was earned.

I am sure there are many more and these can be added if anyone wishes.

2

Comments

-

My 'favourite ' is that Pension contributions made via Net Pay, actually do not come out of your actual net pay, but come out pre tax.

No scope for confusion there !2 -

One I think can clearly cause confusion is this from the pension tax relief page.If you do not pay Income Tax

You still automatically get tax relief at 20% on the first £2,880 you pay into a pension each tax year (6 April to 5 April) if both of the following apply to you:

you do not pay Income Tax, for example because you’re on a low income

your pension provider claims tax relief for you at a rate of 20% (relief at source)2 -

Following a suggestion from @Secret2nd Account on another thread, I have given feedback on ISA interest forming part of the £10,000 threshold for registering for self assessment.

https://forums.moneysavingexpert.com/discussion/comment/80034572#Comment_80034572Secret2ndAccount said:

Instead of repeatedly posting on this forum, why don't you report your concerns to HMRC? Every page on their site has a button near the bottom marked 'Report a problem with this page'RG2015 said:

It is irrelevant whether I accept answers from a group of strangers on a public forum.auser99 said:@RG2015, let me ask a new question.

From the many people who have told you how it works, do you now accept the answer?

So we can get back to reading about gloriously high new fixed rates

I am simply saying that HMRC do not make this at all clear. I would much prefer an unambiguous statement from HMRC.

I will respond with the following question.

Do you acknowledge that the following statement from the HMRC website implies all interest including ISA interest?

You need to register for Self Assessment if your income from savings and investments is over £10,000.

Here is the page you want to report:

https://www.gov.uk/check-if-you-need-tax-return/y/no/no/less-than-50-000/no0 -

It is referring to how the relief is given, not how the contributions are made. So under net pay arrangements the scheme provider has with hmrc.Albermarle said:My 'favourite ' is that Pension contributions made via Net Pay, actually do not come out of your actual net pay, but come out pre tax.

No scope for confusion there !

You keep using that word. I do not think it means what you think it means - Inigo Montoya, The Princess Bride1 -

I fully understand that, but it is a potential point of confusion for people who have no real understanding how tax relief works. We had a poster on the pensions forum recently, where their employer had even got the two terms mixed up.unholyangel said:

It is referring to how the relief is given, not how the contributions are made. So under net pay arrangements the scheme provider has with hmrc.Albermarle said:My 'favourite ' is that Pension contributions made via Net Pay, actually do not come out of your actual net pay, but come out pre tax.

No scope for confusion there !

They informed the pension provider that it was a Net Pay arrangement, so the provider added no tax relief. However the employer than took the contributions from the employees net/taxed pay, because they misunderstood the rather confusing terminology.0 -

Self assessment page 1:

"Are you married?"

The actual question is "were you married during the tax period that you are completing a self assessment for."

Usually almost a year in the past

About 2 million people who have recently got my married or divorced may answer this incorrectly

My personal favourite is not being allowed to enter £ or . In any of the additional details fields.

4 -

Where has that wording been taken from? It is true that income from investments with a high proportion of bonds is categorised as interest rather than dividends, but that just means that 'interest can come from some investments as well as savings', rather than "Investment income includes interest received on savings accounts", so perhaps I'm missing the context?RG2015 said:- Investment income includes interest received on savings accounts. This despite saving (in savings accounts) and investing being quite different from each other.

Looks like the ISA issue has been done to death elsewhere (the general principle being that ISAs are excluded from anything to do with income tax, as explained at https://www.gov.uk/individual-savings-accounts/how-isas-work ), but it's also necessary to self-assess with dividend income over £10K, so the wording seems correct?RG2015 said:- Per HMRC. You need to register for Self Assessment if your income from savings and investments is over £10,000. This does not include interest received on ISAs or dividends received on investments which are not applicable for this £10k threshold.

RG2015 said:

Not sure I'm seeing how that's poor wording from HMRC as such, unless they state or imply something to the contrary somewhere?- The tax year for interest received is based on the date it is available not for the year when it was earned.

1 -

Or press the return button! Nightmare!mark_cycling00 said:Self assessment page 1:

"Are you married?"

The actual question is "were you married during the tax period that you are completing a self assessment for."

Usually almost a year in the past

About 2 million people who have recently got my married or divorced may answer this incorrectly

My personal favourite is not being allowed to enter £ or . In any of the additional details fields.1 -

1. investment Income.eskbanker said:

Where has that wording been taken from? It is true that income from investments with a high proportion of bonds is categorised as interest rather than dividends, but that just means that 'interest can come from some investments as well as savings', rather than "Investment income includes interest received on savings accounts", so perhaps I'm missing the context?RG2015 said:- Investment income includes interest received on savings accounts. This despite saving (in savings accounts) and investing being quite different from each other.

Looks like the ISA issue has been done to death elsewhere (the general principle being that ISAs are excluded from anything to do with income tax, as explained at https://www.gov.uk/individual-savings-accounts/how-isas-work ), but it's also necessary to self-assess with dividend income over £10K, so the wording seems correct?RG2015 said:- Per HMRC. You need to register for Self Assessment if your income from savings and investments is over £10,000. This does not include interest received on ISAs or dividends received on investments which are not applicable for this £10k threshold.

RG2015 said:

Not sure I'm seeing how that's poor wording from HMRC as such, unless they state or imply something to the contrary somewhere?- The tax year for interest received is based on the date it is available not for the year when it was earned.

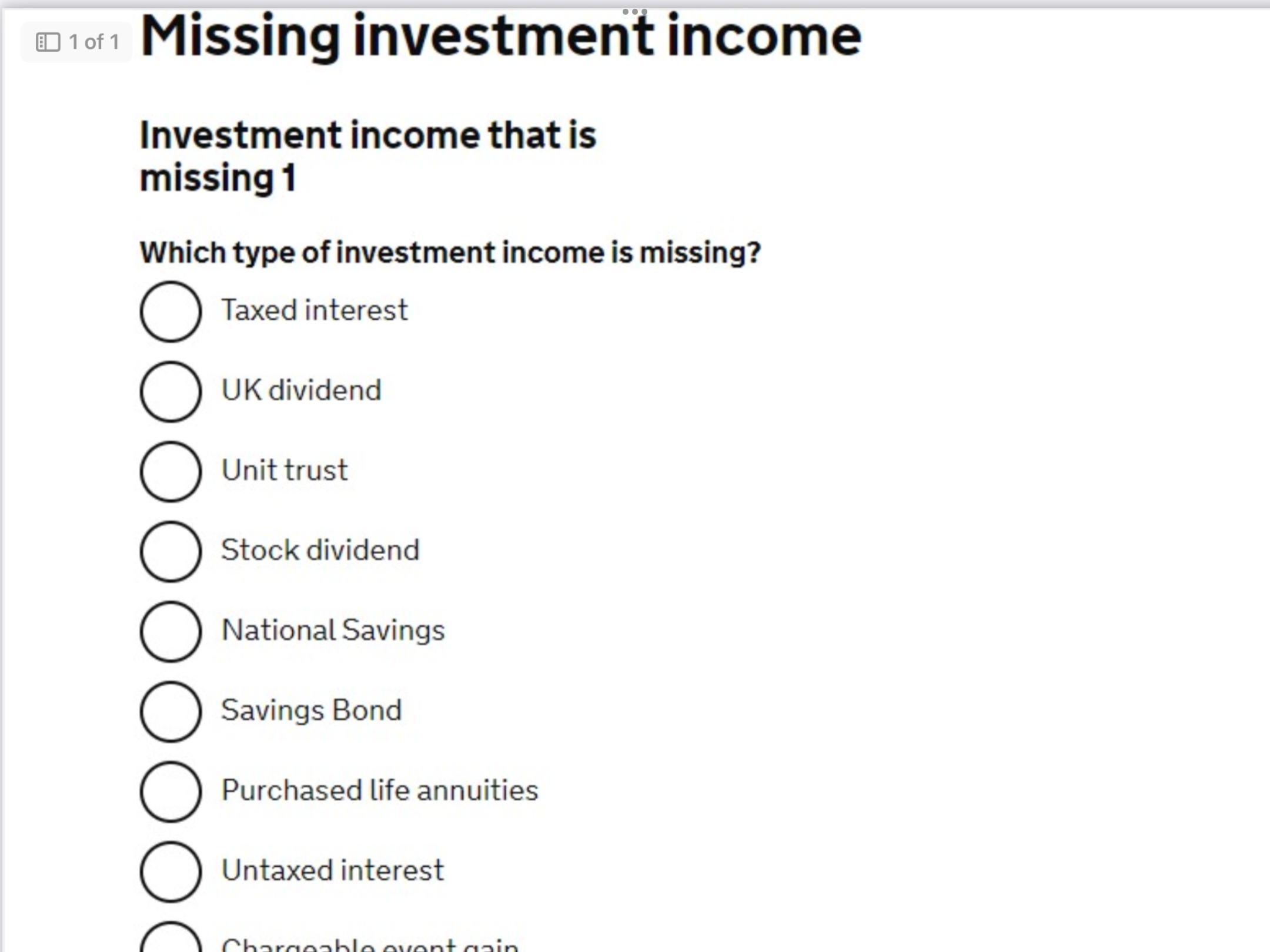

On the personal tax online page for reporting missing investment income, which includes untaxed interest.

0 -

That list looks remarkably like the available options HMRC have to record details on your tax record.RG2015 said:

1. investment Income.eskbanker said:

Where has that wording been taken from? It is true that income from investments with a high proportion of bonds is categorised as interest rather than dividends, but that just means that 'interest can come from some investments as well as savings', rather than "Investment income includes interest received on savings accounts", so perhaps I'm missing the context?RG2015 said:- Investment income includes interest received on savings accounts. This despite saving (in savings accounts) and investing being quite different from each other.

Looks like the ISA issue has been done to death elsewhere (the general principle being that ISAs are excluded from anything to do with income tax, as explained at https://www.gov.uk/individual-savings-accounts/how-isas-work ), but it's also necessary to self-assess with dividend income over £10K, so the wording seems correct?RG2015 said:- Per HMRC. You need to register for Self Assessment if your income from savings and investments is over £10,000. This does not include interest received on ISAs or dividends received on investments which are not applicable for this £10k threshold.

RG2015 said:

Not sure I'm seeing how that's poor wording from HMRC as such, unless they state or imply something to the contrary somewhere?- The tax year for interest received is based on the date it is available not for the year when it was earned.

On the personal tax online page for reporting missing investment income, which includes untaxed interest.

https://www.gov.uk/hmrc-internal-manuals/paye-manual/paye1300601

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards