We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Trying to understand drawdown SWR

Comments

-

Just to put some flesh on some of the comments

Here are the historical 'safe' withdrawal rates (SWR) for a 30 year retirement as a function of retirement start year for the USA (top) and UK (bottom). Portfolios in each case were 60% domestic stocks and 40% domestic bonds (15-20 year maturities) - asset returns and inflation are drawn from https://www.macrohistory.net/ while the code is my own.

The worst case (1937 for the UK and 1965 for the US) gave a SAFEMAX (or maximum safe withdrawal rate, MSWR) of about 3.7% for the US and 2.7% for the UK. The exact figures depend on

a) the duration of the retirement

b) the stock and bond allocation

c) for the UK, the pre-1948 inflation data used (there are at least 4 credible time series prior to the adoption of RPI) leads to variations of about 20 basis points

d) The maturity of the bonds used (e.g. for the US, 5 year bonds gave a better result, while for the UK bills, i.e., a cash proxy, gave a marginally better result in most of the worst cases). Variations are 30-40 basis points.

e) The exact set of returns used for the stock market (again, pre-index days, there are a number of ways of constructing the 'stock market').

f) I've used annual data, for monthly data (which I don't have for the UK, but do for the US), the worst cases are 20-50 basis points lower (depending on stock allocation).

As an aside, the highest SWR in the UK occurred for someone retiring in 1975 (i.e., around the end of the UK stock market slump) - in reality, they would have seen their portfolio drop dramatically over the previous couple of years and would probably have held on for a year or two to see their portfolio recover).

As others have said, this is a useful very rough planning guide (e.g. assuming around 2.5%, 3.0%, or 3.5% depending on age) - using this approach in reality has a number of flaws, not least that considering the variations in points c to f above can lead to variations in MSWR of upwards of 50 basis points as well as the fact that MSWR can only ever be revised downward (e.g. prior to 1965 (edit: actually 30 years later in 1995, i.e., when Bengen wrote his paper), a US retiree would have considered about 4.2% to be 'safe', while a late 19th century Bengen would have concluded that 5% was safe).

4 -

And just for completeness, here is a plot of historical UK MSWR (SAFEMAX) as a function of planned retirement duration for domestic stock allocations of 0%, 20%, 40%, 60%, 80%, and 100%. I've used a 50/50 mix of longish bonds (15-20 years) and bills (3 months, i.e. a cash proxy) for the fixed income component (so an effective maturity of about 7-10 years).

As is well known (but nice to see), for long planned retirements (20 years+), holding more stocks was beneficial (although not a lot of difference between 80% and 100%), while for short planned retirements (<15 years), there was not a huge difference for any allocations of 20 to 80%.

6 -

Thank you - you have given really thorough replies.OldScientist said:It is possible to combine various approaches, e.g.,

1) Income from State pension, DB pensions (if available), and, if necessary, inflation linked annuity to meet essential expenditure (definitions of 'essential' will differ from person to person, but housing, bills, and food are a bare minimum).

2) Variable withdrawals (e.g., 5% of the current value of the pot) from a portfolio of stocks, bonds, and cash to provide income for discretionary expenditure. That this might vary from month to month or year to year with investment performance is less likely to be critical (e.g., in bad years there will be less money for holidays, home improvements, etc.). Mathematically, the portfolio will never completely run out, but the amount remaining (and hence income) may become small if investment returns over the next decades are poor.

This is the essentially the approach we are currently using - until we are old enough to get our state pensions, our basic expenditure is covered by my DB pension, while 'extras' are funded by variable withdrawals from our portfolio. In the event of my death prior to state pension age my OH will only have half the DB income, so we have used term life insurance to cover at least part of this shortfall (which is yet another thing to think about).

I think we are lucky in that our SPs and DB pensions (Civil Service and LGPS) should cover all of our comfortable needs. For us this means a fairly active social life, fortnight in the sun and new car every 5 or 6 years. They should also rise with inflation.

So I appreciate what we are dithering about is the DC money that will provide the cherry on the cake - a second car, more city break holidays, more eating out etc. I consider us very fortunate.

But the money was worked for and so we don't want to throw it away. We also consider that as we age, we are less likely to want the second car, so much foreign travel, so are not so concerned with the effect of inflation on the amount we get from the DC pension. If the money runs out and we still really want all that stuff, we'll downsize")

This is true - at least now people can shop around - and not chose an annuity at all.af1963 said:Not all that long ago though, you wouldn't have had the dilemma, because you wouldn't have had the choice - you'd have been able to take up to a fixed maximum lump sum if you chose to, and then you'd have had to buy an annuity with the remainder. People today in defined benefit schemes have similar limited ( although often also generous) options.

This is a choice that lots of people struggle with - it's one of the biggest financial decisions they will take, probably bigger than buying a house. But at least having the choice means you can look at what may suit your own personal circumstances.

0 -

OldScientist said:And just for completeness, here is a plot of historical UK MSWR (SAFEMAX) as a function of planned retirement duration for domestic stock allocations of 0%, 20%, 40%, 60%, 80%, and 100%. I've used a 50/50 mix of longish bonds (15-20 years) and bills (3 months, i.e. a cash proxy) for the fixed income component (so an effective maturity of about 7-10 years).

As is well known (but nice to see), for long planned retirements (20 years+), holding more stocks was beneficial (although not a lot of difference between 80% and 100%), while for short planned retirements (<15 years), there was not a huge difference for any allocations of 20 to 80%.

Out of interest and off topic, what program did you use for the graphics?

0 -

hildasmuriel said:

Thank you - you have given really thorough replies.OldScientist said:It is possible to combine various approaches, e.g.,

1) Income from State pension, DB pensions (if available), and, if necessary, inflation linked annuity to meet essential expenditure (definitions of 'essential' will differ from person to person, but housing, bills, and food are a bare minimum).

2) Variable withdrawals (e.g., 5% of the current value of the pot) from a portfolio of stocks, bonds, and cash to provide income for discretionary expenditure. That this might vary from month to month or year to year with investment performance is less likely to be critical (e.g., in bad years there will be less money for holidays, home improvements, etc.). Mathematically, the portfolio will never completely run out, but the amount remaining (and hence income) may become small if investment returns over the next decades are poor.

This is the essentially the approach we are currently using - until we are old enough to get our state pensions, our basic expenditure is covered by my DB pension, while 'extras' are funded by variable withdrawals from our portfolio. In the event of my death prior to state pension age my OH will only have half the DB income, so we have used term life insurance to cover at least part of this shortfall (which is yet another thing to think about).

I think we are lucky in that our SPs and DB pensions (Civil Service and LGPS) should cover all of our comfortable needs. For us this means a fairly active social life, fortnight in the sun and new car every 5 or 6 years. They should also rise with inflation.

So I appreciate what we are dithering about is the DC money that will provide the cherry on the cake - a second car, more city break holidays, more eating out etc. I consider us very fortunate.

But the money was worked for and so we don't want to throw it away. We also consider that as we age, we are less likely to want the second car, so much foreign travel, so are not so concerned with the effect of inflation on the amount we get from the DC pension. If the money runs out and we still really want all that stuff, we'll downsize

You're right, it is a good position to be in. I'd suggest 'dithering' (perhaps 'careful consideration' might be a kinder phrase) is better than launching in without a thought! Your position also means that mistakes with your DC pot are less likely to derail your retirement.

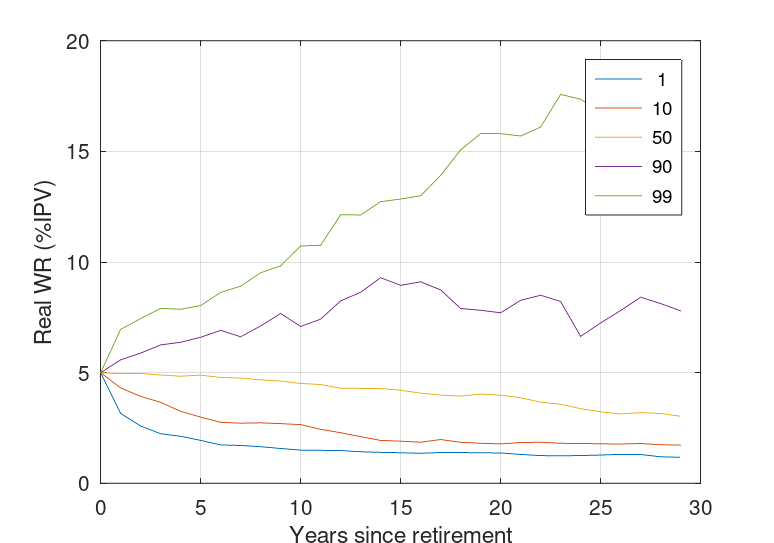

If you'll forgive me for one further graph, the following is a plot of the historical UK real withdrawal rate as a function of time since retirement at the 1st, 10th, 50th (i.e. median), 90th, and 99th percentiles for a constant percentage withdrawal of 5% (this is not same as the inflation adjusted percentage discussed earlier) with a UK portfolio of 60% stocks, 20% bonds, 20% cash.

In the worst cases, after 30 years the income was down to a not great, but at least not zero,1% of the initial portfolio (in real terms), but the median case was still providing an income of 3% with 60% of the original pot (again in real terms) for legacy purposes.

While I'm not using this exact method (we're using VPW, see https://www.bogleheads.org/wiki/Variable_percentage_withdrawal ), personally, I've found a rather mechanical approach has helped me to continue to withdraw money through some of the ups and downs in the stock and bond markets over the last 3.5 years.

2 -

But it isnt known forever as you don't know the inflation rates forever and these will have an impact on the value of your money as time goes on.hildasmuriel said:So the suggested amount (say 3.5%) is of the current total? Not the starting total? Because the rough guide I read said it was of the starting amount which makes no sense whatsoever because that means you would only ever take out 3.5% of the initial amount and it would presumably grow and grow and you would never touch it.

But, with the exception of cash, surely each of those can go down in value? Whereas with a fixed income, the amount you get is known for ever. For a non-risk taker, that has to be a big draw.Drawdown is a method of drawing your pension and nothing to do with the investments in your pension. you can have cash in your pension, property, fixed interest securities or equities.1 -

With apologies to the OP, I used the mac version of octave (https://www.octave.org/ )Suhusa said:OldScientist said:And just for completeness, here is a plot of historical UK MSWR (SAFEMAX) as a function of planned retirement duration for domestic stock allocations of 0%, 20%, 40%, 60%, 80%, and 100%. I've used a 50/50 mix of longish bonds (15-20 years) and bills (3 months, i.e. a cash proxy) for the fixed income component (so an effective maturity of about 7-10 years).

As is well known (but nice to see), for long planned retirements (20 years+), holding more stocks was beneficial (although not a lot of difference between 80% and 100%), while for short planned retirements (<15 years), there was not a huge difference for any allocations of 20 to 80%.

Out of interest and off topic, what program did you use for the graphics?

1 -

Thanks OldScientist - I think a lot of people find it easier to understand concepts with graphics to back up blocks of texts.OldScientist said:0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.7K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.8K Work, Benefits & Business

- 603.3K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards