We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Co-operative bank refusing to pay £125 refer-a-friend offer FOS case

Comments

-

You should be aware of that being as when you opened a new current account a few months after closing previous current account your original online login details became live again shortly after new account opening had been validated by co-operative bank following secondary checks, something that is not unique to them.Alex9384 said:Ed-1 said:Investigator's view: Again, customer is not aware of "having a profile on their system". For how long does this profile exist? Do Coop tell you that you'll have a profile on their system after closing the account?0

Again, customer is not aware of "having a profile on their system". For how long does this profile exist? Do Coop tell you that you'll have a profile on their system after closing the account?0 -

Playing devil's advocate, FOS have always been clear that they aren't exclusively driven by the law (and Ts & Cs, etc) but by what's "fair and reasonable" - this will generally be in the consumer's favour if FOS considers the spirit rather than the letter of the law, as it were, but in cases like this the FOS approach might actually count against complainants who may be perceived to be trying it on, even if they technically have the Ts & Cs in their favour?https://www.financial-ombudsman.org.uk/who-we-are/make-decisions

How we reach decisions

We have a duty to resolve complaints based on what we think is fair and reasonable in all the circumstances of the case.

6 -

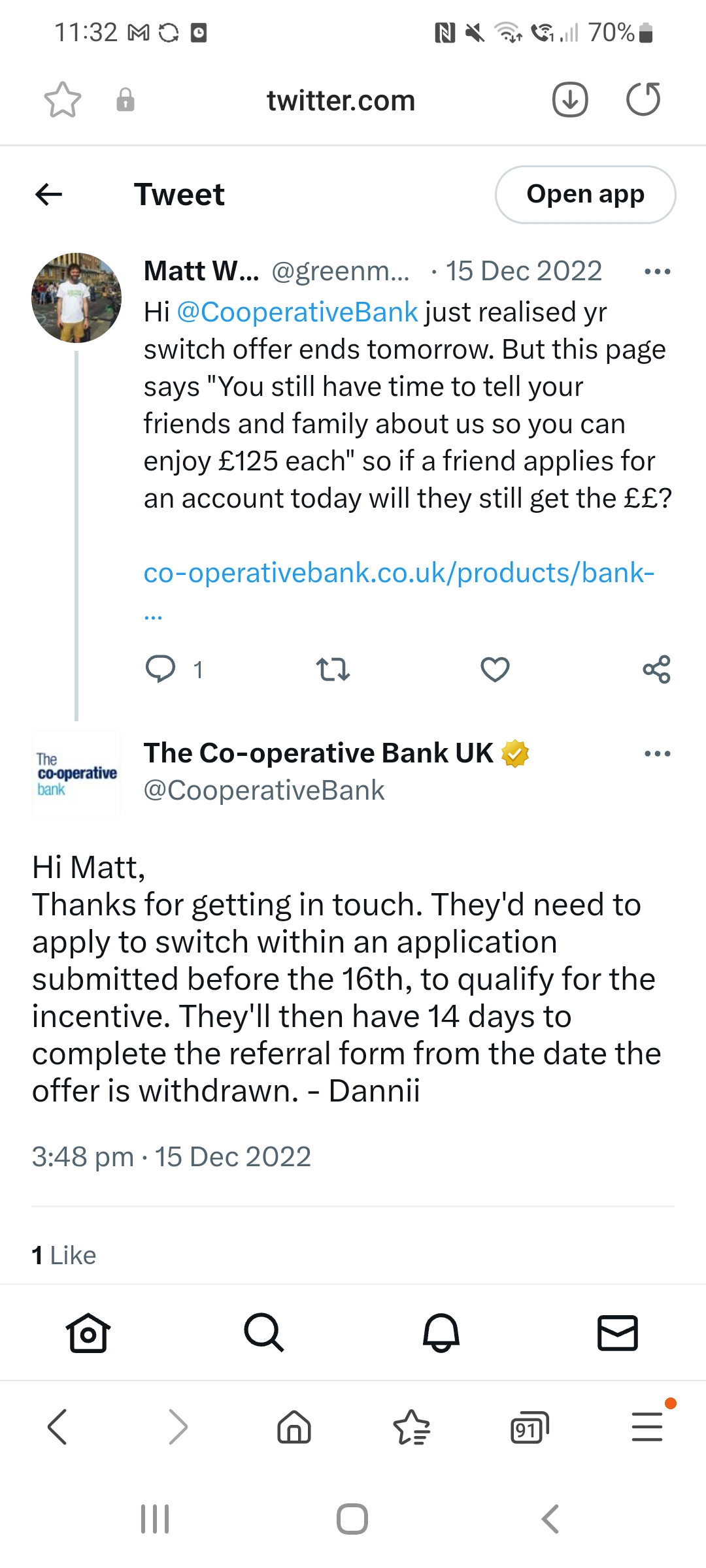

If it helps I took the attached screenshot of a tweet from them saying it was withdrawn on the 16th December (their first £125 offer)

If it helps I took the attached screenshot of a tweet from them saying it was withdrawn on the 16th December (their first £125 offer)

1 -

bristolleedsfan said:You should be aware of that being as when you opened a new current account a few months after closing previous current account your original online login details became live again shortly after new account opening had been validated by co-operative bank following secondary checks, something that is not unique to them.

But you won't find out until you open a new account. I tried to log in after I switched out and I wasn't able to.

For comparison, I switched out my Metro account in October 2021 and I just logged in 5 minutes ago using my original details, despite not having any account with them anymore.

That wasn't the case with Coop. My login details did not allow me to log in after I switched out, so I assumed it's gone for good..

EPICA - the best symphonic metal band in the world !0 -

What the Metro bank or indeed any other bank does is in comparison is irrelevant. Assuming it is going to be the same with the CO-OP is not clever.Alex9384 said:bristolleedsfan said:You should be aware of that being as when you opened a new current account a few months after closing previous current account your original online login details became live again shortly after new account opening had been validated by co-operative bank following secondary checks, something that is not unique to them.

But you won't find out until you open a new account. I tried to log in after I switched out and I wasn't able to.

For comparison, I switched out my Metro account in October 2021 and I just logged in 5 minutes ago using my original details, despite not having any account with them anymore.

That wasn't the case with Coop. My login details did not allow me to log in after I switched out, so I assumed it's gone for good..0 -

diinozzo said:What the Metro bank or indeed any other bank does is in comparison is irrelevant. Assuming it is going to be the same with the CO-OP is not clever.

My point was that Coop makes it look like your account is gone for good, once you switch out, while some other banks still let you log in even if you don't have any account with them anymore. Therefore, it was reasonable to assume that Coop didn't keep my profile active on their systems.

EPICA - the best symphonic metal band in the world !0 -

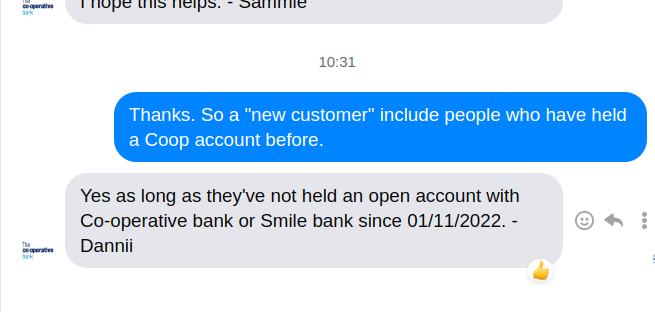

One more time, from their previous T&C:"To qualify for this offer as an eligible new customer you must:

2.p.1. open a new Co-operative Bank standard Current Account ... "T&C does NOT exclude people who have held a Coop account before and doesn't specify who a new customer is. It only says that in order to qualify, you need to open a new account.

Now, in the new T&C (May 2023) they added a clause with dates, which wasn't present in the previous T&C.

This only shows that even according to Coop themselves, a new customer can be someone who has held a Coop account in the past but doesn't have one anymore. So, without this additional clause, it was still reasonable to assume that we were new customers, simply because we didn't have any Coop account at the time of the offer and we opened new Coop account. Right or wrong?

EPICA - the best symphonic metal band in the world !0 -

I believe you are correct, we should be considered to be new customers, and it appears (at least in my case) the case handler agreed. My case handler said this:Alex9384 said:One more time, from their previous T&C:"To qualify for this offer as an eligible new customer you must:

2.p.1. open a new Co-operative Bank standard Current Account ... "T&C does NOT exclude people who have held a Coop account before and doesn't specify who a new customer is. It only says that in order to qualify, you need to open a new account.

Now, in the new T&C (May 2023) they added a clause with dates, which wasn't present in the previous T&C.

This only shows that even according to Coop themselves, a new customer can be someone who has held a Coop account in the past but doesn't have one anymore. So, without this additional clause, it was still reasonable to assume that we were new customers, simply because we didn't have any Coop account at the time of the offer and we opened new Coop account. Right or wrong?Looking at the updated £125 terms & conditions document I think you would have been considered a new customerSo it seems to me that the question that has led to us not being paid is not whether or not you are a new customer but is instead whether or not the £125 offers were the same as the £50 offer.3 -

You're not going to believe the investigator's response to my counter arguments.

They're now pointing out the current offer webpage and saying that it is clear that as an account was held since 1st November 2022 you're not a new customer.

Because it is all the same scheme, apparently the terms announced yesterday now apply to switches done in February!5 -

Ed-1 said:You're not going to believe the investigator's response to my counter arguments.

They're now pointing out the current offer webpage and saying that it is clear that as an account was held since 1st November 2022 you're not a new customer.

Because it is all the same scheme, apparently the terms announced yesterday now apply to switches done in February!

Oh dear... Are you guys actually exchanging emails with the FOS back and forth?

Are you guys actually exchanging emails with the FOS back and forth?

EPICA - the best symphonic metal band in the world !0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards