We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Are we expecting BOE to remain at 4.75% on 8th February 2025?

Comments

-

"The BoE lowering interest rates gradually is a good thing, down to a level in line with the inflation target. "MattMattMattUK said:The economy is a mess and in the short term there is little the government could reasonably do, any measures the government can take would likely be inflationary, kicking the can down the road a few months, or both. The BoE lowering interest rates gradually is a good thing, down to a level in line with the inflation target.

Pushing us into deflationary territory will be bad, equally holding rates too high for the economy. Paying interest is pretty bad all round, it is an overall negative and especially the increase in the costs of state borrowing. I know there are certain users who agitate for higher interest rates because of either poor understanding of economics or personal gain, but thankfully they are not in positions of power.

Why?

"Pushing us into deflationary territory will be bad"

Why?

" Paying interest is pretty bad all round"

Why?

If you are just talking about your own personal circumstance, don't bother replying.To solve inequality and failing productivity, cap leverage allowed to be used in property transactions. This lowers the ROI on housing, reduces monetary demand for housing, reduces house prices bringing them more into line with wage growth as opposed to debt expansion.

Reduce stamp duty on new builds and increase stamp duty on pre-existing property.

No-one should have control of setting interest rates since it only adds to uncertainty. Let the markets price yields, credit and labour.1 -

So, given that the BOE also have the objective for the stable level of inflation to be 2%...Hoenir said:

The BOE's objective is to ultimately have base rate in the region of 1% above a stable level of inflation.BarelySentientAI said:

What number is "in line with the inflation target"? You can't be meaning that it needs 2% base rate to hit 2% inflation, because we all know that's nonsense. After all, we've had 2% inflation with rates at various points between 0.25% and 7.5% that I know of.The BoE lowering interest rates gradually is a good thing, down to a level in line with the inflation target.

Overall, their job is just "have base rate at 3%"?0 -

Inflation is never stable though. Constantly fluctuates around. Base rate changes take around 18 months to reach the real economy. Base rate in the 3.5% to 5.0% would be "normal". Likewise you'd expect mortgages eventually to sit at a minimum of 1% above this. Unwinding the QE era has a very long way to go. All this flick and switch then everything is sorted reporting is unfortunately well off the mark.BarelySentientAI said:

So, given that the BOE also have the objective for the stable level of inflation to be 2%...Hoenir said:

The BOE's objective is to ultimately have base rate in the region of 1% above a stable level of inflation.BarelySentientAI said:

What number is "in line with the inflation target"? You can't be meaning that it needs 2% base rate to hit 2% inflation, because we all know that's nonsense. After all, we've had 2% inflation with rates at various points between 0.25% and 7.5% that I know of.The BoE lowering interest rates gradually is a good thing, down to a level in line with the inflation target.

Overall, their job is just "have base rate at 3%"?0 -

So you agree then that the 5% base rate we currently have is normal and there is no need to be tinkering with it?Hoenir said:

Inflation is never stable though. Constantly fluctuates around. Base rate changes take around 18 months to reach the real economy. Base rate in the 3.5% to 5.0% would be "normal". Likewise you'd expect mortgages eventually to sit at a minimum of 1% above this. Unwinding the QE era has a very long way to go. All this flick and switch then everything is sorted reporting is unfortunately well off the mark.BarelySentientAI said:

So, given that the BOE also have the objective for the stable level of inflation to be 2%...Hoenir said:

The BOE's objective is to ultimately have base rate in the region of 1% above a stable level of inflation.BarelySentientAI said:

What number is "in line with the inflation target"? You can't be meaning that it needs 2% base rate to hit 2% inflation, because we all know that's nonsense. After all, we've had 2% inflation with rates at various points between 0.25% and 7.5% that I know of.The BoE lowering interest rates gradually is a good thing, down to a level in line with the inflation target.

Overall, their job is just "have base rate at 3%"?0 -

Paying interest is the cost when you spend more than you have.MattMattMattUK said:The economy is a mess and in the short term there is little the government could reasonably do, any measures the government can take would likely be inflationary, kicking the can down the road a few months, or both. The BoE lowering interest rates gradually is a good thing, down to a level in line with the inflation target.

Pushing us into deflationary territory will be bad, equally holding rates too high for the economy. Paying interest is pretty bad all round, it is an overall negative and especially the increase in the costs of state borrowing. I know there are certain users who agitate for higher interest rates because of either poor understanding of economics or personal gain, but thankfully they are not in positions of power.

GDP based upon making money from other peoples' money is neither sound nor sustainable. When that flow drops away the whole house of cards comes down and we will get more global financial crisis. If our GDP was based upon product rather than profit we would be much more resilient.

Instead we find that debt, whether that is a household or the State debt, is wasteful and has become the drug that politicians and the public have become addicted to.

Bring back prudence.Your life is too short to be unhappy 5 days a week in exchange for 2 days of freedom!0 -

It hasn`t been normal for a long time, and for that reason people were borrowing way beyond their means for rates at 5%, that is why they will try to tinker with it but as we saw with Truss things can change very fast when it comes to bond markets and perception, having civil disorder on the streets doesn`t help either. The two massive flies in the ointment though are ME tension and the astounding market moves we are seeing in Japan, both will feed into higher borrowing costs.RelievedSheff said:

So you agree then that the 5% base rate we currently have is normal and there is no need to be tinkering with it?Hoenir said:

Inflation is never stable though. Constantly fluctuates around. Base rate changes take around 18 months to reach the real economy. Base rate in the 3.5% to 5.0% would be "normal". Likewise you'd expect mortgages eventually to sit at a minimum of 1% above this. Unwinding the QE era has a very long way to go. All this flick and switch then everything is sorted reporting is unfortunately well off the mark.BarelySentientAI said:

So, given that the BOE also have the objective for the stable level of inflation to be 2%...Hoenir said:

The BOE's objective is to ultimately have base rate in the region of 1% above a stable level of inflation.BarelySentientAI said:

What number is "in line with the inflation target"? You can't be meaning that it needs 2% base rate to hit 2% inflation, because we all know that's nonsense. After all, we've had 2% inflation with rates at various points between 0.25% and 7.5% that I know of.The BoE lowering interest rates gradually is a good thing, down to a level in line with the inflation target.

Overall, their job is just "have base rate at 3%"?0 -

It's in the range of "normal". If the economy slows and inflation is suppressed then minor changes to bring the rate lower should be expected. Though this is very different to the cost of borrowing reducing significantly.RelievedSheff said:

So you agree then that the 5% base rate we currently have is normal and there is no need to be tinkering with it?Hoenir said:

Inflation is never stable though. Constantly fluctuates around. Base rate changes take around 18 months to reach the real economy. Base rate in the 3.5% to 5.0% would be "normal". Likewise you'd expect mortgages eventually to sit at a minimum of 1% above this. Unwinding the QE era has a very long way to go. All this flick and switch then everything is sorted reporting is unfortunately well off the mark.BarelySentientAI said:

So, given that the BOE also have the objective for the stable level of inflation to be 2%...Hoenir said:

The BOE's objective is to ultimately have base rate in the region of 1% above a stable level of inflation.BarelySentientAI said:

What number is "in line with the inflation target"? You can't be meaning that it needs 2% base rate to hit 2% inflation, because we all know that's nonsense. After all, we've had 2% inflation with rates at various points between 0.25% and 7.5% that I know of.The BoE lowering interest rates gradually is a good thing, down to a level in line with the inflation target.

Overall, their job is just "have base rate at 3%"?0 -

I've noticed my Chase Savers account has dropped to 3.85%, though this was probably in reaction to August's announcement0

-

They will hold the rate at 5% for September.0

-

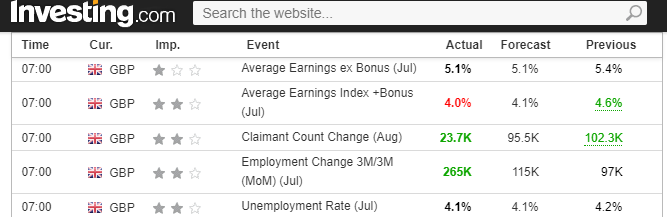

Unemployment is near historic lows, employment maybe softening but is not contracting at anything like a sharp turn, indeed strong numbers today and wage growth is 2x inflation and inflation remains above 2% target.

And yet so many think the BoE needs to cut interest rates again to "balance the economy".

Is the drug addict getting withdrawal symptoms that just cannot be resisted? More, more, more.

Today's employment and wage numbers:

To solve inequality and failing productivity, cap leverage allowed to be used in property transactions. This lowers the ROI on housing, reduces monetary demand for housing, reduces house prices bringing them more into line with wage growth as opposed to debt expansion.

Reduce stamp duty on new builds and increase stamp duty on pre-existing property.

No-one should have control of setting interest rates since it only adds to uncertainty. Let the markets price yields, credit and labour.0

This discussion has been closed.

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards