We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Are we expecting BOE to remain at 4.75% on 8th February 2025?

Comments

-

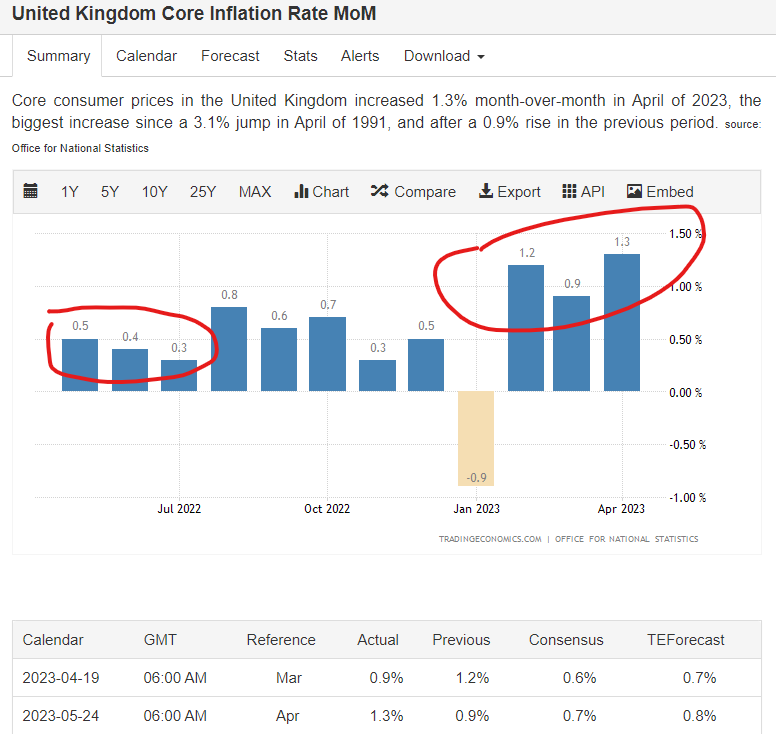

No doubt tomorrow we will hear about the large fall in headline inflation. The following chart shows why. The prior large April '22 number of 2.5% MoM will drop out and be replaced with a lower 0.8% MoM number for April '23 (should the estimate be met).

However, if 0.8% is the number, the last quarter MoM will be averaging 0.9% MoM or 10.8% annualised (ignoring compounding). If that rate of MoM numbers continue then inflation will begin to rise again as lower numbers from the start of the 12m period drop out.

The next 6 months to drop out have an average of 0.85% (that includes the large 2% figure in Oct '22). So, if inflation continues as it has for the last 3 months to April then inflation will remain far above the 2% target for all of 2023. Wage demands and expectations of future inflation will increase over time as real incomes continue to get squeezed.

Under that scenario, there is no way the BoE will not be raising rates at least another 50bps by year end.

The CPI above is headline inflation which includes energy and food. Yet look how fast the various energy and food components have fallen over the past year.

This inflation we are experiencing is about the ability of businesses to pass on price increases and the capacity of the UK consumer to pay the increase. The amount of govt spending (across so many areas) since 2020 has fueled this inflation. See the latest debt figures from today's release below.

Inflation will fall once the money runs out. Beware of the Govt offering gifts as we approach the election given where we are with debt levels. It serves only to increase demand and does nothing for supply.

Increasing supply is difficult for a government to achieve in the near term and hence they find it difficult to take credit when it occurs which is why it is rarely ever their focus.

To solve inequality and failing productivity, cap leverage allowed to be used in property transactions. This lowers the ROI on housing, reduces monetary demand for housing, reduces house prices bringing them more into line with wage growth as opposed to debt expansion.

Reduce stamp duty on new builds and increase stamp duty on pre-existing property.

No-one should have control of setting interest rates since it only adds to uncertainty. Let the markets price yields, credit and labour.1 -

The charts showing the decline in energy and food costs suggest that inflationary pressures are set to ease over the coming months as the price falls filter through to the consumer. Whether other inflationary pressures are sufficient for MOM increases over the next several months to be the same as, or higher than, the same period of 2022 remains to be seen. I predict that the MOM increases in headline CPI will be mostly lower than those in 2022, but only time will tell.

0 -

Meanwhile, over the last 6 months, 2yr yields (and 5yr) keep rising suggesting that whilst inflation may be coming down, it is coming down slower than markets had expected.

My feeling is the consumer cracks (runs out of money) before inflation comes down to 2%. It will then be deflation we need to be concerned about.

Will central banks allow the economy to 'reset' at a lower output level or exacerbate the volatility by cutting rates/adding to debt once again?

To solve inequality and failing productivity, cap leverage allowed to be used in property transactions. This lowers the ROI on housing, reduces monetary demand for housing, reduces house prices bringing them more into line with wage growth as opposed to debt expansion.

Reduce stamp duty on new builds and increase stamp duty on pre-existing property.

No-one should have control of setting interest rates since it only adds to uncertainty. Let the markets price yields, credit and labour.0 -

To solve inequality and failing productivity, cap leverage allowed to be used in property transactions. This lowers the ROI on housing, reduces monetary demand for housing, reduces house prices bringing them more into line with wage growth as opposed to debt expansion.

Reduce stamp duty on new builds and increase stamp duty on pre-existing property.

No-one should have control of setting interest rates since it only adds to uncertainty. Let the markets price yields, credit and labour.0 -

Core inflation still mercilessly beating Britons at 1.3% month on month. No doubt in my mind that this is all the motivation the BoE need to raise interest rates further.

As analysts have repeatedly said, falls in wholesale prices take months to feed through to the consumer. When these finally do feed through to the consumer, will we see negative MoM food and/or core inflation? Or is that too much to hope for?

0 -

These MoM figures are embarrassing for the BoE. They have no credibility whatsoever, from telling people to accept they're poorer, accept lower real wages to having no idea where inflation is actually heading, I honestly question whether a coin toss would be better in deciding where rates should go.

The next 3-6 months is going to be very difficult to explain unless by some weird chance MoM inflation comes in at zero. Based on the last 3 months numbers, core is annualising at 13.6% (i'm not joking) and headline at 12.4%.

For those on low incomes in rented accommodation, hopefully mortgage debt will continue on its path lower and reduce the money supply and eventually pull inflation lower.

If the Govt does anything to encourage housing demand (Help to Buy, etc) then they should be thrown out.

To solve inequality and failing productivity, cap leverage allowed to be used in property transactions. This lowers the ROI on housing, reduces monetary demand for housing, reduces house prices bringing them more into line with wage growth as opposed to debt expansion.

Reduce stamp duty on new builds and increase stamp duty on pre-existing property.

No-one should have control of setting interest rates since it only adds to uncertainty. Let the markets price yields, credit and labour.0 -

Here is the 2 year bond today, reaching for the stars. GBP is actually at risk of falling now as the BoE shows they have no idea what is going on in their own economy.

I would not be surprised if mortgage providers hike their rates today and do not wait for the next BoE hike.

To solve inequality and failing productivity, cap leverage allowed to be used in property transactions. This lowers the ROI on housing, reduces monetary demand for housing, reduces house prices bringing them more into line with wage growth as opposed to debt expansion.

Reduce stamp duty on new builds and increase stamp duty on pre-existing property.

No-one should have control of setting interest rates since it only adds to uncertainty. Let the markets price yields, credit and labour.0 -

They say 5.5% by the end of the year on the news. I thought 6% was the maximum stress testing. Getting a bit risky. Lots of people are going to be in trouble if rates remain this high.0

-

Ah, the straw that broke the camel's bac(n)k!0

-

It would spike now - I can't renew my mortgage until 5th June when no doubt fixes will be up 50+ basis points from where they were just last week

I think....0

I think....0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards