We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

45 years NI contributions required for full state pension?

Comments

-

So so true!zagfles said:Dazed_and_C0nfused said:

True, I suspect there will be some people who don't like the fact you have (almost certainly) paid reduced NI for many years but now have the chance to increase your State Pension.MikeyPGT said:I have 43 years of full contributions and an estimate of £158.68 for a SRA of April 2027, suggesting something like 49 years for a 'full' pension ... It definitely is complicated but who said anything in this life is fair?

But that's not your concern, you've probably just struck gold with the transitional rules.It's strange how the big winners from the transition always seem to be ones who always come on here complaining "it's not's fair" etc whereas the losers don't, probably because the vast majority don't realise they're losers!2 -

Especially in the days following the Money Grabbing Expert giving an overview of the subject that is down to his usual incomplete/incorrect standards.zagfles said:It's strange how the big winners from the transition always seem to be ones who always come on here complaining "it's not's fair" etc whereas the losers don't, probably because the vast majority don't realise they're losers!1 -

I don't normally - as I've said before, he's so often wrong, and his support for the WASPEs (full State pensions from age 60 for all 1950s women regardless of their circumstances) is just beyond ridiculous.p00hsticks said:

Plus the fact that under the old rules, it's the BASIC state pension that's £141.85 a week (if you're going to round, Martin, be consistent - why is £141.85 rounded down to £141, but £203.85 rounded up to £204?).Dazed_and_C0nfused said:

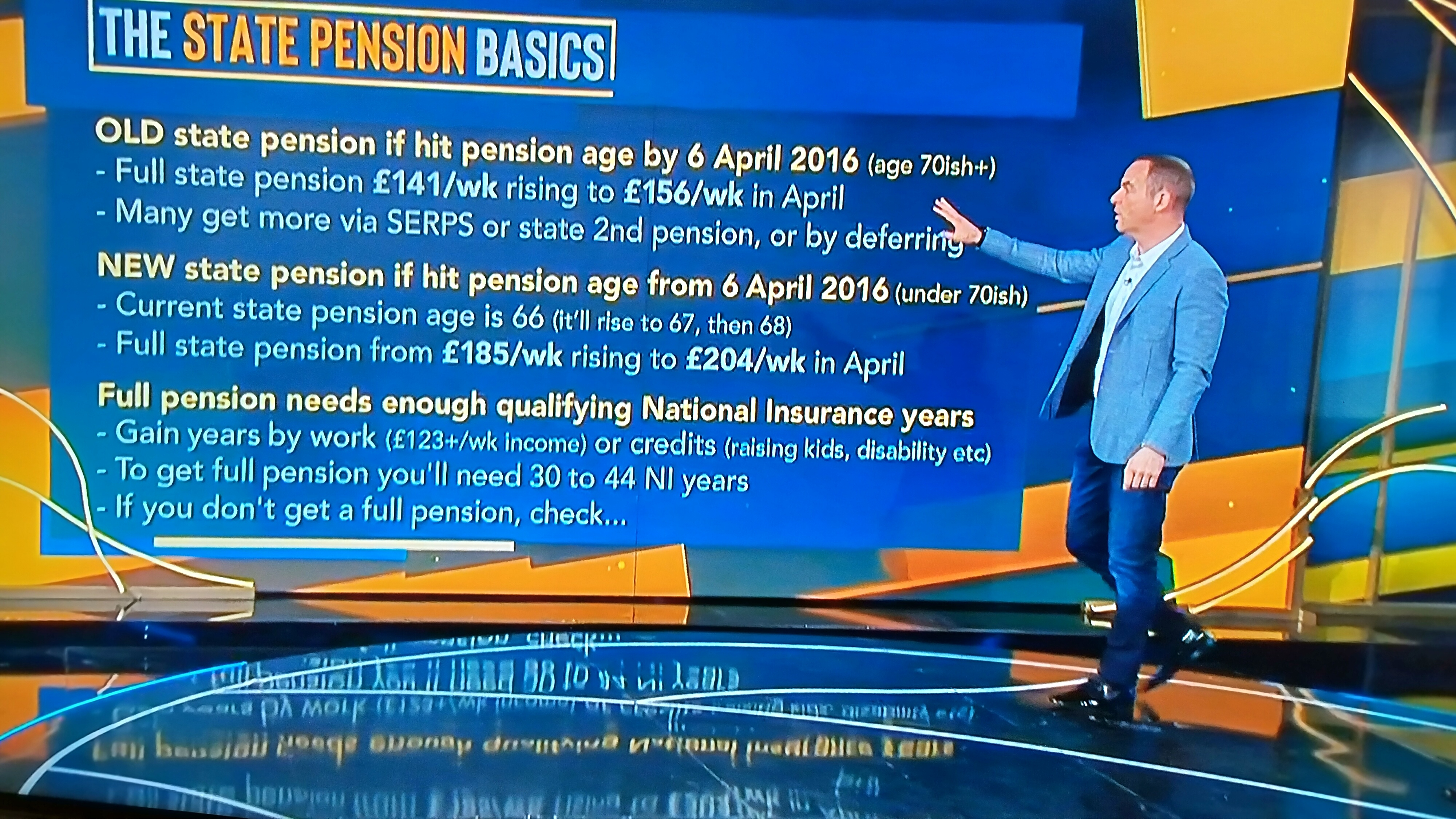

No it's not, there are other factual inaccuracies with that graphic. For example,Billportland said:I should've posted this pic in the OP, would've maybe kept the answers on subject.

The confusing part is "to get full pension you'll need 30-44 years". Appears not to be true according to several posts.

The standard new State Pension is £185.15/week not £185.

From April 2023 it will be £203.85/week, not £204.

You could get to £185.15 with less than 30 years.

Calling it the FULL state pension leads to the misunderstanding that is all everyone under the old rules got, when in fact many got much more than that with SERPS/S2P, leading to the 'hard done by/unfair ' complaints we see on this board from time to time.

Now I remember why I never watch the program - my blood pressure couldn't take it...

Made an exception for this one out of curiosity. Won't make that mistake again.1 -

Which seems odd, if I'm supposed to have reached a certain amount by the time the calculation was made in 2016, if you bear in mind that I have 15 pre 2016 years when I contributed nothing at all.p00hsticks said:

That's quite an unusual one.eastcorkram said:Here's two screen shots of what mine says today. I currently have 31 years paid, and reach S.P.A. in 2025.

The fact that you current have more than the £185.15 maximum indicates that you had already reached that amount by April 2016 and so have a 'protected payment'. I presume that it must be the possibility of filling the additional year 2006-2007 that would result in the further increase (earlier years are no longer available to buy, and you only have until April to buy 2006-7).

In contrast to what we tell a lot of people on these boards, in this particular case, post-2016 years aren't going to increase your forecast any further (but you have to continue to pay NI until you reach State Retirement Age if you are working)0 -

I'm in the "29 and done" club - or perhaps more accurately, the first time I got a forecast, I was on 29 years full contributions and it was already saying I was on the maximum (which for me is £189.45) with no opportunity to improve.p00hsticks said:

and I may be wrong, but going the other way I think we've also had someone posting who had already reached the maximum with only 29 years (because they had built up a lot of SERPS/S2P prior to 2016),Silvertabby said:Martin was wrong (again!). He should have said 'anywhere in the range of 30 to 50+ years', not '30 to 44'.

I needed 48 years (44 from working, 4 from paying voluntary Class 3s. When I mentioned this in a previous post I said that someone else on these boards had needed 49 years, and asked if anyone could beat that. Someone almost immediately popped up with their 50.I suppose it's possible I got to full entitlement before 29 years but I don't think there's any way to be able to check that. And still at least 17 years before I see a penny of it back as well!0 -

Can't see how that can possibly be correct.artyboy said:

I'm in the "29 and done" club - or perhaps more accurately, the first time I got a forecast, I was on 29 years full contributions and it was already saying I was on the maximum (which for me is £189.45) with no opportunity to improve.p00hsticks said:

and I may be wrong, but going the other way I think we've also had someone posting who had already reached the maximum with only 29 years (because they had built up a lot of SERPS/S2P prior to 2016),Silvertabby said:Martin was wrong (again!). He should have said 'anywhere in the range of 30 to 50+ years', not '30 to 44'.

I needed 48 years (44 from working, 4 from paying voluntary Class 3s. When I mentioned this in a previous post I said that someone else on these boards had needed 49 years, and asked if anyone could beat that. Someone almost immediately popped up with their 50.I suppose it's possible I got to full entitlement before 29 years but I don't think there's any way to be able to check that. And still at least 17 years before I see a penny of it back as well!

What would stop you getting the final 20p?0 -

With all due respect to your username, I'm the one that's confused now! What 20p?Dazed_and_C0nfused said:

Can't see how that can possibly be correct.artyboy said:

I'm in the "29 and done" club - or perhaps more accurately, the first time I got a forecast, I was on 29 years full contributions and it was already saying I was on the maximum (which for me is £189.45) with no opportunity to improve.p00hsticks said:

and I may be wrong, but going the other way I think we've also had someone posting who had already reached the maximum with only 29 years (because they had built up a lot of SERPS/S2P prior to 2016),Silvertabby said:Martin was wrong (again!). He should have said 'anywhere in the range of 30 to 50+ years', not '30 to 44'.

I needed 48 years (44 from working, 4 from paying voluntary Class 3s. When I mentioned this in a previous post I said that someone else on these boards had needed 49 years, and asked if anyone could beat that. Someone almost immediately popped up with their 50.I suppose it's possible I got to full entitlement before 29 years but I don't think there's any way to be able to check that. And still at least 17 years before I see a penny of it back as well!

What would stop you getting the final 20p?

And I can assure you it was correct that my pension forecast was at the max when I first checked it 3 years ago (when I was on 29 years full contributions). Admittedly back then it wouldn't have said £189.45 a week, but it would have been whatever the maximum was back then, with no opportunity to improve.

I can equally well assure you that it will be at least 17 years before I see anything back in the way of pension payments. Unless the government lowers the SPA, and that ain't happening!0 -

If you are on £189.45 that is more than the current maximum, so a very nice position to be in after only 29 full years contributions.artyboy said:Dazed_and_C0nfused said:

Can't see how that can possibly be correct.artyboy said:

I'm in the "29 and done" club - or perhaps more accurately, the first time I got a forecast, I was on 29 years full contributions and it was already saying I was on the maximum (which for me is £189.45) with no opportunity to improve.p00hsticks said:

and I may be wrong, but going the other way I think we've also had someone posting who had already reached the maximum with only 29 years (because they had built up a lot of SERPS/S2P prior to 2016),Silvertabby said:Martin was wrong (again!). He should have said 'anywhere in the range of 30 to 50+ years', not '30 to 44'.

I needed 48 years (44 from working, 4 from paying voluntary Class 3s. When I mentioned this in a previous post I said that someone else on these boards had needed 49 years, and asked if anyone could beat that. Someone almost immediately popped up with their 50.I suppose it's possible I got to full entitlement before 29 years but I don't think there's any way to be able to check that. And still at least 17 years before I see a penny of it back as well!

What would stop you getting the final 20p?

And I can assure you it was correct that my pension forecast was at the max when I first checked it 3 years ago (when I was on 29 years full contributions). Admittedly back then it wouldn't have said £189.45 a week, but it would have been whatever the maximum was back then, with no opportunity to improve.1 -

If your entitlement is currently £184.95 and you have 17 years to go to SPA then why couldn't you reach the standard new State Pension amount of £185.15?artyboy said:

With all due respect to your username, I'm the one that's confused now! What 20p?Dazed_and_C0nfused said:

Can't see how that can possibly be correct.artyboy said:

I'm in the "29 and done" club - or perhaps more accurately, the first time I got a forecast, I was on 29 years full contributions and it was already saying I was on the maximum (which for me is £189.45) with no opportunity to improve.p00hsticks said:

and I may be wrong, but going the other way I think we've also had someone posting who had already reached the maximum with only 29 years (because they had built up a lot of SERPS/S2P prior to 2016),Silvertabby said:Martin was wrong (again!). He should have said 'anywhere in the range of 30 to 50+ years', not '30 to 44'.

I needed 48 years (44 from working, 4 from paying voluntary Class 3s. When I mentioned this in a previous post I said that someone else on these boards had needed 49 years, and asked if anyone could beat that. Someone almost immediately popped up with their 50.I suppose it's possible I got to full entitlement before 29 years but I don't think there's any way to be able to check that. And still at least 17 years before I see a penny of it back as well!

What would stop you getting the final 20p?

And I can assure you it was correct that my pension forecast was at the max when I first checked it 3 years ago (when I was on 29 years full contributions). Admittedly back then it wouldn't have said £189.45 a week, but it would have been whatever the maximum was back then, with no opportunity to improve.

I can equally well assure you that it will be at least 17 years before I see anything back in the way of pension payments. Unless the government lowers the SPA, and that ain't happening!0 -

It sounds to me as though artyboy was not contracted out, so had a reasonable amount of additional pension under the old rules, meaning that with 29 years has £4.30 "protected payment" on top of his £185.15 nSP0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards