We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Anything better than BlackRock Consensus 100 available at the moment

Comments

-

The hardest bit is being mature enough to control your fear and greed.bostonerimus said:this investing lark seems pretty simple to me.

1 -

Linton said:

But perhaps it would be prudent to balance this with the experience of investors who had highly undiversified investments and failed miserably. Trouble is the winners tend to trumpet their success and lthe losers keep quiet.adindas said:

Did I ever say I want to become another Warren Buffet. How did you know that I blindly following him. I follow and learn strategies of various Proven billionaire investor, not from random guy from the internet.Linton said:

If you want to become another Warren Buffer you need to do a little more than pick random quotes from him and blindly follow them. Do you have the skills and the money to do the rest of what being a Warren Buffet involves?adindas said:Linton said:adindas said:bostonerimus said:

You only mention the success stories for such a strategy, not the people who have failed. A well diversified portfolio is best for most people. It made me a millionaire and all the funds I ever invested in were diversified equity and bond funds. I'll never be a billionaire, but I don't need to be one as I'm still financially independent which was my goal.adindas said:msallen said:

And ...? As those funds are very diversified they will achieve a form of "average" return. That being the case there are bound to be lots of things that have recently performed better, and a roughly similar amount that have performed worse.adindas said:It will depend on you definition of better. There are a lot of funds, individual stocks are currently performing better than Blackrock Consensus 100 and Vanguard LifeStrategy 100.Correct if it is randomly chosen, not with strategic and methodical ways. And I do not need to repeat about diversification again and again. Excessive diversifications are not a good investment strategy. This is not me saying that it is strategy from billionaires proven investors such as Warren Buffett Charlie, Munger, Peter Lynch, Bill Ackman, Howard Marks, Jim Simons, John Templeton, etc. Most of these proven billionaires investors are contrarians and contrarian do not do excessive diversification.That is the strategy they have been applying for years. Search it, there are already a lot of links about this in this saving and investment forum.Some same group of people in this MSE do not like if there is reminder again what these proven billionaires investors have been saying so I suggest you search from previous posts.Aa Everyone could become a millionaire if they keep adding money until at least a million in the stock market, they have assets in value of at least 1mil does not he ??

b) You do not even need to invest in the stock market to become a millionaire. Everyone with income exceeding the outgoing spending will be financially independent does not he.c) What matter is do you outperform the return from the market.d) I never say people do not need to diversity I am just confronting the view of the urban myth that excessive diversification is a good strategy for those whose aim is to grow their wealth which I believe the aim of majority of people when investing. Otherwise why not just keep it all in saving account, safe and secure, risk free.....

d) I do not understand the concept of excessive diversification. One can have inappropriate diversification or insufficient diversification. Your understanding of diversification seems somewhat limited. It is not simply a matter of % bond funds but rather how do you minimise risk by investing in as broad a range of assets as possible whilst still meeting your objectives.Rather than getting involved in a never ended argument with random guy on the internet, better to use a well known figure, proven investors. This guy is your opponent. Please do contact him what he means with that. Someone limited knowledge might exceed the knowledge of other random guy on the internet. Does anyone need a lot of efforts to understand what diversification mean in investing?? Those who don't have basic understanding should not be getting involved in investing in the first instance.ChatGPT, Investopedia for the beginning. And there are a lot of sources.Oh well, I waiting a lot of dislike posting autorotative source like this. But even using authoritative sources people still still arguing, let alone if you are just a random guy on the internet.

Someone limited knowledge might exceed the knowledge of other random guy on the internet. Does anyone need a lot of efforts to understand what diversification mean in investing?? Those who don't have basic understanding should not be getting involved in investing in the first instance.ChatGPT, Investopedia for the beginning. And there are a lot of sources.Oh well, I waiting a lot of dislike posting autorotative source like this. But even using authoritative sources people still still arguing, let alone if you are just a random guy on the internet.

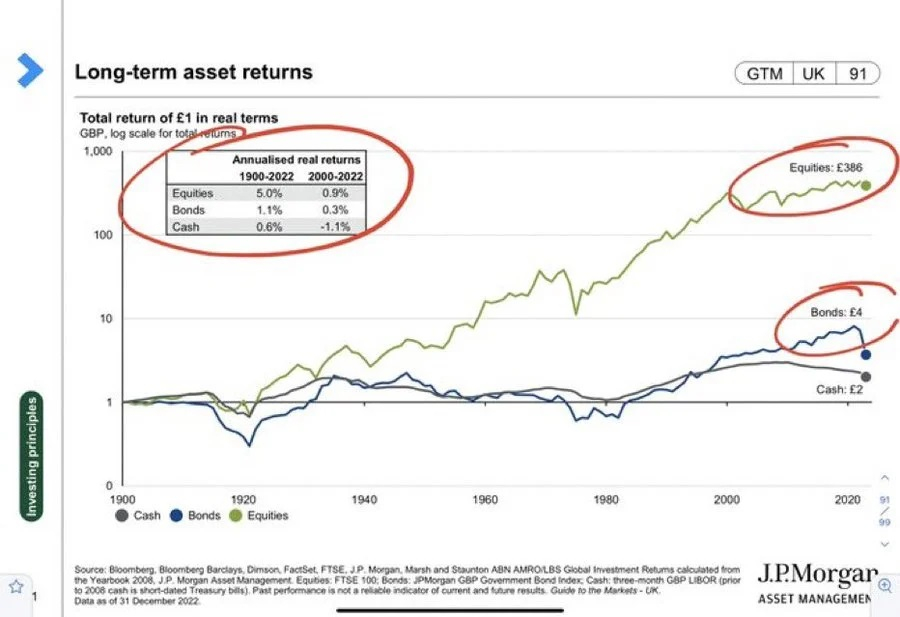

Rather than getting involved in a never ended argument with random guy on the internet, it is better to use the wisdom from a proven investors, isn't it ?I agree with that. But some people are just following the crowd of people who might have a different objectives, different horizon. Do people need an asset diversification adding bond assets (for instance) in their portfolio if the aim if to maximise growing their wealth in a long time Horizon after looking into this graphics ? It is similarly with diluting / mixing up a strong team with weak team. Keep in mind all equities portfolio could be contained in index fund, so there is some level of diversification here are getting involved.

There were quite a few people on this forum are complaining about their bond performance last year. Just look at the bond market performance last year, did they do the job to sooth volatility ??In the current climate some people would rather put the money into higher interest saving account earning 7%, 6%+. This return is better than the return from the bond market, but it is risk free and some of them are instant access.You might have notice in saving and investment forum, there are now increasingly people are doing that. Some people enhanced it with drip feeding it into the equity market using an enhanced DCA to avoid missing the best days in the stock market.0

There were quite a few people on this forum are complaining about their bond performance last year. Just look at the bond market performance last year, did they do the job to sooth volatility ??In the current climate some people would rather put the money into higher interest saving account earning 7%, 6%+. This return is better than the return from the bond market, but it is risk free and some of them are instant access.You might have notice in saving and investment forum, there are now increasingly people are doing that. Some people enhanced it with drip feeding it into the equity market using an enhanced DCA to avoid missing the best days in the stock market.0 -

There were quite a few people on this thread are complaining about their bond performance last year. Just look at the bond market performance last year, did they do the job to sooth volatility ??Markets will perform within expectations 95% of the time. Fixed Interest suffered two events that in a single year that fall within the 5%.

Do you not kid yourself about the scale of drop that can and will occur on equities when they suffer an event that falls within the 5%

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Agreed, investing is simple, but often not easy.Alexland said:

The hardest bit is being mature enough to control your fear and greed.bostonerimus said:this investing lark seems pretty simple to me.“So we beat on, boats against the current, borne back ceaselessly into the past.”1 -

Yes, if we knew the future this would all be a doddle. Bonds are having a bad moment and that has and will come to equities. So being diversified is necessary. We can argue about the appropriate amount for particular circumstances ie I'm 90% equities now in my funds as my fixed income is covered by cash savings, a pension and I have rental income, but people must be aware that backing a single horse to win can be a risky business, better to back a horse to place - eggs, baskets etc.dunstonh said:There were quite a few people on this thread are complaining about their bond performance last year. Just look at the bond market performance last year, did they do the job to sooth volatility ??Markets will perform within expectations 95% of the time. Fixed Interest suffered two events that in a single year that fall within the 5%.

Do you not kid yourself about the scale of drop that can and will occur on equities when they suffer an event that falls within the 5%“So we beat on, boats against the current, borne back ceaselessly into the past.”0 -

Yes, fair enough....many use physical replication too, at least for the bulk of the fund (and other techniques too) - but it doesn't really matter here.....the core point was about diversification.Alexland said:

To be fair the index trackers use optimal sampling techniques to balance the risk of tracking error against the trading cost of needing to buy into the whole market and sometimes this will cause minor variances but it should hopefully average out over time so they are capturing the market return while keeping costs low.MK62 said:A market tracker fund will invest in every company in that market (it has to really, as otherwise it's not really tracking the market), whereas an actively managed fund will not (to varying degrees)......the jury is still out on that one (and likely always will be), but there's no denying that the maximum diversification, market tracking, approach is a viable option for many.

So with passive you are getting an above average investor return through lower costs and with active you are taking a path where the return expectations are lower in the hope of being one of the few that gets better than passive results which studies suggest is easier to achieve in the short term than consistently over the long term.")

0 -

Well not really. Because I am fully aware how the Equities vs Bonds have been performing sofar, especially in the long run. The Graphics and the Table in the post above showing my awareness. Also each to their own but I personally don't invest in Bonds, my saving in RSA and high interest saving account earning a nice 7%, 6%+ are currently functioning better than the bond market risk free.This money are drip fed to equity using an enhanced DCA strategy.dunstonh said:There were quite a few people on this thread are complaining about their bond performance last year. Just look at the bond market performance last year, did they do the job to sooth volatility ??Markets will perform within expectations 95% of the time. Fixed Interest suffered two events that in a single year that fall within the 5%.

Do you not kid yourself about the scale of drop that can and will occur on equities when they suffer an event that falls within the 5%As I said before in this saving Investment some people (not me) are complaining about their bond performance that they did not expect. I remember a guy are even want to sue his Financial Adviser.0 -

Physical replication is good it means they own the assets - it's synthetic replication you need to watch out for. This is one are that US investors seem to be better protected as their investment company act and tax treatment make synthetic ETFs much less common than in Europe.MK62 said:Yes, fair enough....many use physical replication too, at least for the bulk of the fund (and other techniques too) - but it doesn't really matter here.....the core point was about diversification.

0 -

Well not really. Because I am fully aware how the Equities vs Bonds have been performing sofar, especially in the long run.What do you define as long run? There is the very long term which consumers wont be invested in and long term which could be as little as 15 years.

The very long term will mask long term rare events that could take decades to recover. An 80% loss on equities that takes 15 years to recover would have a catastrophic outcome for many people. Especially those in decumulation.But the counter to that is that any asset class that has fallen as much as fixed interest would be ripe for repurchase for the long term. Gilts are up around 6% in the last 6 months. They are still volatile and will remain so until inflation is thought to have properly peaked. However, with unit prices back to mid to late 1990s levels, the buying potential for the long term is much more attractive than cash.

but I personally don't invest in Bonds, my saving in RSA and high interest saving account earning a nice 7%, 6%+

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

Sorry I do not follow that. I prefer to follow the well known strategy from proven investors that have proven track records of making money in the stock market.dunstonh said:Well not really. Because I am fully aware how the Equities vs Bonds have been performing sofar, especially in the long run.What do you define as long run? There is the very long term which consumers wont be invested in and long term which could be as little as 15 years.

The very long term will mask long term rare events that could take decades to recover. An 80% loss on equities that takes 15 years to recover would have a catastrophic outcome for many people. Especially those in decumulation.But the counter to that is that any asset class that has fallen as much as fixed interest would be ripe for repurchase for the long term. Gilts are up around 6% in the last 6 months. They are still volatile and will remain so until inflation is thought to have properly peaked. However, with unit prices back to mid to late 1990s levels, the buying potential for the long term is much more attractive than cash.

but I personally don't invest in Bonds, my saving in RSA and high interest saving account earning a nice 7%, 6%+

What about gilt/Bonds performance last year ??

Did you observe the graphics, table that I have shown before ??

15 Years investing is a long wait ?. Well how many years typically investors are staying in the stock market ? How many years people stay investing in S&P500, FTSE100, etc Less than 15 years ??

Anyway if you see this graphics do investor need to wait 15 years before they realize that equity outperform bonds ?

For some investors put their money into saving are waiting allocation to equities using DCAs.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards