We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

PLEASE READ BEFORE POSTING: Hello Forumites! In order to help keep the Forum a useful, safe and friendly place for our users, discussions around non-MoneySaving matters are not permitted per the Forum rules. While we understand that mentioning house prices may sometimes be relevant to a user's specific MoneySaving situation, we ask that you please avoid veering into broad, general debates about the market, the economy and politics, as these can unfortunately lead to abusive or hateful behaviour. Threads that are found to have derailed into wider discussions may be removed. Users who repeatedly disregard this may have their Forum account banned. Please also avoid posting personally identifiable information, including links to your own online property listing which may reveal your address. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

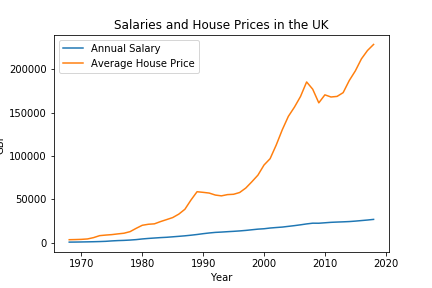

Retiring landlords risk fuelling rental shortage

Comments

-

I bought my first house in 1978 so I also felt that pain.theartfullodger said:

Little story: In November 1979 under Thatcher's Iron handbag Bank of England base rates hit 17% (!) - Seventeen percent. Had a for then large mortgage. It was painful - although my building society (remember them..??) only wanted 15%,. You young folk ain't seen nothing yet...

Best wishes to all.

However that house, then 5 years old, cost £10,000.

Those houses now fetch upwards of £250,000 even though they are 50 years old now and need a lot of TLC.

Allowing for inflation that house would have cost £40,000 at today's prices. No chance of anybody lending me that, plus the repayments, hard enough to scrape together in those days, would have been an eyewatering 4x what they actually were.

So perhaps not quite so easy for today's young folk!1 -

Reported.newsgroupmonkey_ said:[Deleted User] said:

This is just daft. There are lots of people trying to save to buy at the moment. Some number of people who aren't doesn't make the others go away or mean we shouldn't try to help them.newsgroupmonkey_ said:

We've had this conversation time and time again.Firstly, not everyone wants to buy.Secondly, even if houses were £100k and only needed a 5% mortgage, many people live so hand to mouth that they can't afford to save £5k.Finally, many people have bad credit ratings, so they couldn't get a mortgage even if they could afford it.Bringing in rent controls and no-fault evictions won't stop them selling when people leave. As I said in my post, AFAIK, they've never kicked anyone out. They may have issued S8s before, but I don't remember ever mention of an S21. They wait for people to leave, then sell. One less home on the rental market.

The BTL market isn't causing the surge in house prices over the last few years. It may have done back in the 1990s when my folks bought many of theirs and prices were cheap.

BTL absolutely is both pushing prices up, and making it harder for people to buy when they are up against BTL people in a better financial position and little care about defects in the property.

Why do you keep posting this nonsense?OK, taking your abuse aside..... I'll be the bigger man.Of course there are lots of people saving to buy. My children are amongst them.

BTL hasn't been massively increasing the prices for some time. As the original post says, older folk are selling up. We've seen on this forum for some time that people are dropping their BTLs because of the tax burden, stricter rules and so on that have been coming on for some time.The problem is (and I could even give you some crashy statistics if you want), that there frankly isn't enough housing stock. That's what is pushing the prices up. And rents too.

Taking your aduse aside, FTBs are in a very difficult position. They usually need a big mortgage, and are at a point in their career before their peak earning. Often the places they can afford are prime BTL properties too.

Lots of BTL people in the market directly affects their ability to buy.0 -

17% sounds high until you realise that your house cost a fraction of what houses cost today, relative to average income.theartfullodger said:There have always been landlords retiring: Often for reasons nothing to do with legislation & tax changes. There have always been new landlords coming into the B2L market. There always will be.

As it happens I've been getting rid of property 500+ miles away as due to my age (75, brain not what it was) and health issues (nothing serious but makes travel etc much much harder...) but not due to tax & law changes. 2 sold during lockdown, another under offer now.

The current fuss over the impending doom of Buy2Let is hugely exaggerated...

Little story: In November 1979 under Thatcher's Iron handbag Bank of England base rates hit 17% (!) - Seventeen percent. Had a for then large mortgage. It was painful - although my building society (remember them..??) only wanted 15%,. You young folk ain't seen nothing yet...

Best wishes to all.0 -

Indeed. I read an article recently (I'll post a link if i can find it again) that said that when you take into account income to house price ratios, mortgage repayments as a percentage of income, inflation, cost of living etc then the 15% that people often talk about (including my father in law, who, like the poster above, is of the "we had it much harder than you" persuasion) is actually akin to people paying around 3% interest nowadays.[Deleted User] said:

17% sounds high until you realise that your house cost a fraction of what houses cost today, relative to average income.theartfullodger said:There have always been landlords retiring: Often for reasons nothing to do with legislation & tax changes. There have always been new landlords coming into the B2L market. There always will be.

As it happens I've been getting rid of property 500+ miles away as due to my age (75, brain not what it was) and health issues (nothing serious but makes travel etc much much harder...) but not due to tax & law changes. 2 sold during lockdown, another under offer now.

The current fuss over the impending doom of Buy2Let is hugely exaggerated...

Little story: In November 1979 under Thatcher's Iron handbag Bank of England base rates hit 17% (!) - Seventeen percent. Had a for then large mortgage. It was painful - although my building society (remember them..??) only wanted 15%,. You young folk ain't seen nothing yet...

Best wishes to all.1 -

Yeah, all in these stories from the 70s and 80s are before prices went insane in the 2000s.

My parent's first house cost £36k adjusted for inflation, on a mid 70s combined income of £18k adjusted for inflation.

People who think they had it hard back then really have no idea.1 -

Also savings rates were higher, AND compounded! (A luxury that many bank accounts now do not offer).[Deleted User] said:

17% sounds high until you realise that your house cost a fraction of what houses cost today, relative to average income.theartfullodger said:There have always been landlords retiring: Often for reasons nothing to do with legislation & tax changes. There have always been new landlords coming into the B2L market. There always will be.

As it happens I've been getting rid of property 500+ miles away as due to my age (75, brain not what it was) and health issues (nothing serious but makes travel etc much much harder...) but not due to tax & law changes. 2 sold during lockdown, another under offer now.

The current fuss over the impending doom of Buy2Let is hugely exaggerated...

Little story: In November 1979 under Thatcher's Iron handbag Bank of England base rates hit 17% (!) - Seventeen percent. Had a for then large mortgage. It was painful - although my building society (remember them..??) only wanted 15%,. You young folk ain't seen nothing yet...

Best wishes to all.

I've been saving all my life for a house deposit. For most of that time all my money in the bank has been earning next to nothing (and I'm someone who reads the MSE articles and shops around for the best rates).

Of course now that I'll have no savings left (if I finally buy somewhere) the rates are now going up!

There's a reason that many older un's own multiple houses and were able to buy these while earning only a single household salary in a manual job.. Try that nowadays even with TWO top-end salaries after many years of academic study, with the student debt tagged on, too! There's a reason the average age of FTBs is now in the mid-thirties (like me, 35)... (And people wonder why the population is decreasing!)1 -

House prices house prices went bonkers in the ‘80’s. My folks bought at auction in the early 60’s for just under £3K. they sold that house for £40K in 1985. Almost three years later the same house sold for just over £80K. My folks managed to get a £10K mortgage in 1985, having paid off their previous £2K mortgage. Things were different back then. These days their house has been sold and now funds my mum’s care home.

Fast forward to now and my colleague recently bought a newish 4 bed. He hasn’t moved into it yet preferring to decorate throughout first, and has been living in his newish 2 bed down the street, also mortgaged. Colleague is in his early 30’s and joined the workplace less than 10 years ago.0 -

I inherited half a house when my Mum died. My brother bought me out, so he now owns a whole rental property, mortgage free. Neither of us wanted to give the tenant notice as we felt - and still feel- very strongly that it’s her home. The problem now is that in order to be able to afford to live closer to family (as opposed to completely by himself), my brother needs the capital from the house. A mortgage on it wouldn’t work due to his personal circumstances (newly self employed, single). Obviously, in an ideal world the tenant would give notice but I don’t think she will.

House prices are complicated. Sure, BTL has removed some stock. There are also many people in unsuitable houses. Some rattle about by themselves in a 4 bed. Others are crammed in, 6 to a 2 bed. Short of insisting that at retirement everyone moves into a sheltered accommodation flat (!) that’s going to be an issue. First time buyers tend to be older nowadays, so what used to suit them (1 or 2 bed starter home) doesn’t work. The increase in working from home has meant that people want at least one spare room to work in.

Of course, what would really help a lot of people who are on low incomes/precarious jobs/want to stay local to family etc is if a load of new council houses (not housing association, or affordable housing, but proper council housing) was built. Build proper communities with a good mix of housing stock and employment opportunities- and repeal the Right to Buy. I’ll get my coat!

2 -

Exactly, and savings rates were good back then as well. Smart landlords sold up two or three years ago, or fixed for ten.[Deleted User] said:

17% sounds high until you realise that your house cost a fraction of what houses cost today, relative to average income.theartfullodger said:There have always been landlords retiring: Often for reasons nothing to do with legislation & tax changes. There have always been new landlords coming into the B2L market. There always will be.

As it happens I've been getting rid of property 500+ miles away as due to my age (75, brain not what it was) and health issues (nothing serious but makes travel etc much much harder...) but not due to tax & law changes. 2 sold during lockdown, another under offer now.

The current fuss over the impending doom of Buy2Let is hugely exaggerated...

Little story: In November 1979 under Thatcher's Iron handbag Bank of England base rates hit 17% (!) - Seventeen percent. Had a for then large mortgage. It was painful - although my building society (remember them..??) only wanted 15%,. You young folk ain't seen nothing yet...

Best wishes to all.1 -

The other thing they usually forget is pensions. You have to put a hell of a lot more in now to get a decent return. All those fantastic final salary, defined benefit schemes are long gone.BobT36 said:

Also savings rates were higher, AND compounded! (A luxury that many bank accounts now do not offer).[Deleted User] said:

17% sounds high until you realise that your house cost a fraction of what houses cost today, relative to average income.theartfullodger said:There have always been landlords retiring: Often for reasons nothing to do with legislation & tax changes. There have always been new landlords coming into the B2L market. There always will be.

As it happens I've been getting rid of property 500+ miles away as due to my age (75, brain not what it was) and health issues (nothing serious but makes travel etc much much harder...) but not due to tax & law changes. 2 sold during lockdown, another under offer now.

The current fuss over the impending doom of Buy2Let is hugely exaggerated...

Little story: In November 1979 under Thatcher's Iron handbag Bank of England base rates hit 17% (!) - Seventeen percent. Had a for then large mortgage. It was painful - although my building society (remember them..??) only wanted 15%,. You young folk ain't seen nothing yet...

Best wishes to all.

I've been saving all my life for a house deposit. For most of that time all my money in the bank has been earning next to nothing (and I'm someone who reads the MSE articles and shops around for the best rates).

Of course now that I'll have no savings left (if I finally buy somewhere) the rates are now going up!

There's a reason that many older un's own multiple houses and were able to buy these while earning only a single household salary in a manual job.. Try that nowadays even with TWO top-end salaries after many years of academic study, with the student debt tagged on, too! There's a reason the average age of FTBs is now in the mid-thirties (like me, 35)... (And people wonder why the population is decreasing!)

Combined with a higher cost of living now, the loss of decent public transport links and the fact that many new estates are in the middle of nowhere... The cost of living is much higher now.

Care is another huge cost that is being laid on younger people, to put a limit on lifetime costs for older people. The idea being that they have something to pass on. The irony...1

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards