We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Incorrect bank transfer

Comments

-

RBS is Royal Bank of Scotland, NatWest Groupdeb1111 said:RBS. Which Halifax are part of. 😩

BoS is Bank of Scotland, Lloyds Banking Group

Halifax is part of Lloyds Banking Group, not NatWest GroupIf you want me to definitely see your reply, please tag me @forumuser7 Thank you.

N.B. (Amended from Forum Rules): You must investigate, and check several times, before you make any decisions or take any action based on any information you glean from any of my content, as nothing I post is advice, rather it is personal opinion and is solely for discussion purposes. I research before my posts, and I never intend to share anything that is misleading, misinforming, or out of date, but don't rely on everything you read. Some of the information changes quickly, is my own opinion or may be incorrect. Verify anything you read before acting on it to protect yourself because you are responsible for any action you consequently make... DYOR, YMMV etc.6 -

I don't know if they have disputed or not. All I know is that Halifax couldn't recover the money.masonic said:This seems a bit of an odd one as most banks signed up to the misdirected payments code of best practice, which I believe does permit a bank to make such disclosures as are necessary to allow legal proceedings to be initiated. Any complaint should always be made against your bank, because the recipient bank (if different) does not have a contractual relationship with you.It would be helpful to understand the facts of the matter:Do you know whether or not the recipient of the money has disputed that it was sent in error?Is the recipient bank signed up to the voluntary code?

I assume RBS are part of the voluntary code.0 -

Yes, I am fairly sure Natwest/RBS is signed up to the code. That means unless the recipient has disputed that the payment was misdirected, then you would have had it back, or a repayment plan would have been arranged. The recipient should have been warned that by falsely disputing the claim, they are committing an offence. RBS may be unable to disclose contact information if the recipient has convinced them your payment was genuine and not misdirected. If you can get confirmation of this, then you might be able to report it as a crime to get a crime reference to be used to extract the details of the guilty party, or take RBS to court for the return of the money (sending a letter before action to their legal correspondence address might be enough to do the trick). Neither option guarantees you'll make any progress, but unfortunately the misdirected payment code does rather depend on the honesty (or silence) of the recipient.deb1111 said:

I don't know if they have disputed or not. All I know is that Halifax couldn't recover the money.masonic said:This seems a bit of an odd one as most banks signed up to the misdirected payments code of best practice, which I believe does permit a bank to make such disclosures as are necessary to allow legal proceedings to be initiated. Any complaint should always be made against your bank, because the recipient bank (if different) does not have a contractual relationship with you.It would be helpful to understand the facts of the matter:Do you know whether or not the recipient of the money has disputed that it was sent in error?Is the recipient bank signed up to the voluntary code?

I assume RBS are part of the voluntary code.

1 -

Are you referring to the voluntary code adopted by most players back in 2014? As a voluntary code of practice, I didn't think it had sufficient status to override obligations under data protection legislation but I couldn't find a copy of the code anyway, as it was published by the Payments Council and all online traces seem to have disappeared!masonic said:This seems a bit of an odd one as most banks signed up to the misdirected payments code of best practice, which I believe does permit a bank to make such disclosures as are necessary to allow legal proceedings to be initiated.

RBS were certainly part of it from the word go though....0 -

eskbanker said:

Are you referring to the voluntary code adopted by most players back in 2014? As a voluntary code of practice, I didn't think it had sufficient status to override obligations under data protection legislation but I couldn't find a copy of the code anyway, as it was published by the Payments Council and all online traces seem to have disappeared!masonic said:This seems a bit of an odd one as most banks signed up to the misdirected payments code of best practice, which I believe does permit a bank to make such disclosures as are necessary to allow legal proceedings to be initiated.

RBS were certainly part of it from the word go though....It's a voluntary code, but it is binding on those who voluntarily signed up to it. I don't think it ever required banks to make disclosures where the recipient convinced them the payment was genuine.Edit: the code certainly has disappeared though. Payments Council become Payments UK in 2015, then UK Finance in July 2017. Sadly I couldn't find any trace of the code there.0 -

Looks like there is some pretty credible advice here about the procedure to follow:"If the recipient refuses to return the money, you need to obtain their details in order to pursue the matter. These should be requested in writing from your bank, giving them a reasonable amount of time to respond to you. If the bank refuses to provide these details on data protection grounds, you will need to get a court order compelling the bank to disclose this information. A solicitor is best placed to assist you with this. Once you have these details, you may contact the recipient directly. If the recipient continues to refuse to repay the money, you need to take legal action against them."

0 -

Yes, that was my understanding, that a court order is needed to force a bank to disclose personal data, referred to as a Norwich Pharmacal order.masonic said:Looks like there is some pretty credible advice here about the procedure to follow:"If the recipient refuses to return the money, you need to obtain their details in order to pursue the matter. These should be requested in writing from your bank, giving them a reasonable amount of time to respond to you. If the bank refuses to provide these details on data protection grounds, you will need to get a court order compelling the bank to disclose this information. A solicitor is best placed to assist you with this. Once you have these details, you may contact the recipient directly. If the recipient continues to refuse to repay the money, you need to take legal action against them."1 -

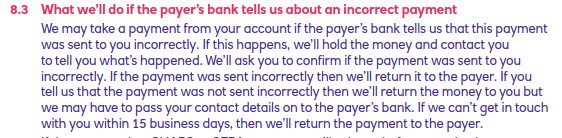

FWIW, here are the relevant T&C from RBS. At least this makes it clear what must have happened for the money not to have been returned.

Unlike HSBC, the wording is more consistent with being compelled to pass on contact details, rather than passing them on voluntarily.It's a shame really, as it adds costs that probably cannot subsequently be recovered - added on to the uncertainty surrounding the recipients ability to repay the money.0

Unlike HSBC, the wording is more consistent with being compelled to pass on contact details, rather than passing them on voluntarily.It's a shame really, as it adds costs that probably cannot subsequently be recovered - added on to the uncertainty surrounding the recipients ability to repay the money.0 -

Thank you so much everyone for your advice. I at least feel like I have a few options I can pursue here now.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards